Market Perspective

Dry ice and mothballs

Did you miss it too? That interlude between the deflation scare and the inflation panic, when the talking heads were telling us that things were just fine? Or did the economy, like dry ice and mothballs, switch from static solid into expansive gas, skipping the liquid bit in the middle?

Neither. Headlines never tell us things are fine; the economy does not sublime. The news machine punctuates crisis with crisis, but economic reality is less volatile.

If we’re going to worry about something, it has always been inflation, not deflation. We think the economy is less fragile than feared (or officially forecasted). And while there have been many destructive hyperinflations, there have been no hyperdeflations. That said, today’s inflation threat needs to be kept in perspective.

In particular, while it has coincided recently with slower growth, to label the result “stagflation” is premature. It took a decade for the original stagflation mix to brew, and the inflation-per-unit-of-growth ratio — and its social impact — was grim when it did. Could it happen again? Of course. Will it? We doubt it, for reasons outlined below.

If economies really were about to stagnate, the chances of today’s socially aware central banks tackling that inflation with higher interest rates might be smaller. As things are, we think policy rates are set to start normalising (again) a bit earlier and further than money markets expect. In the short term, that can hardly be good news for stocks, where there are again profits potentially to be taken. But corporate earnings may regain the lead in their race with interest rates, and bonds look strategically more exposed to us.

Capital markets can alter state more quickly than the underlying economy.

(COP26 — previewed in August — is still underway, and will be reviewed in December’s issue)

Kevin Gardiner/Victor Balfour, Investment Strategists

Please use the buttons below to read the other blogs in this edition of Market Perspective

| One thing after another? | Kevin Gardiner | 5 minute read | |

| The UK goes boldly… | Kevin Gardiner | 4 minute read | |

| UK government debt: inflation matters | Victor Balfour | 3 minute read | |

| IMF takeaways | Victor Balfour | 1 minute read | |

| Looking for direction | Charlie Hines | 3 minute read | |

| Anyone can be popular | Kevin Gardiner | 8 minute read | |

| Costs and consequences | Kevin Gardiner | 8 minute read |

One thing after another?

Supply bottlenecks and labour difficulties. Surging energy and food prices. Talk of a revived gold standard. Slowing growth. More taxes. Bigger government. Here in the UK, the pound “plummets”. You blink, and we’re back in the 1970s — or at least we’re increasingly told we are. The queue of pundits diagnosing “stagflation” would not be out of place at a London filling station.

To all this, add some more modern ailments, such as an energy squeeze reportedly made more acute by a shortage of wind, and some perennial concerns, such as dysfunctional US politics and government dictat in China, and all of a sudden Goldilocks has been eaten by the bears, and the Governor of the Bank of England is expecting a Biblical plague.

Except it's not quite like that.

There isn’t room here to tackle the latest rebuilding of the wall of worry (and we have already discussed some of its bricks in earlier posts and Market Perspectives). This post is just a holding statement, advising — as we often do — against rushing to make dramatic adjustments to long-term investment portfolios.

Those echoes from the ‘70s are audible, but faint. To stretch the metaphor, we hear them partly because our media-trained ears these days are sharper. The pound’s “plummet” was a dip of less than 2%.

“Stagflation” then was eventually diagnosed after a decade-long struggle to maintain Western monetary credibility. The inflationary surge then, and the slowing in growth, was itself a decade or so in the making. Key ingredients included abysmal industrial relations and a newly formed oil cartel (at a time when oil was both more important, and more widely believed to be scarce, than it is today).

Monetary credibility recently has been much stronger. Inflation has been low and stable, which has boosted confidence in central banks’ explicit inflation targets (which were not around in the ‘70s) and reduced the risk of spiralling, self-fulfilling expectations.

We do worry that central banks may have become a bit complacent now — we have written often about mission creep and hubris. The idea that inflation is capable of being “fine-tuned” is (in our view) mistaken. But there is no doubt that inflation expectations now are much less deeply ingrained than they were then, whatever bitcoin promoters would have us believe.

