Growth Equity Update

May 2026 – Edition 50

- UK launches Sovereign AI fund: ‘The speed of venture. The strength of a nation’. The newly launched Sovereign AI fund is a £500m investment vehicle backed by the UK state and intended to invest in and support British AI companies. It will also offer access to the UK’s national AI supercomputing infrastructure, potential fast track visa decisions for key staff and access to government data and early procurement opportunities.

- Supports the Ineffable Intelligence seed round: Sovereign AI, and the British Business Bank, supported Ineffable Intelligence’s $1.1bn April seed round at a valuation of $5.1bn - one of the largest ever seed rounds in Europe. Founded in late 2025, Ineffable Intelligence aims to develop AI systems through reinforcement (trial and error) learning.

- NASDAQ rule changes: We review the potential impact of two key interlinked changes to the NASDAQ listing rules introduced in May - no minimum free float and fast index inclusion – which are likely supportive for the prospects of major tech related IPOs in the pipeline in 2026/27.

- Venture Capital – Buoyant markets, but what if you are not an AI or related business? ‘The top 1% of companies by valuation now absorb a third of all venture capital deployed. The bottom half get 7%, technically “venture-backed” but also kind of like sitting in the parking lot at a concert and claiming you saw the show’’. - Lux Capital. We assess the data and find that, in the US, venture funding for companies in non-AI ‘Other sectors’ rose by 64% or $41bn in 2025 and by 38% 2023-25 in Europe. The rising tide is lifting all ships.

- Another strong month in April: In Europe 43 rounds of $20m+ raised a total of $5.9bn in April, up 156% yoy and 75% ytd. In the US the $35bn raised in April in $100m+ deals, was up 4.1x yoy with the ytd date total up 3.6x.

- Pipeline of c$82bn. Of which $74bn is in US deals, including a potential $50bn for Anthropic at a $900bn valuation, and $8bn in Europe led by $2bn each for Poolside and Neura Robotics.

- Public markets – Earnings outweigh geopolitics: Since March 30 NASDAQ is up 26% and the S&P500 17% with a strong and broad Q1 earnings season driving up full year S&P500 earnings expectations to 20%+ and year end S&P strategist targets to over 8,000.

Download a PDF version of the Growth Equity Update

UK launches a sovereign AI fund

'The speed of venture. The strength of a nation'

At the start of April, the UK government launched the latest in a series of initiatives designed to support early-stage growth companies. This most recent programme is Sovereign AI, a £500m investment fund backed by the state and intended to support and invest in British AI companies.

Liz Kendall, Technology Secretary at the Department of Science, Industry and Technology stated at the launch:

‘We are backing our brilliant innovators and entrepreneurs, so we seize the benefits of AI to reshape Britain for the benefit of all. Sovereign AI is unlike anything government has ever done before. Its unique approach will help break down the barriers that have too often held back British enterprise and innovation. This is how we ensure Britain’s economic prosperity and national security in the modern age.’

As described at its launch

Sovereign AI is designed to be different from any previous government-backed unit, acting like a venture capital fund with the muscle of the state behind it – moving fast, backing ambition and cutting through the red tape that so often holds brilliant ideas back. It will invest directly in the UK’s most promising AI start ups, help them scale quickly, and give them the support they need to compete with the best in the world.

The intention is that Sovereign AI will operate at the pace of a venture capital firm. The fund will invest in businesses directly with a typical cheque size of £1m-£10m. It will also offer support that goes beyond funding. Given the scale of potential investment in AI firms relative to the £500m resources of the fund, this is probably the most significant element of the package.

The Sovereign AI initiative will offer

Compute capability: Fully funded access to the UK’s largest AI supercomputers, with up to one million GPU hours available per start up - providing the capability needed to help train state of the art AI models. The sovereign AI unit provides access to the UK’s national AI supercomputing infrastructure through the AI Research Resource (AIRR), including systems like Isambard-AI and Dawn. Capacity stands at 5,500+ GPUs today and is set to scale 20-fold by 2030, with an additional £250m of cloud credits available from later this year.

Fast-track global talent: Every company receiving investment will get visa decisions within a working day, plus access to an initial ten cost-free visas for the ‘world’s top R&D talent’ to come and work for them in the UK.

Government support: Help navigating access to data, early procurement opportunities, independent product validation and routes into new approaches to regulation. As part of an integrated approach government will act as an early customer to help validate novel AI solutions and de-risk investment for the wider market.

