Wealth Management: Thematic Insights – The battle for streaming media supremacy continues

Amaya Gutiérrez and William Therlin, Wealth Management. Click here for the PDF version (467 KB).

When Neil Armstrong and Buzz Aldrin in 1969 left the Apollo Lunar Module Eagle and took those small steps on the lunar surface, millions of families cramped together in front of their dreamy televisions to watch history in the making.

At present, the ways in which we consume media and entertainment could hardly be more different from that Sunday in 1969. From black and white TV to colour, from single channel to cable, from few houses with one TV to plural, and, most recently, from fixed content to over-the-top streaming (OTT, see Uncovering TV lingo).

Netflix, founded in Scotts Valley, California in 1997, blazed a trail in the early 2000’s, when it changed shape from an online DVD rental provider to delivering video on demand online to paying customers. With the number of internet users growing by more than four billion in 20 years and the quality and speed of internet greatly improving, the OTT market has reached US$129.59 billion as of 2021 (Statista, Video Streaming OTT TV and video revenue worldwide, 2021, Statista.com). Central to this trend has been:

- The growth of smart phone and tablet use by households

- The tendency for consumers to unbundle the content they purchase

- The adhesive power of subscription models which have been central to accessing streaming platforms – see our separate article Subscribe and Stay. (Subscription-based or add-supported business models are the two most popular for streaming services.)

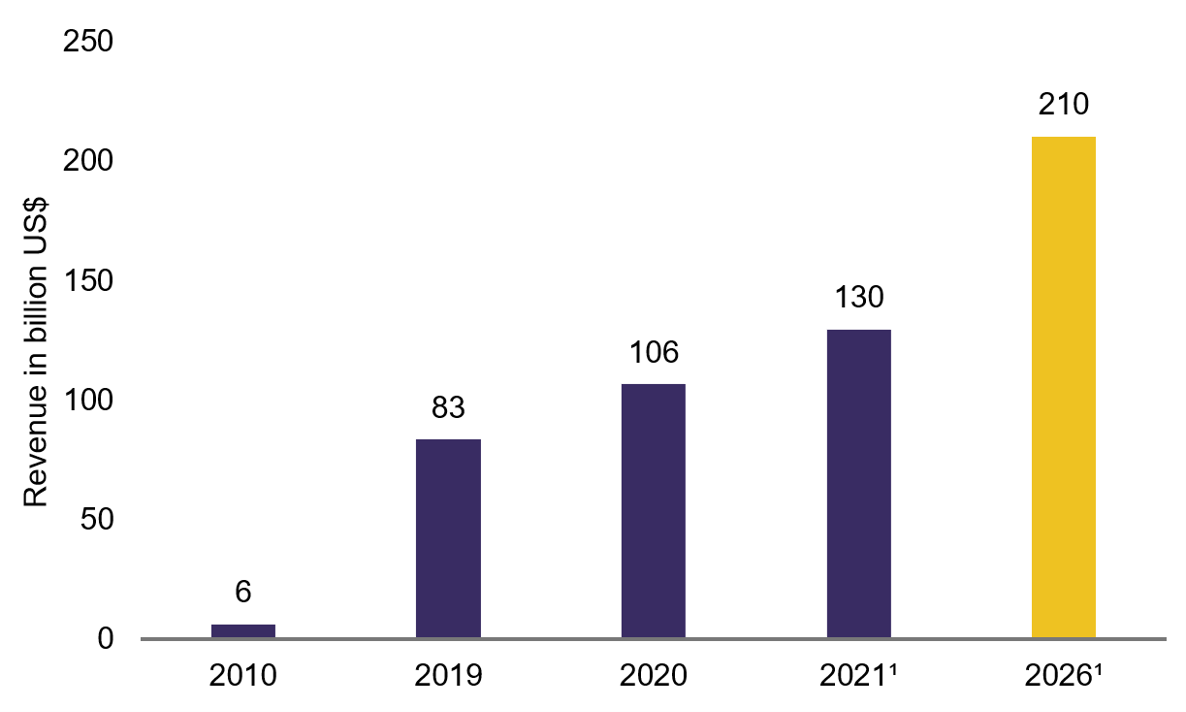

Given these three factors, the OTT market is now projected to grow 10% annually and set to reach US$210 billion by 2026 – supporting the thesis that growth is here to stay, see chart 1.