The original gold standard was not casually discarded, but effectively fell apart after it failed to cope with the strains posed by that gathering inflationary momentum in an increasingly multi-polar world. The world was not crisis-free under gold, but it was a lot poorer. So far this year the gold price has fallen, suggesting monetary credibility may not be especially fragile.

The economic disappointments of the ‘70s were much more dramatic and durable than anything we’re encountering (or, in our view, are likely to encounter) now. Western inflation in 2021 is going to exceed expectations at the start of the year, but perhaps by a percentage point or so. Some upturn was always on the cards as economies reopened — see our January report, “Inflation: revision notes”. We think that trend rates, not just this year’s, will be higher in future than they have been of late. But those trends are still likely to be confined to low single digits.

And today’s labour problems — or at least, those that persist beyond the immediate reopening phases — are not those of the ‘70s. Then, we had sustained higher levels of unemployment to look forward to (though we didn’t realise just how high, or for how long) as market rigidities were slowly eased. Now, we may be looking at a labour market that will become effectively fully employed into the medium term. Some jobs may need higher real wages to attract workers — and while many of those are skilled occupations, some will be more foundational, which might address some inequalities at least.

This may be what is starting to play out currently. The mix of post-pandemic occupational reappraisals with pandemic-related changes to work incentives — with Brexit an additional source of uncertainty here in the UK — means that nobody can know the likely duration of today’s problematic shortages.

But levels of labour utilisation today are still below those seen pre-pandemic. It may not feel like it, but there is still some slack in the system. And even when that slack is fully taken in, there is still plenty of room for productivity to grow: the supply-side constraints that lead to that underlying inflation risk are likely looser than they used to be.

Inflation has always looked to us more likely than deflation, and our portfolio managers have compiled their long-term investments partly with that idea in mind. But we have not seen anything yet to make us think that the scale of the underlying threat — as opposed to the immediate energy and bottleneck-inspired spike — is significantly bigger than we’d thought.

Kevin Gardiner — 30 September

![]()

The UK goes boldly…

The Autumn Budget presented by the Chancellor confirms the UK as one of the few developed economies to be embarking on policy normalisation. The Chancellor presented a set of prospective accounts confirming that UK fiscal policy is both less loose than he’d previously suggested, and poised to normalise faster in the years ahead.

Cyclically adjusted current borrowing is now on course to disappear in 2023/24 (previously 2025/26), having peaked at 12% of GDP in 2020/21. Headline borrowing falls from 17% in 2020/21 to 2% in 2025/26 (previously 3%). The net debt ratio is now expected to peak at 98% of GDP in 2021/22, whereas it was previously projected to peak at 110% in 2023/24 — a revision that is sensational, or should be.

The Chancellor was able to do this without actually planning any new tightening (that is, beyond what had already been announced). There is to be a further net increase in taxes, but planned spending is poised to rise by more (as part of the government’s “levelling up” strategy for reducing inequality — that is, for winning the next election).

Regular readers will not be surprised at the main reason for this surfeit of cake (that is, cake for having, and cake for eating). Not for the first time, the OBR, whose economic forecasts are the input to the Treasury’s projections, has been significantly too pessimistic on the rebound in economic growth, which is now put at 6.5% in 2021 (previously 4.0%). Higher inflation will probably also boost some taxes, though it will do the same to spending too (and in some unusual areas — see below).

In addition, not all of the government’s contingent support for pandemic assistance may have been taken up: the starting point for debt is smaller than it was too. Again, this will not surprise regular readers.

Monetary policy — which is independent of the government — also seems likely to start tightening sooner than markets had expected, and earlier than in the other major economies. In his latest comments about inflation, the Governor of the Bank of England has all but validated more hawkish money market expectations.

Whether he meant to speak quite as frankly as he did is moot, but for the Bank’s Monetary Policy Committee not to follow through could be a risky strategy. Rates seem poised to rise (and not because of energy prices, but because the economy is stronger, and employment prospectively fuller, than the Bank had realised).

We expect the Federal Reserve to follow suit in the first half of 2022 — again, because of lasting underlying inflation pressure, not transitory headline risk.

