Supply chains: state of play

“I always say ‘tariffs’ is the most beautiful word to me in the dictionary” - Donald Trump, 20 January 2025 inauguration

Global supply chains have experienced several shocks in recent years, including a pandemic and war, but have so far proved resilient. The latest threat is Mr Trump and his tariff agenda, a bigger threat than in his first term and one which, as we note below, has already affected world trade.

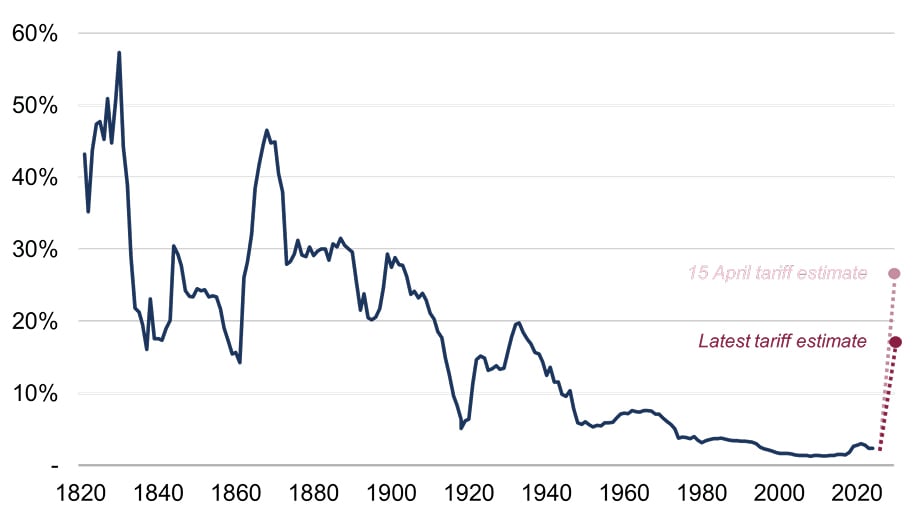

1. Trump’s proposed tariffs mark a major break with the recent past

Following the ‘Liberation Day’ tariff announcements on 2 April, the US tariff rate was headed for its highest reading in over a century. Country-specific tariffs were however then postponed for 90 days on 9 April, as was the 145% China tariff on 12 May, and so the overall ex ante (or proposed) US tariff rate currently looks to be around 15-20%. This is roughly 10 percentage points below the ‘Liberation Day’ plans, and could turn out a bit lower if import behaviour changes, but it is still the highest rate since the Smoot-Hawley tariffs of the 1930s.

Figure 1: Effective US tariff rate on total imports and today’s ex ante proposal

(%)

Source: Rothschild & Co, U.S. International Trade Commission, U.S. Census Bureau, The Budget Lab at Yale

