Strategy blog: UK mortgage rates

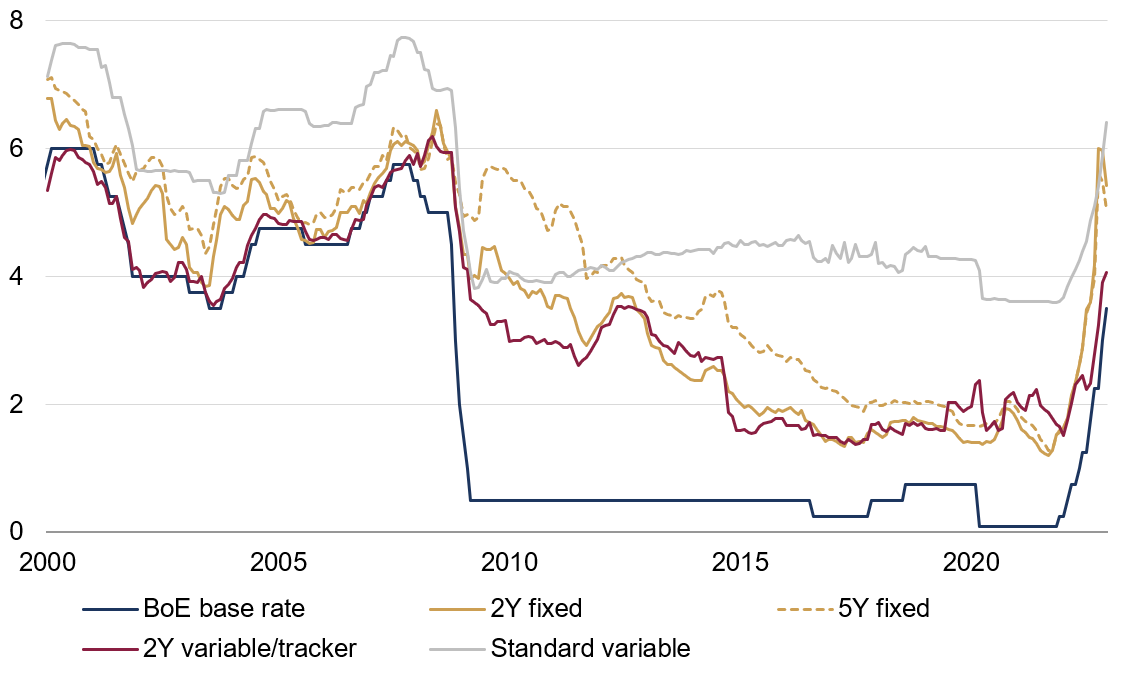

The Bank of England's tightening cycle has pushed UK mortgage rates higher, with variable and fixed rates surging to levels not seen since the Global Financial Crisis (Chart 1). It's also likely that there is further to go: market-implied rates are suggesting that the base rate will increase by another 100 basis points this year.

Chart 1: Mortgage rates have surged (%)

Source: Rothschild & Co, Bloomberg, Bank of England

Footnote: All mortgage rates are based on 75% loan-to-value ratios. The "two-year variable rate" refers to a product comprising of a variable rate tracker mortgage (Bank of England base rate plus x%) for two years, after which borrowers shift onto the "standard variable rate" (which has typically been less attractive: see chart).

