Accumulating assets as a partner

Background

Our client is a partner at a UK magic circle law firm. She is 40, married with two young children.

Having joined the partnership at 37, she bought her dream home shortly afterwards.

Key objectives

Our client was keen to put a plan in place to pay off her mortgage, pay the school fees for her children and make consistent investments over her career for an enjoyable retirement.

Understanding our client

At the outset, we wanted to get a strong understanding of her current financial position. Using our ‘Wealth Framework’, we were able put her assets into ‘pots’ which not only gave her a better view of her wealth but also identified some areas where she may want to take action. Her well-earned promotion to partner was a major career milestone but also added complexity to her income and employment status. We identified three areas to consider as she planned her wealth:

Pension considerations when self-employed: on becoming a partner, our client became self-employed, which had implications for workplace pensions accrued from her time as an employee.

Mortgage repayment considerations: our client had taken out a large mortgage and moved into a new property. She wanted to know whether it was better to repay the mortgage early or to invest more in her portfolios.

Planning for tax bills: as she is now self-employed, she is required to personally pay her tax bills to HMRC. She needs to keep enough liquidity in her assets to meet these liabilities.

Solutions and options

Having received a clear picture of our client’s financial situation, current challenges and aspirations, we started to build out some options for a plan. We:

- Created a cashflow planning model to show the impact of various financial decisions such as timing early repayment on her mortgage versus investing, paying for her children’s school fees, and designating cash to cover estimated tax bills (due in January and July).

- Proposed an approach to manage her short-term liquidity using high-interest baring accounts and liquidity funds made up of a range of gilts. We arranged the short-term liquidity strategy to meet two goals: cover mortgage overpayments and to pay estimated tax bills.

- Simplified and organised her wealth by transferring her employer pension to a self-invested personal pension, invested school fees via a lower risk portfolio, and set up a designated tax account where gilts would mature with each tax bill with the funds going directly to HMRC.

Outcome

As a result, our client now feels like he has a much better understanding of his plans to retire and aims to diversify the risk of his private assets by investing further in his family’s Nest Egg.

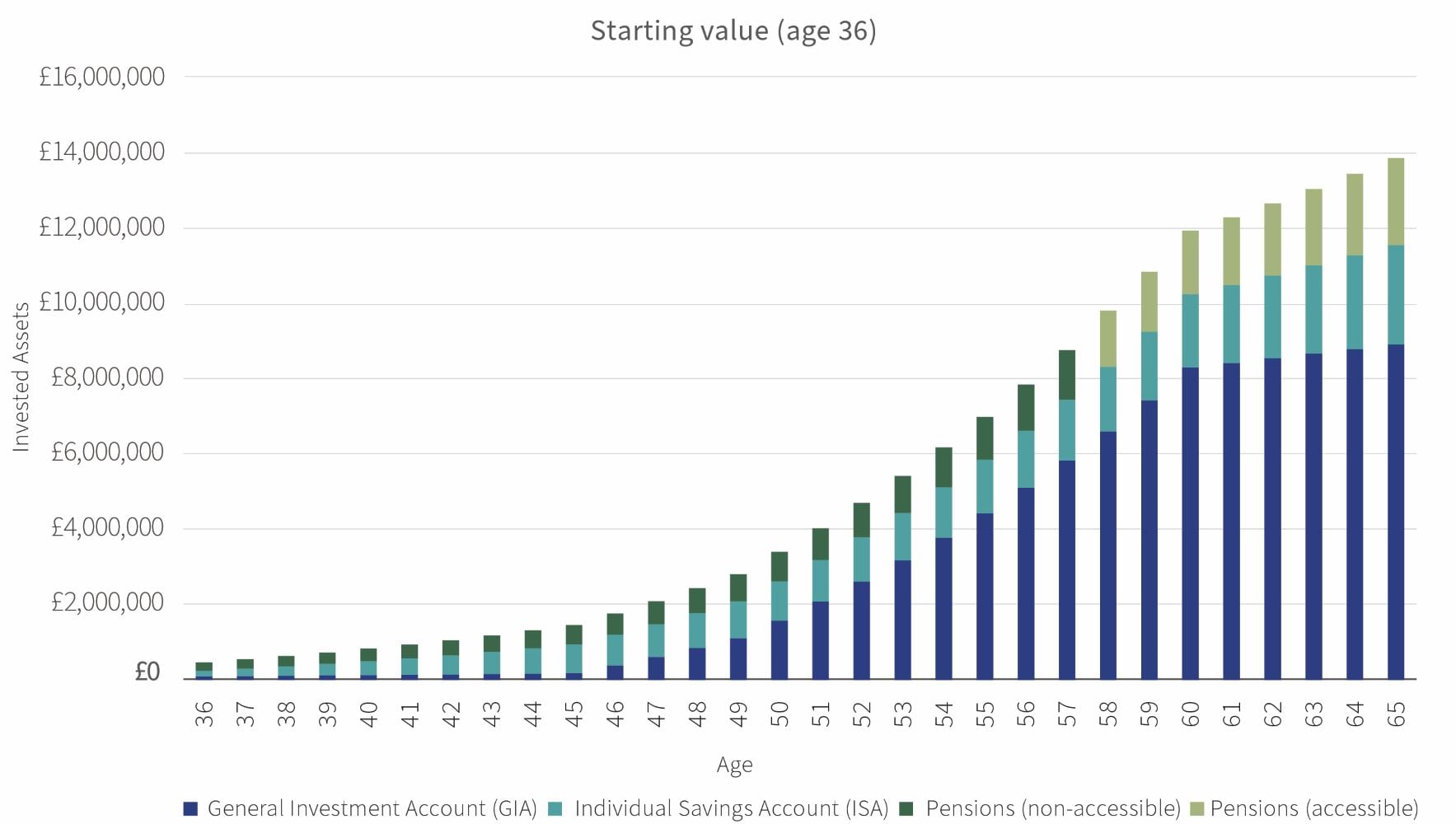

Cashflow modelling for a UK Magic Circle Partner

| Assumptions | GIA | ISAs | Pensions (Non accessible) | Pensions (Accessible) |

| Starting value (age 36) | £200,000 | £100,000 | £200,000 | £0 |

| Performance (balance for illustration) | 6.24% | 6.24% | 6.24% | 6.24% |

| Inflation | 2.00% | 2.00% | 2.00% | 2.00% |

Source: Rothschild & Co, Bloomberg Data from 31 December 2002 to 31 December 2024.

The New Court Fund GBP inception date was 14 July 2015. Performance for periods prior to inception date is the Rothschild & Co Wealth Management UK Ltd GBP Balanced composite, adjusted to reflect the fund's 1% annual management charge and 0.06% operational costs. Performance data is net of fees. Data post 30 September 2007 is net of actual client fees incurred. Data prior is actual gross performance less current average client fees.

Past performance is not a reliable indicator of future performance and the value of investments and the income from them can fall as well as rise.

The above graphs are for illustrative purposes only. The information above is not intended and should not be construed as tax advice. Each investor should seek their own independent tax advice