Asset Management Europe: Monthly Letter – January 2020

Marc-Antoine Collard, Chief Economist, Head of Economic Research, Asset Management, Europe

Economic environment

The wind of optimism that has been blowing amongst investors for several months was reinforced by how central banks implemented, rarely as synchronized, accommodative monetary policies, pouring a significant amount of liquidity into financial markets. Investors have also been reassured by how China and the US are on the verge of signing Phase 1 - resulting in the de-escalation of their trade dispute even if the conflict is far from resolved - as well as the UK election results, where Boris Johnson won an overwhelming majority, allowing his Brexit Withdrawal Agreement Bill to clear the House of Commons.

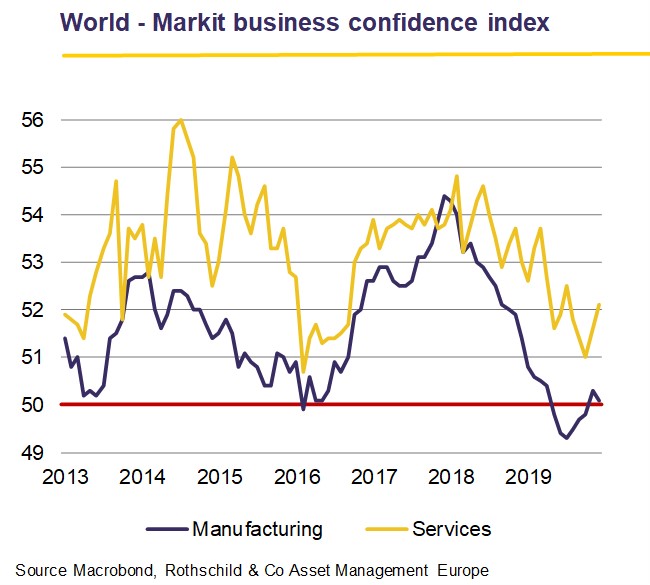

Leading economic indicators published in recent weeks have nevertheless sent mixed signals. After an upturn that began in August, business confidence in the global manufacturing sector remains depressed, returning to its downward trend. This decline is at odd when compared to the strong rise of the stock markets, the perennial weather vane of investor optimism. However, business confidence in the service sector rose for the second consecutive month in December, reaching a high since last summer and continuing to withstand the persistent headwinds from the weak manufacturing sector.

Click the image to enlarge

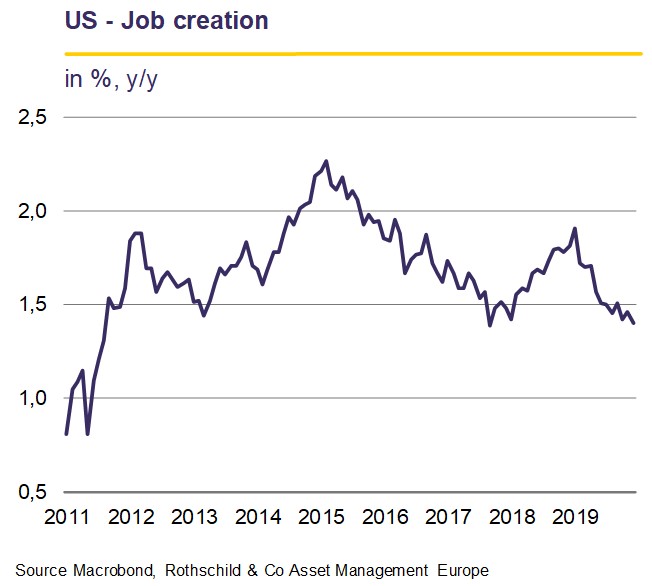

This dichotomy is particularly glaring in the US, where the ISM manufacturing index sank further into recession territory, registering its lowest level in a decade while, conversely, morale in nonmanufacturing companies remained healthy. The US labour market ended 2019 with less momentum as job gains (145,000) cooled more than expected and wages rose at the weakest pace (2.9% y/y) since 2018, despite the unemployment rate (3.5%) remaining at a half-century low.

Click the image to enlarge

After three successive cuts in its Fed funds rate - justified by trade tensions, weak business investment and an unfavourable international context - the FOMC kept its rate unchanged at its last meeting in December. The question now is, how long will the status quo last? The weakness of inflation and the risk of de-anchoring inflation expectations have convinced the majority of members to adopt a cautious approach. What's more, Fed Chair Jerome Powell has recently stressed that any rate hike must be preceded by persistent and above-target inflation. Soon to celebrate his second anniversary at the head of the Fed, Mr. Powell will thus have completed a remarkable metamorphosis, adopting a tone much closer to his predecessor Janet Yellen who, during her mandate, opted for a cautious and patient approach. As a result, in the absence of a major event, the monetary status quo in the US is expected to last for some time.

