Asset Management Europe: Monthly Letter – November 2019

Marc-Antoine Collard, Chief Economist, Head of Economic Research, Asset Management, Europe

Economic environment

The reverberation of the 2018-19 slowdown has been broad-based across countries - including the US - and recent macroeconomic data suggest that weakness in business investment and manufacturing could broaden to a slowdown in consumer spending and service sector growth through softer labour markets. That said, confidence in a 2020 growth rebound, in the wake of fading geopolitical tail risks and the effective transmission of central bank easing to global financial markets, has gained momentum among market participants.

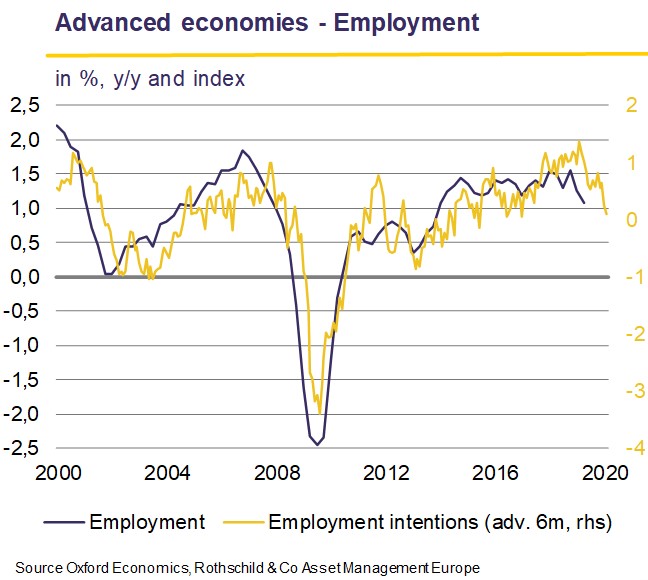

Click the image to enlarge

According to the latest Markit business confidence survey, the global manufacturing sector contracted for the sixth successive month in October, although the small improvement observed in the past three months has been interpreted as a further sign that the downturn in the global industrial sector may have bottomed out last July. Two factors are particularly worthy of being highlighted. First, part of the uptick may be explained by firms increasing their inventories to pre-emp the rise in US tariffs - initially supposed to take hold in mid-October and again in mid-December - thus temporarily boosting demand. This would explain the upward inflection in the production sub-component. Second, most of the improvement has been concentrated in a handful of countries, most notably China. From June to October, the Chinese Markit index rose 2.3 points to 51.7, a two-and-half-year high. Interestingly, the manufacturing PMI, released by the Chinese National Bureau of Statistics, fell to 49.3 in October (lowest since February 2019), with sentiment remaining in negative territory for the sixth month in a row. Even if there have been occasions in the past when the gap between these two surveys has been as wide, rarely has the trend been so different.

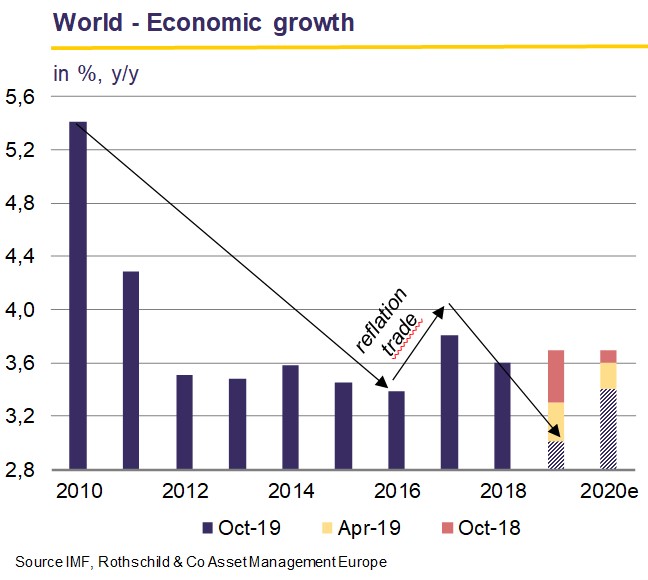

Click the image to enlarge

The Sino-US discussions remain ambiguous and the comments from each side are difficult to reconcile. The two countries seem on the verge of signing a draft agreement - 'Phase 1' - where China would commit to increase substantially its purchases of agricultural commodities, while the US would postpone the rise from 25% to 30% on customs duties on USD250 bn of imports. Phase 1 would allow both sides to obtain, in the short term, a favourable outcome. China's food inflation surged 11% in September, the fastest pace in nearly eight years, and a boost in agricultural imports is timely. For his part, President Trump will be proud of his victory, especially as his Presidency's approval rating has suffered due to the scandal related to Trump allegedly pressuring his Ukrainian counterpart to open corruption proceedings against one of his opponent to the Presidency. An impeachment procedure, increasingly supported by voters, is under consideration. Yet, while it is in the interest of China and the US to come to an agreement, Phase 1 is trivial compared to other enormous obstacles, particularly on intellectual property issues and the monitoring process of any deal. Comments by Chinese leaders suggest that the discussions are moving slowly and that they are not confident on achieving a broader agreement.

