Business with Humanity - 91 Global Environment Fund

Fund portrait

Launched in 2019, the Ninety One Global Environment Fund is a global long-only equity fund investing in companies leading in the reduction of carbon emissions. The fund uses proprietary bottom-up research to identify companies which will benefit from sustainable decarbonisation using quantifiable carbon-avoidance metrics. The portfolio is based on high conviction trades and is benchmark agnostic with just c. 25 stocks. All the companies in the fund are exposed to at least one of the key pathways to a low-carbon economy.

The fund is managed by specialists in this sector, Deirdre Cooper and Graeme Baker. Prior to joining Ninety One in 2018, Deirdre was a partner, co-portfolio manager and head of research at Ecofin where she worked for over 10 years. Graeme joined in 2010 as an energy equity and commodity analyst, covering conventional and new energy sources. The co-PMs are supported by the wider thematic equity team of Ninety One. Established in South Africa in 1991 under the name of Investec Asset Management, Ninety One is an independent, active global asset manager, managing more than USD 180 billion in assets.

The following interview with Deirdre Cooper was held on 30.09.2021.

Deirdre, you have been working in sustainable investing for many years. How has the sector changed since you started?

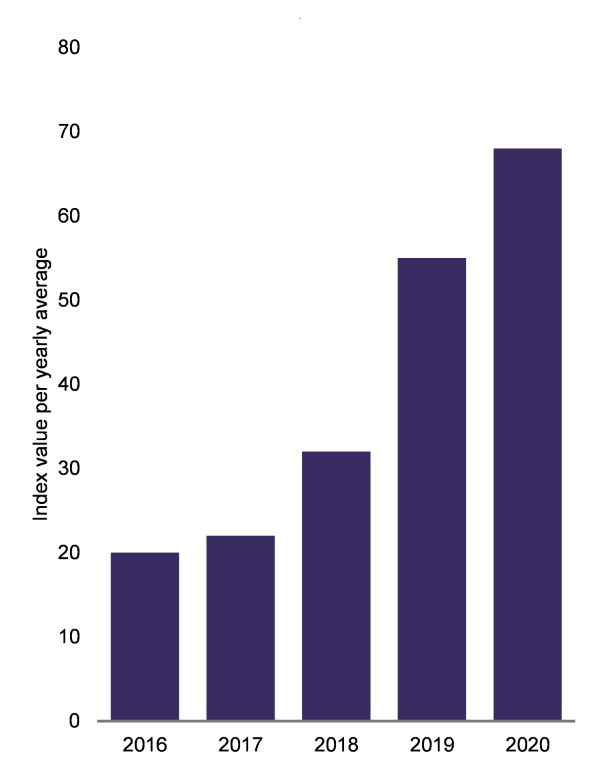

Since I started investing in the space almost 20 years ago, the sector has changed significantly. First, there has been considerable technological progress. Renewable energy used to be a very expensive form of electricity. These costs have declined by 20% p.a., so we are now at a point where renewable energy is almost always the cheapest alternative to fossil fuels when it comes to generating power. Second, there has been a change in consumer behaviour as well as consumer preferences. In the last 20 years we have seen a large increase in the number of people who question the carbon footprint and sustainable attributes of the goods they buy (see the R&Co article on The Conscious Consumer). This was recently confirmed by our proprietary survey - planetary pulse – as well as the WWF's first survey on sustainability where google searches for such products were analysed. Surprisingly enough the biggest increases in consumer “eco-awareness” were in emerging market countries such as Indonesia and Pakistan.

At the same time however, the pace of regulatory change has been disappointing. Governments signed up very quickly to treaties but have been slow in implementing them. We would expect that to accelerate but as with all initiatives which rely on regulation, the devil is in the detail. We are therefore eagerly awaiting the outcome of COP 26 in Glasgow.

Global Google searches for sustainable products (shopping products) Source: WWF and EIU report 2021: “An Eco-wakening”; Ninety One Planetary Pulse Survey 2019.