Are these really such bold moves by the UK? As that budget arithmetic suggests, much of the fiscal “tightening” is being done by the economy, not to the economy. And a 15 basis point increase in interest rates this month — which is what the money markets think they have been promised — is much smaller than traditional monetary moves.

Nonetheless, we can see the stage being set for a rerun of economists’ popular pastime of “spotting the policy mistake”. At some stage in the next few months/quarters, growth indicators will doubtless surprise to the downside, at which point we should expect to read many “we told you so” essays along the lines of “central banks have killed growth again”.

Such slowdowns might prove temporary, or benign (maybe by then all the pent-up demand will have been sated). If the UK — or US — economy cannot live with slightly higher nominal interest rates than today’s, then our reading of it is wrong, and we’re surely doomed.

Kevin Gardiner — 27 October

![]()

UK government debt: inflation matters

As noted, the UK is the first big developed economy to tighten fiscal stance — a remarkable move, perhaps, given the stimulus packages being debated in Congress and the expansive policies being considered in Germany and Japan. Why is the UK government so keen to cut its deficit?

It could be an attempt to restore the UK’s international credibility, or an attempt to consolidate control of the political centre ground. But it could also reflect a more prosaic pressure: the UK’s mounting interest bill on the back of rising inflation.

For most developed governments, a little bit of inflation, if it delivers negative real borrowing costs, erodes the ‘real’ value of those liabilities. However, roughly a quarter of the UK’s outstanding debt is index-linked gilts (ILGs) — disproportionately more than the US or Germany, for example.

Inflation as measured by the UK’s Retail Price Index (RPI) — the reference for UK ILGs — is at a decade high of 4.9% and poised to accelerate further (as is internationally comparable Consumer Price Index inflation, at 3.1%). OBR estimates suggest that a one percentage point increase in the RPI adds £4bn of inflationary uplift to the capital value of those bonds at redemption.

Mr Sunak may well have some fiscal breathing room even if such inflationary pressures persist. UK interest payments have fallen in absolute and relative terms over the past five years, even as the stock of debt has grown by more than a third. But that headroom could quickly be eroded.

Eventually, if inflation becomes too entrenched, the markets might start to anticipate higher real borrowing costs too, and as the stock of debt is rolled over, the cost of new borrowing will rise alongside the inflation uplift.

The Treasury might issue more conventional (nominal) gilts. But asset-liability matching schemes — including pension funds and insurers — continue to demand indexed gilts, even at today’s negative real yields. Today, the yields on ILGs are close to all-time lows, with the 10-year at -2.9%.

For traditional investors, the budget deficit itself rarely drives yields — inflation and the business cycle matter more. And the yields on both nominal and index-linked gilts are still too low for comfort. While inflation expectations are still rising — as we write the rate of RPI inflation priced into the 10-year gilt is pushing above 4% for the first time since 2008’s spike — then index-linked gilts will continue to outperform. They are not attractive return assets, but diversifiers, muting the risk of a more dramatic (tail risk) inflation outcome.

Victor Balfour — 27 October

![]()

IMF takeaways

In the IMF’s October semi-annual World Economic Outlook (WEO), global growth has been trimmed this year to 5.9% (from 6.0%), while inflation risks have been upgraded to 4.8% (from 3.6%) — a warning shot across the bows of unhurried central bankers, perhaps.

Some more subtle and positive aspects of the report were perhaps overlooked.

The revised economic forecast shows that advanced economies may be closer to regaining their earlier trendline than the Fund suggested in April. Projected annualised growth has been revised from 2% to 2.3% for 2022 to 2026 — equivalent, cumulatively, to the addition of a country like Switzerland (in dollar terms).

The fiscal story has also subtly improved too. Debt-to-GDP ratios fall from this year, shaving some two and a half percentage points off advanced economy debt-to-GDP ratios by 2025 relative to April’s estimate (from 121% to 118.5%).

It’s clear we are not out of the pandemic woods yet — the Fund sounded caution on the Covid-19 threat, suggesting “huge risks” remain if the developed world fails to deliver on more equitable global vaccine rollout. But at least for now, the IMF’s projections, though cautious as ever, point overall to continued growth and relatively well-anchored inflation.