Click the image to enlarge

Indeed, China is calling for the cancellation of tariff hikes planned confidence index for next December and is seeking to roll back tariffs on as much as USD360 bn of Chinese imports. However, the US fears that by loosening the clamp of customs barriers, the Chinese authorities will no longer be encouraged to keep its commitments. Adding to the fragility of the recent truce of the Sino-US trade war, the Brexit saga continues as the EU granted a “Flextension” until 31 January 2020. Faced with Parliament's inability to endorse the draft Withdrawal Agreement negotiated by Prime Minister Boris Johnson, MPs finally decided to give voters the say on December 12. At present, the Conservative Party (36%) leads the Labour Party (24%), whose leader Jeremy Corbyn wants to renegotiate the draft agreement, which, as it stands, would minimise future ties with the EU while raising the questions about the UK's territorial integrity due to the differential treatment of Northern Ireland. For their part, theLiberal Democrats (18%) want to cancel Brexit, and are supported by the Scottish Nationalist Party (4%), while the Brexit Party (11%) advocates a quick exit, with or without agreement. If the Conservative Party stands a good chance of winning this election, its intentions regarding the Withdrawal Agreement are unclear. In addition, the possibility of a hung parliament, unable to reach an agreement with the EU, cannot be ruled out.

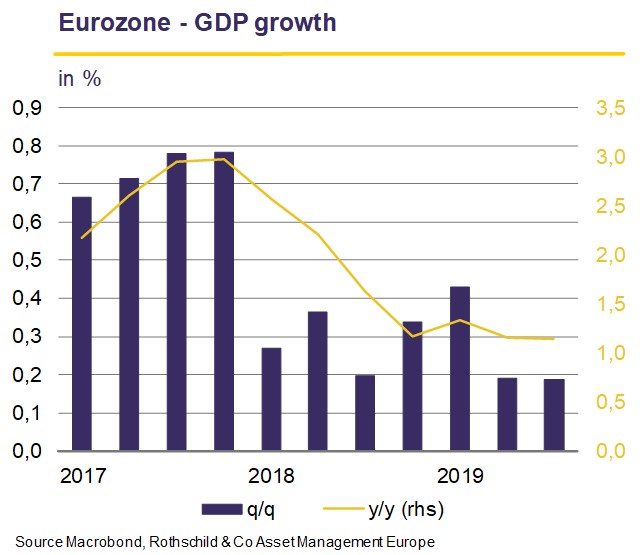

Meanwhile, fading tail risks and hints of stabilisation in activity are no doubt influencing thinking at central banks. The US Fed has delivered three rate cuts - versus three hikes expected a year ago - and the need for further accommodation is no longer obvious. By contrast, inaction continues to rule the Bank of Japan (BoJ) despite weaker growth, lower inflation, and depressed inflation expectations. As for the ECB, the eurozone's expansion remains lacklustre - 0.2% q/q in Q3 2019, in line with Q2 growth and recent surveys - but the tentative tick up in the eurozone core inflation may also promote caution, especially if the renewed optimism keeps financial markets climbing. Thus, a key question is the extent to which the latest tempered easing from the Fed, the BoJ and the ECB will affect central banks in emerging markets. For the highyielding countries, these shifts are likely too subtle to discourage expected future easing, unless currency depreciation against the dollar continues. For the lower-yielding economies, however, these signals could temper projected rates cuts in the coming months.

Click the image to enlarge

Overall, recent economic and geopolitical news have solidified the consensus view that the global expansion will survive the tug-of-war between negative geopolitical shocks and positive policy supports, and, in so doing, return to stronger growth in 2020. Nonetheless, uncertainty remains as to how much of the recent stabilisation/improvement in business sentiment surveys is due to temporary factors, not to mention the long-running debate over the merits, efficacy and risks of monetary easing in a world of alreadylow rates and elevated central bank balance sheets.

Download the PDF version Monthly Letter (633 KB)