Source: WWF and EIU report 2021: “An Eco-wakening”; Ninety One Planetary Pulse Survey 2019.

|

The UK has hosted the 26th UN Climate Change Conference of the Parties, also known as COP26, in Glasgow, Scotland between 31 October and 12 November 2021. The conference is set to incorporate the 26th Conference of the Parties (COP) to the United Nations Framework Convention on Climate Change (UNFCCC). It is the 16th meeting of the parties to the Kyoto Protocol (CMP 16), and the third meeting of the parties to the Paris Agreement (CMA3) . This conference is the first time that parties are expected to commit to enhancing those climate change mitigation targets agreed to in Paris during COP21 in 2015. |

Source: 91 Global Environment Impact Report, 2021

The fund's strategy is focused on decarbonization. How do you achieve and measure this and what are the themes you look for?

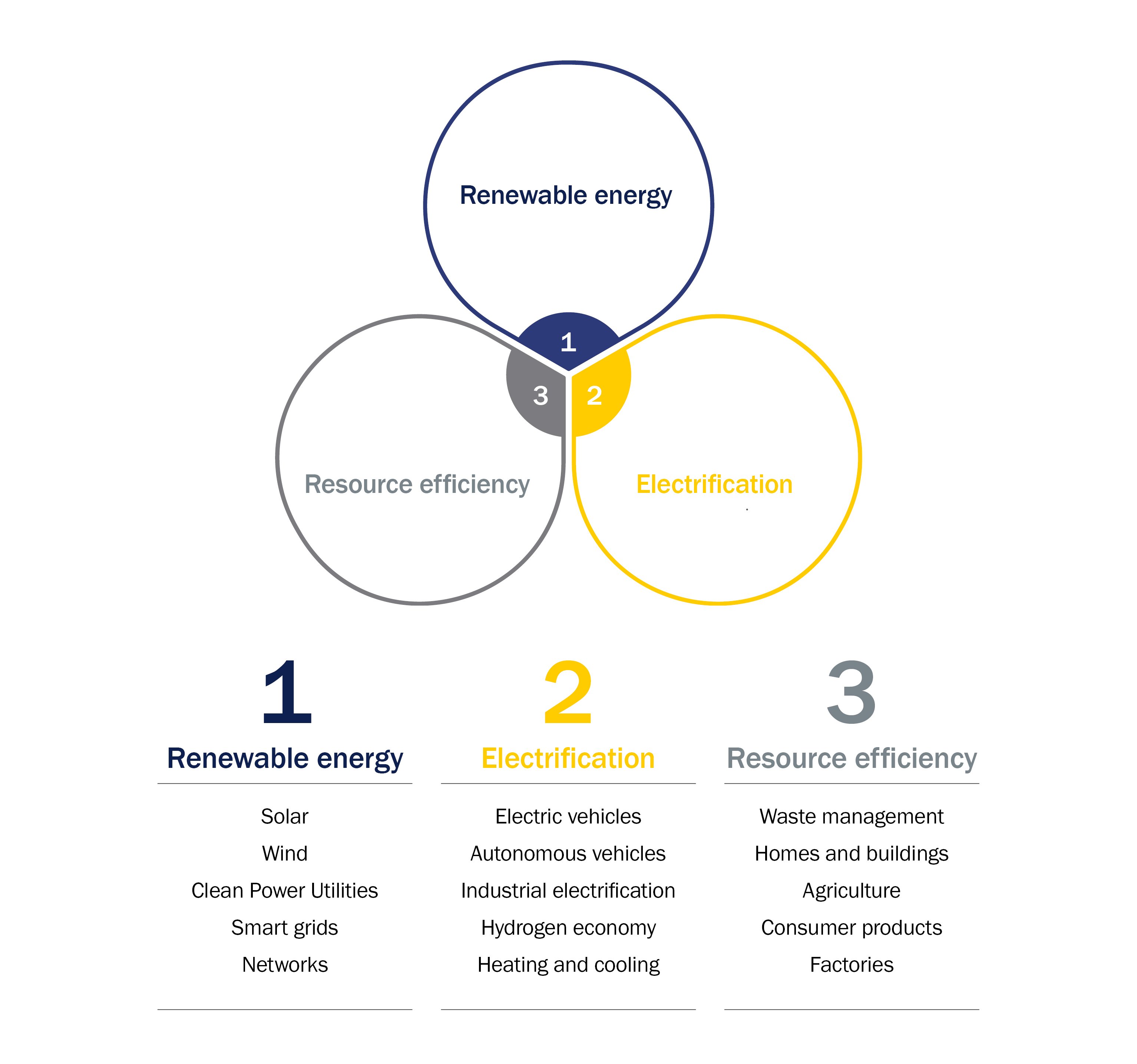

Every company in our investment universe manufactures products that avoid the use of carbon. We select these companies from three pathways which we view as critical to a low-carbon future, (1) Renewable Energy, (2) Electrification, and (3) Resource Efficiency. To measure carbon avoided, we take a sector-specific approach. For example, in power companies we look at all the assets they own, calculate their carbon footprint and then compare them to their sector peers. We look for companies that have positive carbon avoided as evidence that these businesses are part of the solution in tackling climate change. The method we apply across different value chains allows us to identify companies that are the real enablers of decarbonisation and that also create a positive impact since they are selling products which ultimately help to curb climate change.

Turning to energy – what are the consequences of high energy prices for the renewables industry?

The consequences of high energy prices should be positive since energy shortages will lead to people questioning their habits and adopting non-fossil fuel technologies such as electric vehicles. They should also help to spur policy action and thus accelerate the development of renewable energy alternatives.

What's your view on greenwashing in the energy sector?