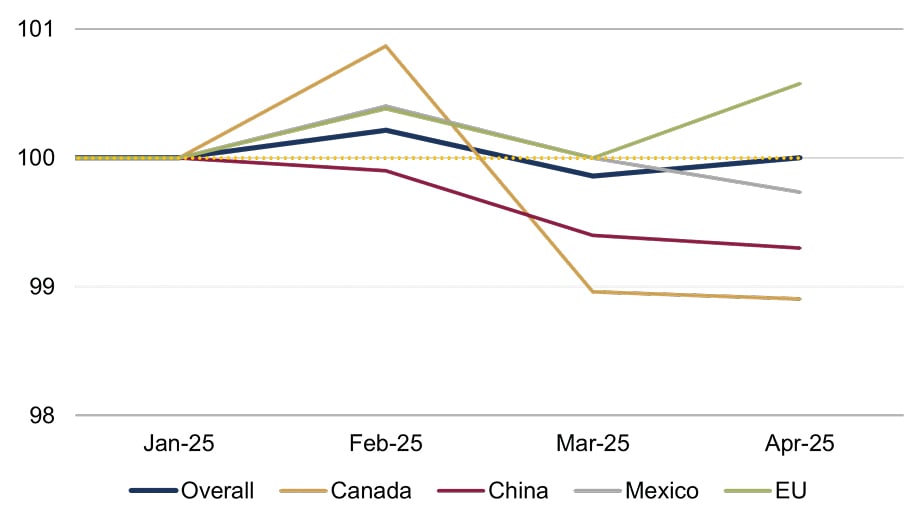

2. Exporters to the US may start to absorb a little of that higher cost

US consumers are most likely to bear the costs of higher tariffs, but may not do so alone: exporters to the US, realising that their products will be made more expensive, might cut their selling prices to avoid losing market share. As yet, there is little sign of this happening. US import prices, which are recorded before tariffs are added, have been flat through this year (as of April, which admittedly may be too soon for any effect to show up). That said, the prices of imports from Canada, Mexico and China, all of whom were tariffed earlier in the year, have fallen, suggesting this pattern may yet emerge for other countries’ exports to the US. It’s also possible that some of the higher costs will be borne by US distributors – including the companies arranging the imports – before being passed onto the final buyer and showing up in consumer price indices. The US CPI for April was if anything softer than expected, but again it may simply be too soon to expect the tariffs to show up.

Figure 2: US import price index by country/region

Rebased indices (January 2025 = 100)

Source: Rothschild & Co, Bloomberg, US Bureau of Labor Statistics

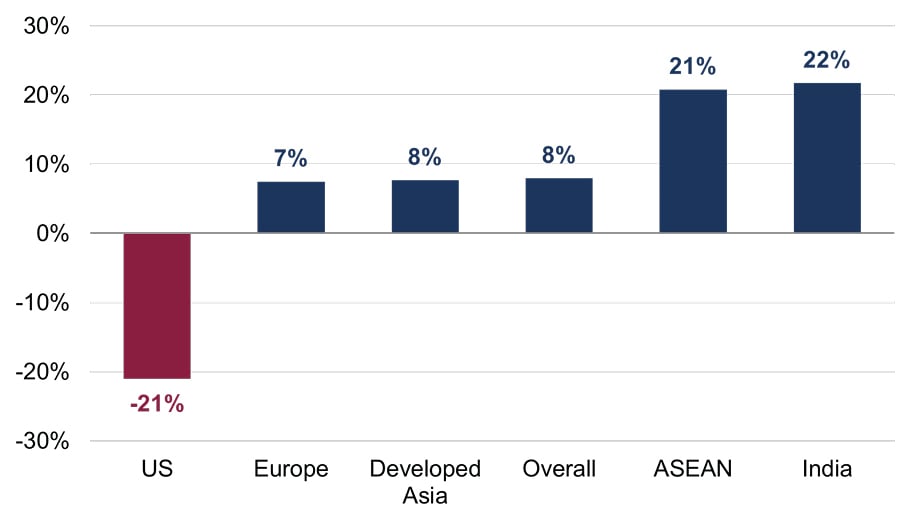

3. China exports to the US slumped in April, following the spike in tariffs…

China’s exports to the US, as recorded by Chinese data, collapsed by a fifth in April (relative to the prior year) after Trump raised its tariff to 145%. Even so, overall exports were up by almost a tenth, with exports to nearby countries – such as the ASEAN cohort and India – rising notably. There were few signs of significant dumping in Europe in April, though if the US’s lower tariff on Chinese goods proves to be temporary then the likelihood of that behaviour might increase.

Figure 3: China exports by country/region in April

Year-over-year change (%, USD)

Source: Rothschild & Co, Datastream, China Customs. Note: Developed Asia is Japan, Singapore, South Korea and Taiwan. Europe is the EU and UK.