Victor Balfour - 19 October

![]()

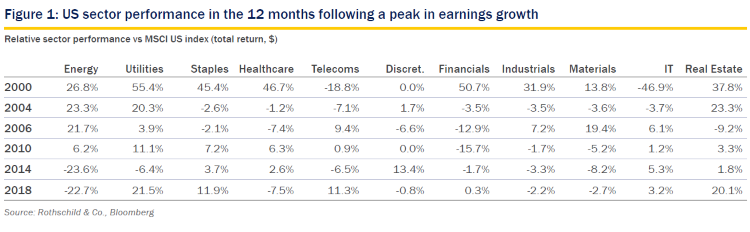

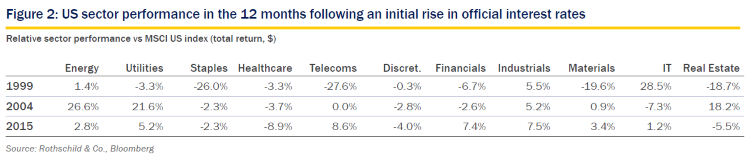

Looking for direction

Much of the post-lockdown recovery is surely now behind us, and the key macro themes of restored profitability and (even) lower interest rates are now largely priced in to stock markets. Without trying yet to call the climatic “growth versus value” race (with the former still far out in front), are we poised to see some tactical rotations in market leadership?

What are the candidates? Sectors might offer long-term, secular growth (that is, high growth driven by long-term trends in technology and/or lifestyles). They could be plays on short-term (cyclical) economic growth, or on interest rates. Others might offer relative stability, or defensiveness. (The first of these groups is the core of the wider “growth” segment, but that bloc (or investment “style”) is named more for its valuation characteristics than for its economic footprint.)

Market leadership is not always clear, and some sectors can exhibit more than one of these characteristics. Banks are both cyclical and interest rate plays. Tech can offer both secular growth and cyclicality. Energy can be seen as cyclical; sometimes as defensive; and until recently perhaps as a secular decliner (thanks to ESG concerns).

What might cause a rotation now? The peaking of corporate earnings growth, perhaps, and the beginning of some rebound in official interest rates.

A slowdown in aggregate corporate earnings is not the same as a recession-led reversal: the latter would warrant a search for outright defensive sectors, such as food and drink, and utilities. Slowdown might simply trigger a switch to overlooked sectors that might have lagged in the immediate excitement of recovery.

Rising interest rates (or a steeper yield curve) can boost banks’ net interest income, and hurt bond-like utilities and real estate sectors; but if driven by a strong economy they can also refocus investor attention on sectors exposed to the business cycle.

The circumstances in which we arrive at inflection points in growth and interest rates are different in every cycle, and when we look at the historical data (see for example Figures 1 and 2) there seem to be few consistent winners and losers after these inflection points. This cycle is perhaps even more special than usual, and we doubt that any simple rules of thumb could be relied upon. And as noted, there doesn’t have to be a clear leader anyway.

That said, while we may not yet have strong views on the next market leader, if any — in the top-down context, we still favour a mix of sectors — we have more conviction as to what it won’t be, namely: defensiveness. It seems too early to worry about the next recession and/or financial crisis.

Charlie Hines — 19 October

![]()

Anyone can be popular

Germany’s new government…

Whatever the political colour of the eventual new coalition government in Germany — whether “Traffic Light” (most likely), “Jamaica”, or another red-black “Grand Coalition” (see our August 25th post) — we doubt it will be a game-changing outcome for investors. It is hard to imagine business as usual without Chancellor Merkel, but that is what Germany seems likely to get.

That said, there were a few things for investors to ponder. The SPD’s gains were smaller than those made by the Greens, whose best-ever result made them the third-largest party: a force to be reckoned with, particularly since the bigger parties seem happy to consider working with them (and vice versa).

Less visibly, but perhaps just as importantly, the results confirm the nationalist AfD party has lost momentum, its vote falling by two points. It is the fifth-largest party, but this may overstate its significance, as the others will not work with it. Is populism losing popularity, in Germany at least?