When it comes to communicating your investment credentials as an investor, the most important thing is transparency. To avoid greenwashing it is important to stick to the truth and avoid storytelling. The latter is all too common in sustainability reporting given that there is a desire to tell good stories. When we report on a company's impact, we look at its carbon data as well as footprint, check its factories' effincency, the structure of its supply chain and whether it manufactures products that avoid carbon. We also assess sustainability more broadly, meaning that we ask how companies treat their employees, how much water they waste as well as question their general impact on society. When there are areas in which the company is not best- in-class, we engage with the management and set goals which we monitor. Ideally, we would like to see all our portfolio companies reduce their carbon footprint each year.

How do you consider the dominance of ESG money in the context of the current valuation of ESG stocks?

There is neither a consistent definition for the term "ESG" nor what constitutes an environmental company. This means that we have to come up with our own definition. In our case this means, as mentioned before, that we only invest in companies that manufacture products and offer services that avoid carbon in a quantifiable manner. This provides us with a very broad investment universe, consisting of 1200 companies with a USD 12 trillion market cap across different geographies as well as sectors. When it comes to valuation, stocks that are recognised by many ESG indices can often be expensive. Last year we saw a strong rally in stocks linked to decarbonization although we continue to find companies which have significant exposure to decarbonization at attractive valuations. One example is the Chinese company Wuxi Lead Intelligence Equipment, the market leader for Lithium batteries in electric vehicles. According to the IEA Net Zero by 2050 report we need over 40 times more batteries to get to net zero carbon emissions. Wuxi as a producer of the latter is directly linked to that need and will give our fund exposure to a growing market.

Can you tell us more about the fund's engagement activities?

Generally, we engage with our portfolio companies by meeting them 4 - 5 times a year to carry out a detailed analysis. Sometimes emerging market companies find it challenging to integrate sustainability data into their reporting, so we have elaborate discussions with them on this topic. Generally, we intend not to influence and engage too much but instead try to ensure that the companies ultimately get there. However, if we find that conversations are moving too slowly or are not successful, we exit, which we have done in the past.

Can you explain more about the Global Environment fund's Exposure to China?