A closer call: variable vs fixed rates

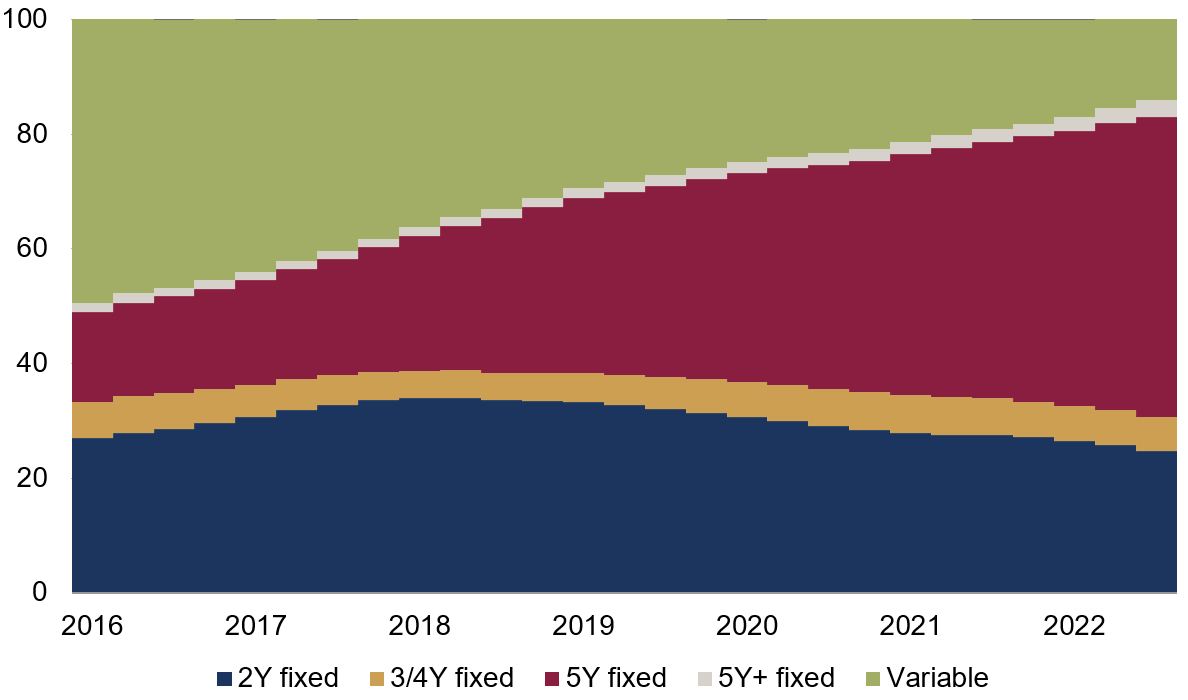

It was only (just over) a year ago when interest rates were at record-low levels. This followed a prolonged period when rates had already been historically subdued, and perhaps unsurprisingly, the bulk of outstanding mortgages gradually shifted from a variable to fixed-rate basis. Borrowers – like us – couldn't quite believe that such low rates would last, and decided to lock them in while they could, particularly since the standard variable rate didn't seem to be passing on the good news fully anyway. By late 2022, almost all borrowers had chosen to fix (or refix) their mortgages, with most opting for the longer five-year tenure (Chart 2).

Chart 2: Distribution of outstanding mortgages (% of total)

Source: Rothschild & Co, Bank of England, UK Office for National Statistics

Now that mortgage rates have rebounded sharply (and with the base rate likely to increase further in coming months), the picture is evolving again. Projected base rates – and with them, variable or tracker mortgage rates – are closer to what we used to think of as "normal" levels. So too are the fixed rates now on offer from lenders, as much of the rebound in rates is thought to be a lasting one (longer-dated interest rates such as gilt yields have also risen as the Bank has been tightening).

The question is whether today's fixed rates are at levels that, over two or five-year horizons, will average out lower than the likely variable rates. It may be tempting to choose the variable option as market-implied rates are reflecting interest rate cuts towards the end of this year. But we feel that markets might be 'jumping the gun' a little: the base rate could plateau – rather than roll over swiftly – particularly if inflation proves to be stickier than anticipated. And as noted, interest rates are likely to rise further first, something which has not yet been reflected in current variable rates.

An added complication is that the fixed rates on offer appear to have turned modestly lower in recent weeks. This could be a sign that mortgage lenders' balance sheets are healthier than in 2007-08, and they are now able to reduce rates (to stimulate demand) without damaging their creditworthiness.

As we see it, the call is currently a close one – much more so than in recent years. The psychological benefits of being able to budget more confidently may give fixed rates an edge for many borrowers, even though that may mean missing out on lower rates – which may not arrive soon anyway.

Is the economic impact overstated?

Those homeowners who are currently paying variable rates, or about to refinance or reset their fixed rates, will see their post-mortgage disposable income fall – mortgage payments could more than triple for some households. Still, the impact needs to be placed into perspective, something that many public comments fail to do. The number of households facing a dramatic increase in mortgage payments – whether in step-change fashion as fixed rates expire and are reset, or more gradually as variable rates rise – is not that large.

For one, only 28% of households have a mortgage to begin with (based on estimates for England). And for many of these, fixed rate terms will not expire soon: perhaps only 6% of all UK households will see their fixed rates reset sharply higher between the final quarter of 2022 and the end of 2023. A further 4% of all households are on some form of variable rate, and will have been grappling with rising costs due to the Bank raising base rates. This leaves perhaps 90% of all households directly unaffected in 2023 by rising mortgage rates. More fixed rates will roll off next year and beyond of course – though perhaps only another four percentage points in 2024 – but by then some other risks (such as energy costs) may have moved into reverse (arguably they already have).

Of course, this says nothing about the magnitude of the hit to disposable incomes. Moreover, it says little about the picture for households renting from private landlords, who may seek higher rents to compensate for inflation, even if they do not themselves face higher mortgage costs. However, the ONS Index of Private Housing Rental Prices was running at 4.2% year-on-year in December, suggesting only a relatively restrained – and firmly sub-inflation – acceleration to date. Nonetheless, the popular picture of a UK economy wholly driven by mortgage costs is a caricature, and not a helpful one.

Ready to begin your journey with us?

Past performance is not a guide to future performance and nothing in this blog constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

Chips: Moore spending

Strategy Blog

Despite renewed Middle East tensions and oil price spikes, a bigger market question is whether AI investment momentum can justify soaring capital expenditure. Demand remains strong, but investors are increasingly focused on adoption, monetisation and funding sustainability, raising concerns over future earnings, valuations and capital discipline.

-

Rothschild & Co receives five major awards at Euromoney's Awards for Excellence 2026

Awards

Global Advisory has been recognised with five prestigious awards at this year’s Euromoney's Awards for Excellence.

-

Politics on the beach

Strategy Blog

Populism is reshaping politics across the US and Europe, drawing parties away from the traditional centre. Rather than left versus right, voters increasingly divide along establishment versus anti-establishment lines, creating opportunities for populist movements and challenging conventional political assumptions.

-

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester

Press releases

Rothschild & Co’s UK Wealth Management business continues to strengthen its regional presence with appointment of Samantha Beach in Manchester.

-

Growth Equity Update

Insights

The 52nd Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory.

-

Monetary policy - behind the curtain

Strategy Blog

Interest rate expectations have shifted markedly in 2026, with markets now anticipating higher rates amid persistent inflation, economic resilience and more hawkish central banks. Despite this, strong AI-driven earnings have supported equities.