… and some Big Picture musing

Conventional wisdom sees a wider test of this hypothesis looming with next April/May’s presidential election in France. Le Pen’s rebranded nationalist party has been running neck-and-neck with Macron’s LREM, though it has faltered in recent weeks as another populist threatens to split the right’s vote.

But what exactly is a populist? Arguably, “populism” is a tactic, not an ideology, and it can appeal in any number of contexts — not just the explicitly political — and to all sorts of people.

Consider, for example, a couple of recent “you couldn’t make it up” stories. A TED-talking behavioural economics paper on consumer honesty is reported to have been based on fabricated data. The IMF effectively reverses, at the drop of a hat, its own long-standing establishment view on debt and says maybe it doesn’t matter quite so much after all (“Sorry, Enfield!”). Then we read of alleged manipulation of the World Bank’s international “ease of doing business” indices. The cynicism such stories foster has nothing to do with nationalism, but can perhaps contribute to a generalised anti-establishment resentment.

President Macron is not a nationalist, and his own background is hardly anti-establishment, but his stunning success in 2017 was nothing if not populist — that is, if we define populism as an appeal to ordinary voters over the heads of the established parties. LREM itself is a vehicle for Macron and his views. Perhaps success for Macron — and now for the Greens in Germany — was/is not evidence of waning support for populists, but simply a different manifestation of it.

For several years, pundits have extrapolated the rise of populist nationalists — in Italy, France, Germany, the US, Brexit and elsewhere — into a Big Picture that embraces (among other things) a wholesale rejection of the EU and globalisation, and a nascent threat to democracy. We are wary of Big Pictures at the best of times, and this one has seemed especially unconvincing.

Populism’s defining streak may thus be a rejection of the establishment, not chauvinism and autarky. A widespread wish to “stick it to the man” — to give the great and the good, the talking heads, the know-it-alls, a biff on the nose for their complacency — may have different consequences than the conventional Big Picture suggests. It may be a tactical, not strategic, phenomenon, and — while in place — may point in some unexpected directions.

Exactly what establishment is being rejected may vary. In Germany, the target of voter resentment is perhaps not now a refugee-welcoming administration, but climate change deniers. In France, Macron’s LREM may now be just another established party, and France’s volatile electorate may indeed yet set up a new populist challenger to both Macron and Le Pen. Italy’s shifting array of populist parties — including one led, for a while, by a bona fide comedian — is almost too volatile to follow.

In the US, however, the new administration has quickly been unmasked as the old establishment, once again presiding over political dysfunction: the Beltway swamp is undrained. The president has not yet got his infrastructure and redistributive plans through Congress, and the debt ceiling, and risk of federal government shutdown, is again a chronic concern.

Perhaps ironically, Biden faces criticism over (amongst other things) his harsh treatment of immigrants, his provocative stance towards China, and Afghanistan. A book revealing that a senior general actively worked against the Trump administration in its final days backfired, managing almost to do the impossible and cast the outgoing administration as a wronged party. A very familiar populist is itching for another go in 2024.

Which is the in-crowd now?

In the UK, the homemade difficulties facing the government are not yet translating into any great surge in support for the established opposition party. Somehow, as Brexit has “got done”, the government — a Conservative administration! — has morphed into the anti-establishment party, and the unfortunate opposition party (both parts of it) looks like the political in-crowd (as, perhaps, do the local environmental activists, who seem determinedly unpopular).

Brexit’s importance may dwindle if/when it becomes clear — current embarrassments notwithstanding — it is not the transformational event Project Fear said it would be. The Treasury economists who drew up the scary simulations, and who had earlier failed to realise the real economic significance of free movement after the EU enlargement in 2004, perhaps represent an economics mainstream that can appear overconfident and unaccountable, pretending to expertise in a field that does not permit it (as per those examples above).