Chart 1: Worldwide OTT TV & Video revenue set to reach over US$ 200 billion by 2026

Notes

1 Forecast

2 Data prior to 2019 comes from previous reports

Source: https://www.statista.com/statistics/260179/over-the-top-revenue-worldwide/

Uncovering TV lingo

OTT refers to the content – subscription-based or ad-based – which is delivered on a digital platform to a final user, available via downloading or streaming (watch it online) at any time, on any device, anywhere in the world.

Long live the (content) king

The rise of OTT is changing the content landscape. The rapid success of Netflix, with over 200 million worldwide subscribers in some 190 countries, has triggered other media competitors to launch their own offerings. Unlike Netflix, many competitors view OTT services as just one of many revenue sources, such as Amazon. We observe two trends from this fragmented market:

- Firstly, distributors like Netflix are increasingly developing their own content such as The Queen's Gambit and My Octopus Teacher. As distributors become content creators, they risk losing third-party shows such as when Disney moved content off Netflix for exclusive streaming on Disney+ (more on Disney below).

- Secondly and because of the fragmentation of content, viewers often sign up to multiple OTT subscription platforms in order to access their favourite content. As of 2021, subscribers on average have four paid-for video streaming services (Deloitte Insights Digital media trends, 15th edition, April 2021, Deloitte.com), outlining the fact that consumers are open to multiple players in the market.

For providers and subscribers alike, the importance of hosting a broad range of high-quality content is quite naturally growing with increased competition. Providers competing for subscribers must therefore stand out to attract viewers and it comes as no surprise that content spend has increased dramatically having reached over US$105bn by the end of the last decade. Just looking at Amazon – it spent US$11 billion on content for its music and video streaming services in 2020, up from US$7.8 billion a year earlier. (Amazon 2020 Annual Report, 5 March 2021 Amazon 2020 Annual Report (PDF)).

A dynamic landscape

As mentioned, the OTT market has become increasingly diverse in recent years. In eighteen months, Disney+ reached over 100 million subscribers that enjoy access to content from Disney, Pixar, Marvel, Star Wars and National Geographic. Amazon, meanwhile, leverage their eCommerce business to entice Prime Video members. In 2021, Amazon agreed to buy Metro-Goldwyn-Mayer Studios for US$8.45 billion, noteworthy with the James Bond franchise in the catalogue. Finally, Apple launched Apple TV+, and a catalogue of original content, including collaborations like Sofia Coppola's On the Rocks or Oprah Winfrey's Book Club.

The power of data

Retaining and attracting new subscribers to these platforms have rich advantages beyond the immediate financial impact from the revenues generated. As an example, the 200 million worldwide Netflix subscribers each generate an abundance of data such as: how much time is spent on the platform, which content receives a thumbs up versus a thumbs down. Such invaluable datasets are essential in the process of purchasing and creating new content. Whilst it is impossible to say how many of the seven Oscars Netflix won in the 2021 Academy Awards can be attributable to its data, user data definitely played its part.

Streaming beyond the pandemic

With the pandemic creating stay-at-home captive audiences, one might wonder whether the brightest days of streaming services are behind us. The industry is still in search of an equilibrium, but the twin effects of increased internet usage and diversified streaming platforms have transformed both video and audio entertainment industries (for more on music streaming, see the sound of streaming box).

The Covid-19 legacy has for anything bolstered new subscriptions, podcasts, genres and platforms for consumers to enjoy. Consuming entertainment via these channels is forecast to remain strong, as the latest study by the United Talent Agency shows. In this survey, 67% of those exploring entertainment intend to spend more time, consuming online videos, movies and TV shows post Covid than they did before (Forever changed: Covid-19's lasting impact on the entertainment industry, UTA, June, 2021 Unitedtalent.com). As such, it seems that a post Covid world is a place for both online and offline entertainment – even when consumers once again are able to actively choose.

Investing in streaming

An industry still in search for its equilibrium, with an evolving offering and with different business models, our Investment & Portfolio Advisory team at Rothschild & Co's Swiss Wealth Management business can advise on the ways of gaining exposure to the topic of streaming.

Related Files

More Information