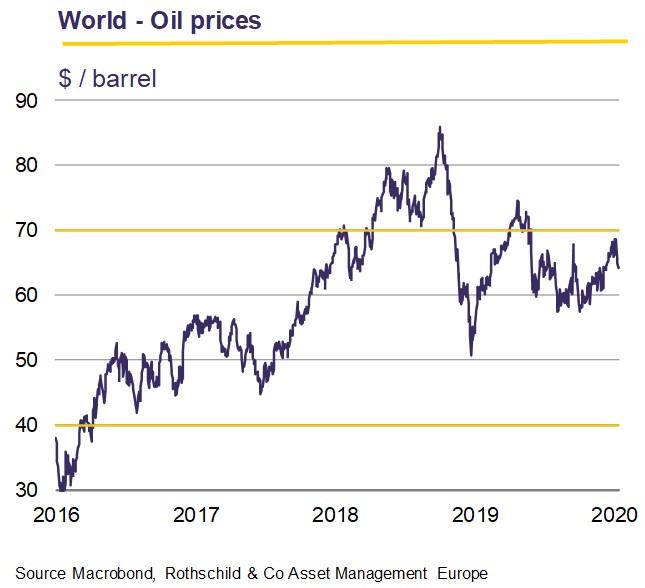

As the Sino-American trade war entered a lull, the Middle East experienced a rise of geopolitical tensions caused by the death of the Iranian general, Qassem Soleimani, in an American drone strike and Iran's response, which was to launch missiles on US military bases in Iraq. For now, President Donald Trump has chosen to play the game of calm, but his future decisions are likely to be influenced foremost by the imperatives of an election year. Considering the Middle East's leading role in the energy sector, price volatility could be significant and a jump in the price of oil could severely penalise the world economic outlook.

Click the image to enlarge

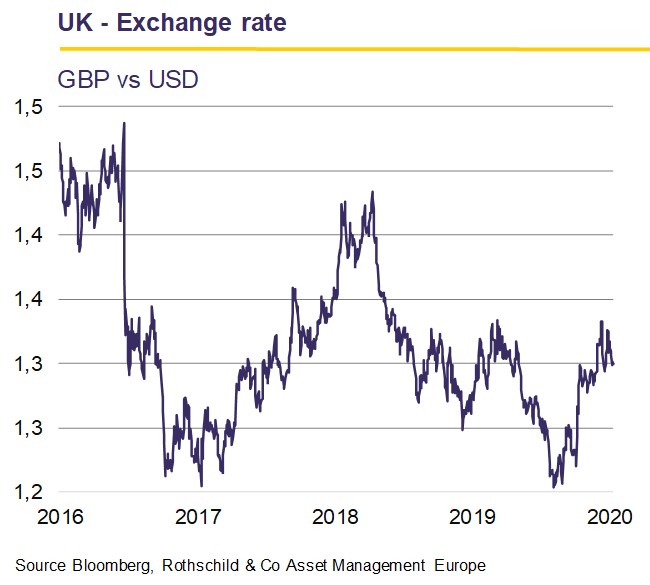

Meanwhile, after January 31, the European Union (EU) and the UK will enter a transition period. The UK will officially cease to be part of the EU and lose decision-making powers within the bloc, but will continue to apply European rules and benefit from it. The two parties will have until the end of 2020 to agree the terms of their future commercial relationship. However, finding an agreement in just eleven months will be a challenging task. In addition, Boris Johnson insists that he will not negotiate beyond 2020, should more time be needed for negotiations on future relations, even though the transition can be extended, once, until 2022.

Johnson aims for an ambitious trade deal, although refusing at the same time to align with EU rules. In fact, faced with this tight schedule, the UK government has hinted that it could settle for a partial agreement if no comprehensive agreement was reached by the end of the year. Yet, the new Commission President, Ursula von der Leyen, has been clear that fair competition in the fields of environment, labour, taxation and state aid were necessary conditions for the UK to have continued access to the Single Market. The EU has begun work to define its red lines and objectives in the negotiations, which it will present to the Member States. The EU has also said it would continue planning for the possibility of no deal at the end of 2020 - an eventuality which could again threaten serious economic disruption. One thing is certain: Brexit is far from being resolved.

Click the image to enlarge

Overall, despite a struggling industrial sector and moribund global trade, global economic expansion did not stop. That said, 2019 saw the weakest economic growth since the Global Financial Crisis, and growth is largely moving sideways at sub-trend levels. After reaching a peak last summer, the likelihood of a recession has receded and market participants have priced in a marked global rebound. However, the magnitude of the upturn is contested. The latest World Bank Global Economic Outlook anticipates only a marginal rebound, concentrated in a handful of countries - Argentina, Brazil, India, Iran, Mexico, Russia, Saudi Arabia and Turkey. What's more, indebtedness around the world, which is growing at its highest rate in 50 years, is clouding the economic outlook. Therefore, the institution still believes that downside risks predominate. Not enough, it seems, to raise investors' eyebrows.

Download the PDF version Monthly Letter (635 KB)