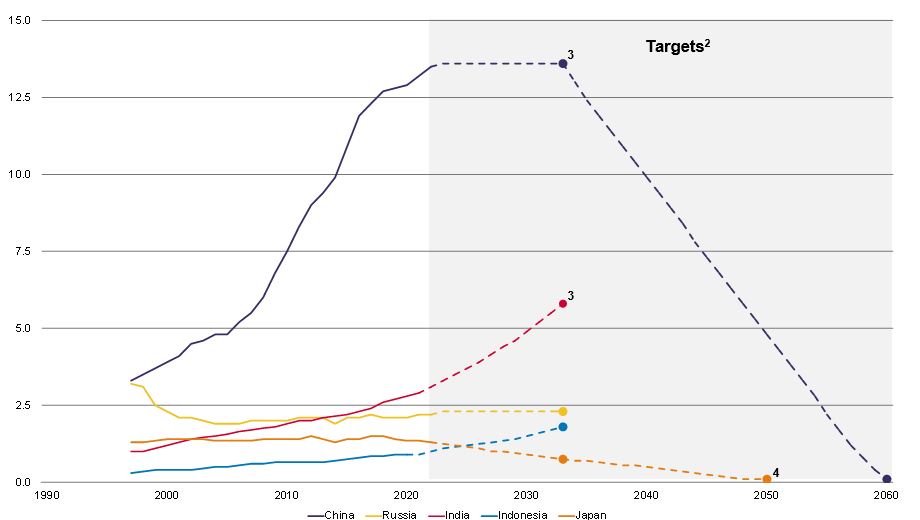

As a fund we look at the sources of global carbon emissions. The United States, the EU with its 27 member states as well as the UK produce less than 25% of global carbon emissions. According to the IEA, the Asia-Pacific region's burning of fossil fuels produced six gigatons ("GT") of CO2 in 1990, which represents about a quarter of the world total. In 2020, Asia emitted 16.5 GT which represents 49% of global emissions and China alone produced almost 30% of the overall emissions.

Greenhouse-gas emissions1, gigatonnes of CO2 equivalent

Source: Climate Action Tracker

Source: Climate Action Tracker

Notes:

1. Excluding forestry and other land use, except net-zero targets which include emissions removals from these sources.

2. When target is a range, central estimate is shown.

3. Multiple targets.

4. Unclear if this targets CO2 or all greenhouse gases.

As illustrated in the above charts, if we want to decarbonise our economies, we need to invest in emerging markets. China and other emerging markets form a critical part of the supply chain for global decarbonization through for example the production of solar panels and electric vehicle batteries. These markets pose an extraordinary decarbonization opportunity which in turn provides us with significant investment opportunities. Finally, it is worth noting that emerging markets did not create the climate problem. It is one which we have all inherited from the industrialisation of European and North American markets.

Do you believe in policy regulation or do you think that the market would eventually adopt and target climate issues sooner rather than later?

2021 is likely to see the largest annual increase in carbon emission since 1965. If you add up the emission plans of all countries attending the 26th UN Climate Change Conference of the Parties, it leads to a scenario with emission increases of 16% by 2030. If we are to manage a pathway to net zero, that number must go down by 45%. It is easy to get depressed by these figures but there is also plenty of room for positive surprises. To avoid a high exposure to regulatory risk, we prefer to invest in companies with a strong economic business case which are not reliant on government subsidies or elevated energy prices. To return to your question, regulation would not be necessary for the world to decarbonise if we had been quicker to tackle the issue. However, without global policy action the technological progress of consumer behaviour will not change in a way that gets us to a carbon-neutral world quickly enough.

|

An interview with Deirdre Cooper, Portfolio Manager of the Ninety One Global Environment Fund. Interviewed by our Investment Insights and the Fund Analyst team at Rothschild & Co Wealth Management, Switzerland & Germany. Please note that the views expressed in this interview are not made on behalf of Rothschild & Co. For more information on our Investment & Portfolio Advisory services please contact us. |

More Information