When a leading Brexiteer said “the people of this country have had enough of experts… saying that they know what is best and getting it consistently wrong”, we could see what he was driving at: a distrust of those talking heads. Economists may want to be compared to technicians like doctors and mechanics, as their indignant responses to the comment made clear, but the reality is that our subject matter doesn’t permit the provision of such precise advice. The Brexit debate was particularly frustrating because the counterfactual scenarios could never be known. (Declaration of interest: we couldn’t see an economic case for leaving, but doubted it would be a game-changing event.)

Meanwhile, the Conservative administration focuses on “levelling up” the left-behind regions, using higher taxes and bigger government if need be, and thereby triangulating the supposedly radical opposition almost into electoral irrelevance. (Not all those regions may want to be levelled up by a Westminster government — but are Scotland’s nationalists best viewed as populists, or have they become a local establishment to be rebelled against?)

Investment conclusion?

The Big Picture that equated surging populism with nationalism, and with a lasting retreat from globalisation, was an oversimplification. Perhaps only in the US is the initial caricature intact (which is admittedly hardly reassuring, but at least the rest of the world may be moving on).

In many places populist nationalism has not really taken hold to begin with. Switzerland has not been immune from insular tendencies, and its traditional referenda offer populists plenty of opportunity for expressing them. But while there are lots of voting opportunities, the government is small, and seems to lack a personality against which to rebel (this is not a criticism).

In China, it’s the opposite.

Kevin Gardiner — 7 October

![]()

Costs and consequences

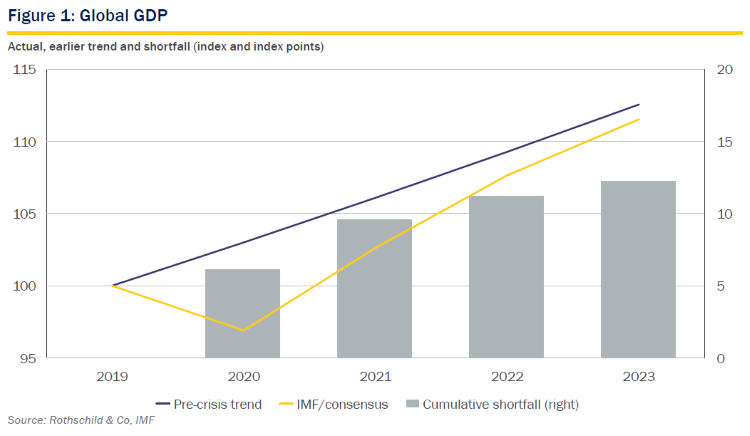

How have the macro consequences of Covid evolved since our discussion in June 2020 (when we suggested inflation risk would be one likely legacy)?

The global economy likely regained its pre-pandemic size in the spring, and has since expanded further. However, the economic costs of suppressing the virus are arguably still mounting. Costs…

The relevant shortfall is not the cumulative difference between pre-pandemic levels of GDP and what actually happened, but the cumulative gap between what would otherwise have happened and what did. Without lockdowns, GDP would not have stayed put, but would have grown.

We suggested in June that such a counterfactual path is unknowable. A plausible guesstimate, however, is that global output at the end of this year may still be perhaps 3% lower than if we hadn’t collectively decided, in 2020, to close much of the economy to deal with the public health emergency.

The cumulative shortfall at end-2021 might be around 9% of annual GDP, or $8 trillion, and it will continue to grow as long as output stays below its previous trend path. It is difficult to compare this with the position at a similar stage after 2008’s Global Financial Crisis, because the global economy’s pre-2008 trajectory was unsustainable, making it (even) harder to identify a plausible counterfactual trend. But the peak-to-trough fall in quarterly global GDP was much steeper: 9% now, 2% then.

The gap between actual GDP and an extrapolation of earlier trend growth may narrow further (Figure 1, based on annual data). It could close completely, and might even turn positive — at which point cumulative costs would start to fall, as some of the lost output is effectively made good.

Such a “catch up” scenario may not be the most likely, but is distinctly possible, as we have noted often. Policy remains supportive; productivity growth continues; and capacity has been less damaged than feared (today’s bottlenecks notwithstanding).

Until we know whether the gap stays open, closes or reverses, we can’t draw up a final GDP bill.