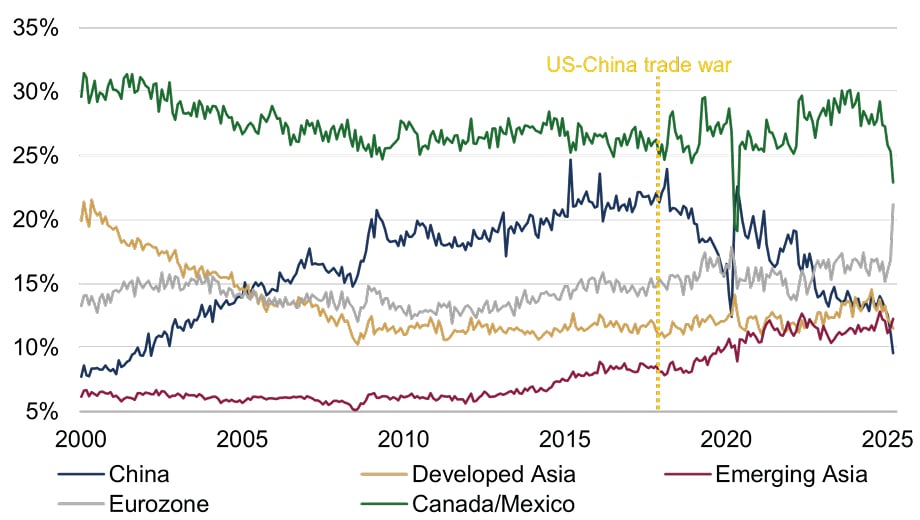

4. … but trade may continue to be re-routed in the months ahead

US import behaviour was highly unusual in March ahead of the ‘Liberation Day’ tariffs. Notably, the proportion of imports from the euro area surged, likely because its other major trading partners had already been subject to extra tariffs at that point. As noted above, the import share from China slumped, to below 10% – the lowest reading in more than two decades. However, some of that China trade has likely been re-routed to nearby countries – rather than re-shored – as a rise in import shares from Developed and Emerging Asia have partly offset the decline in China since Trump started his trade skirmishing in 2018.

Figure 4: US goods imports share by country/region

Total imports (%, USD)

Source: Rothschild & Co, Rothschild & Co, Datastream, U.S. Census Bureau. Note: Developed Asia is Japan, Singapore, South Korea and Taiwan. Emerging Asia is India, Indonesia, the Philippines, Malaysia, Myanmar, Thailand and Vietnam.

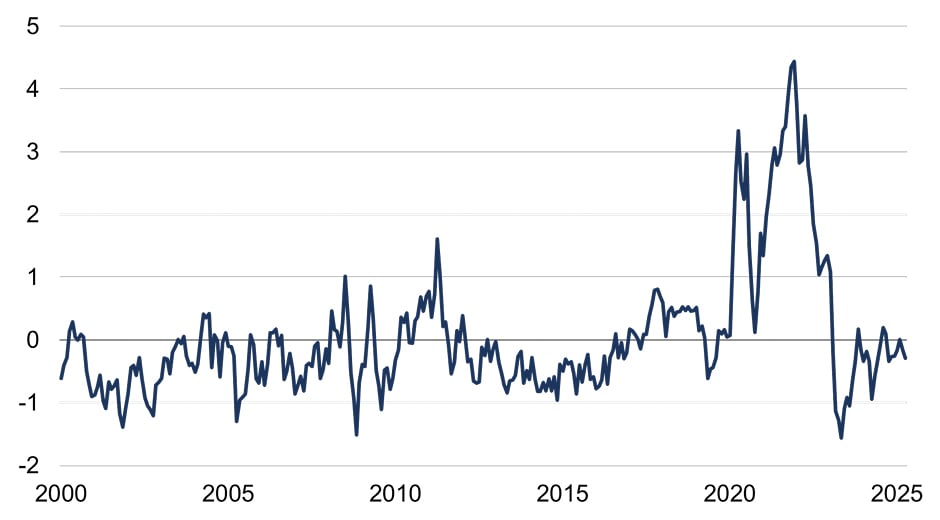

5. Overall, supply chain conditions seem normal

Despite the heightened trade uncertainty and unusual shipment patterns, supply chains on balance appear healthy. The New York Fed’s Global Supply Chain Pressure Index, which aggregates transportation cost data and supply chain-related components from the Purchasing Managers’ Index, suggested normal conditions in April. Moreover, the IMF’s PortWatch Monitor reported that world maritime trade volumes grew by close to 2% in April (in year-over-year terms, though it takes the three-month moving average). There are of course pockets of stress in the system – for example, shipping activity near Ukrainian ports and also the Red Sea remain subdued – but there are so far remarkably few signs of major supply chain stress.

Figure 5: Global Supply Chain Pressure Index

Standard deviations from average value

Source: Rothschild & Co, Bloomberg, Federal Reserve Bank of New York

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.