Wealth Management: Strategy blog – Going green

Strategy team: Charlie Hines

Recent articles have suggested that a ‘seismic’ shift to green investing has inflated the prices of sustainable assets. To some extent this is true; sustainability defined broadly to include environmental, social and governance has been a popular theme among investors, particularly in 2020 – but the focus of this, and the subsequent rise in valuations, has been confined to just one part of the ESG triplet.

Over the past year, ESG funds have accounted for a record $51 billion of net inflows from investors, and more than double the prior year’s total, according to Morningstar. By some margin, climate-related funds were the biggest beneficiaries - partly because the environmental impact can be objectively measured, but no doubt because the climate emergency is uppermost in most investors’ and governments’ minds.

Frustratingly, the premium paid for sustainable investments is empirically hard to measure. The index parameters and ethical definitions vary across institutions, and a lack of historical data makes it difficult to compare indices to long-term trends as well as to each other.

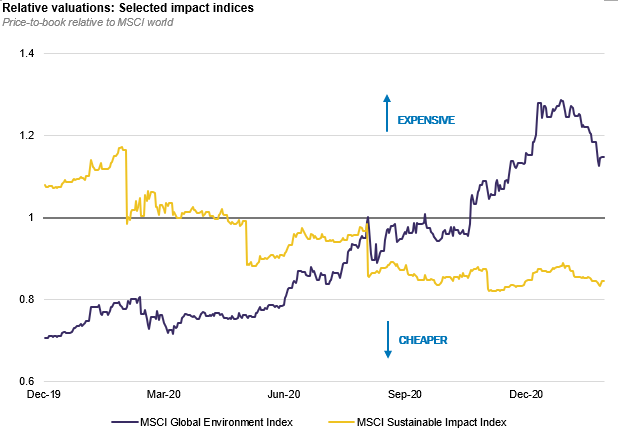

That said, more narrowly focused climate indices have become relatively expensive: “impact” indices – which includes companies that seek to have a positive environmental impact – have moved into even more expensive territory, relative to broader indices. Though top-down analysis here is somewhat compromised – short track records and the fluctuating composition of the more niche ESG benchmarks makes valuation comparison especially challenging.

Despite the various measurement challenges price-to-book ratios, which are less distorted by today’s special (covid-related) circumstances than earnings-based measures, indicate a clear investor preference for green (as opposed to socially or governance-oriented) investments, with valuations moving higher.

In the case of the MSCI Global Environment Index, where 50% of the companies derive their revenues from environmentally positive products and services, the price-to-book ratio has nearly doubled to 3.3x over the past year, while the broader global MSCI index has seen a comparatively smaller move (2.5x to 2.9x).

In contrast, the broader MSCI’s Sustainable Impact index, which incorporates companies that address social challenges, as well as environmental ones, has seen its price-to-book ratio decline over the same period.

Source: Rothschild & Co, Bloomberg

Composition is clearly making itself felt. Tesla, for example, makes up over one-third of the MSCI Global Environment and a more modest 6% of the Sustainable index. Whether this changes the interpretation is moot, however.

The more important question perhaps is whether sustainable assets warrant a premium, and whether it will last. As investors continue to tweak their benchmarks in favour of these assets, and supply lags behind, prices may continue to be squeezed higher.

The dynamics could shift as new sustainable funds enter the market, of course. In theory, vigorous enough government action might even eventually reduce that demand (we can but hope).

For the time being, however, we think the trend for sustainable investing will continue to grow with rising support for environmental and climate action at least. Careful due diligence, and an appreciation of exactly what goes into each index, is important. But for the time being, overall valuations, even where inflated by particularly high-profile stocks (which, as noted, may not be unreasonable anyway) do not yet look high enough to reduce that demand.

Disclaimer

Past performance is not a guide to future performance and nothing in this blog constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.