…and consequences

What about the other obvious macro effects of Covid suppression, namely: (1) higher government debt, and the higher taxes that may be introduced to deal with it; and (2) greater inflation risk (lasting beyond the “transitory” component of the recent spike)?

These are important. But neither debt nor (moderate) inflation is a net cost in the way lost output is.

Debt does not affect potential growth, despite the best efforts of some very smart economists to show otherwise. The world cannot be insolvent, nor borrow from unborn generations. Debt can lead to liquidity squeezes, and redistribute economic potential from one group to another; but these are different concerns.

There is no indication that the additional government debt issued to help sustain poorer families and companies during lockdown is “unsustainable”. We have not crossed a Rubicon, and bond markets have been happily financing that extra borrowing when asked to do so: there has been little link between government debt ratios and bond yields, historically or recently.

There could admittedly be all sorts of second-order effects from extra government debt, and a really determined government could surely do some serious damage to incentives and markets if it borrowed aggressively enough.

But the extra government debt is not itself a net economic cost. It shifted spending power from bond buyers to families and businesses, and in due course it will be taxpayers who repay those bondholders. The profile of growth will have been smoothed, but the economy will end up roughly where it would have been had the debt not been issued. Similarly, extra taxes now are not a long-term cost to the economy overall, but are simply reversing the earlier redistribution.

As it turns out, earlier official economic forecasts of economic growth and government borrowing are, predictably, looking too pessimistic, and (as we note in an earlier essay) debt ratios are set to peak sooner, and taxes rise less, than feared.

If the redistribution of spending power lingers too long, then the debt might be said to be contributing to the inflation pressure we have long been braced for (though today’s bottlenecks likely exaggerate the underlying capacity shortage, and the Federal Reserve is probably right to suggest that some of today’s inflation spike may be transitory).

But monetary policy is also playing a role there, as is the risk to monetary credibility posed by the seriousness greeting the idea of “Modern Monetary Theory” — that is, the idea that governments might as well simply print money rather than borrow it. Quantitative easing programmes — the buying of bonds by central banks — come close to doing this.

Inflation itself, while a serious matter for investors — see January’s “Inflation Revision Notes” report — need not be a net cost to the economy in the way that lost output is. Provided it remains moderate (say 2–4% on a trend CPI basis, as opposed to the sub-2% trends economists had started to take for granted) there is no need for it to have a significantly disruptive macro effect.

Like debt and taxes, moderate inflation will redistribute spending power, in this case from savers to borrowers. If real interest rates were to rise back into positive territory even this effect might be cancelled, but we see no big central bank willing to countenance such hawkishness currently.

Are there any positive macro consequences? Lower interest rates, and a remarkable surge in productivity, have boosted bond and stock markets, and even as nominal interest rates begin to rebound we doubt these effects will be completely reversed.

This has obviously been good news for investors, but it does not in itself represent an addition to aggregate well-being: potential output is no bigger (again, with this assertion we are ignoring all sorts of secondary effects).

The acceleration of the shift to a more weightless (digital) economy, and to more flexible working arrangements, can perhaps be seen as beneficial side effects, but these are qualitative and subjective in nature.

Was there an alternative?

The bottom line then, macro-wise, is the shortfall in GDP: this is the net economic cost of Covid. As noted, it is still too soon to balance the books. But even if there is no catch up, and the shortfall (or output gap) stays wide or grows further, we should be wary of interpreting the total too literally. “Cost” can seem to imply choice, but there may have been little alternative.

A pandemic was — is — always possible. We don’t know whether this virus was preventable. Sometimes there are only bad outcomes to choose between. If we had not locked down economies, many more people would have died, perhaps a multiple of the number we have lost to date.

It is mistaken to say that we cannot put an economic value on human lives: we have noted that insurance markets and politicians (via healthcare budgets, for example) do just this. A more complete analysis, then, might also try to take into account, alongside lost GDP, the implied economic cost of lives lost and saved, drawing on estimates in use elsewhere. Sadly, in contrast to conventional calculations involving “quality adjusted life years”, the charges here are not anonymous statistics but reckoned in terms of relatives and friends.

Kevin Gardiner — 26 October

![]()