The Chair of Sovereign AI is James Wise, a partner at Balderton Capital with a particular focus on AI, energy and health technologies. He heads the small team of investment partners at Sovereign AI.

As ever the hope is that the assistance of the Sovereign AI fund will attract further private capital to help fund and scale start-up businesses. The government cites the UK Investor Partnerships programme which claims that £100m in public grants has leveraged £1.25bn in private follow-on capital.

The first investment announced by Sovereign AI has been in Callosum, an intelligent systems company combining chips and compute architecture to build more effective AI systems capable of running on a mix of hardware. The company raised a pre seed round of $10m in February 2026 led by Plural. It has now received an undisclosed level of equity funding from Sovereign AI.

A further six start ups (Prima Mente, Cosine, Cursive, Doubleword, Twig Bio and Odyssey) will receive access to the AIRR supercomputer network – with Sovereign AI getting a right of first refusal on future investments for a number of the recipients. Sovereign AI is in discussions with another 30 firms over potential AIRR access.

The most high-profile investment by Sovereign AI so far is its investment in Ineffable Intelligence, a UK company founded in late 2025 and led by David Silver, previously head of the reinforcement learning team at Google DeepMind and a Professor of Computer Science at UCL. Ineffable is developing AI systems that develop through reinforcement learning. Its seed round of $1.1bn at a valuation of $5.1bn in April was led by Sequoia and Lightspeed. NVIDIA and Google participated and so did the UK Sovereign Fund alongside the British Business Bank. The UK Sovereign Fund observed

‘We will invest directly in promising UK AI companies to help them scale in the UK. Our investments will be focused on companies at the early and growth-stage. Typical equity investments will be worth around £1-10 million, though every company’s circumstances will be different.’

https://www.sovereignai.gov.uk/

New NASDAQ trading rules

No minimum free float and fast index inclusion are key changes

2026-7 is likely to see an interesting transition period as several of the major, previously privately funded, US growth companies seek IPOs. It is widely reported in the press that SpaceX, OpenAI, Anthropic and others are contemplating IPOs in 2026 or early 2027.

These are big companies. Reuters reports (April 8, 2026) that SpaceX is seeking a $1.75 trillion valuation, which would make it the sixth largest listed US company. Open AI’s last private round was conducted at an $850bn valuation. Anthropic is said currently to be raising $50bn at a $900bn valuation.

According to press reports (FT May 1st, 2026) Space X plans to sell an initial $75bn of stock which, based on its widely reported possible valuation of $1.75trn would represent 4.3% of its equity.

Recent rule changes at NASDAQ may potentially smooth the arrival of such vehicles onto the market. The rule changes took effect on May 1, 2026. The key elements are:

Fast entry: Early entry to the NASDAQ Index potentially accelerates passive fund buying

- Hitherto large cap newly public companies have been added to the Nasdaq -100 index (NDX) at the time of the annual reconstitution of the index, which takes place in December of each year. Typically, companies would have to have traded for at least three months to be considered for inclusion at that stage. Thus, a company floated in June would need to wait for the December reconstitution to enter the index. A company floated in October might have to wait until December of the following year for inclusion.

- Under the new rules, large cap recently listed businesses will be eligible to move into the NASDAQ 100 index, as long as they are in the top 40 by market capitalisation, after just 15 trading days. There is no need to replace an existing NDX constituent. The index can temporarily have more than 100 constituents until the next reconstitution.

Free float rule: No minimum free float introduced

- Unlike many other indices, the Nasdaq-100 uses listed market capitalization for weighting rather than float-adjusted market capitalization for weights. This approach is designed to ensure that the index remains focused on the largest companies on Nasdaq, without overemphasizing public float.

- From June 2024 NASDAQ introduced a 10% minimum float rule for index inclusion. A company with less than 10% free float would be automatically excluded from the index.

- NASDAQ’s view is that float is a subset of market capitalization. As a result, all index members are already represented at a multiple of their float. For fully floating securities, float and market capitalization are equal- a multiple of 1x. For securities at the previous 10% float minimum level - the multiple was 10x.

The changes

- NASDAQ’s new rules remove the minimum free float requirement.

- Index weighting is now capped at three times a security’s free float – the 3x float cap. Securities with float above 33.3% are weighted using their full, eligible listed market capitalization. Those with floats below 33.3% are weighted on a multiple of 3x their free float.

- In practice this means that for a company with a 21% float, its weighting would be (21% x 3) 63% of its listed market value; for a 19% float company, the weighting is (19% x3) 57% of its listed market value. For a 5% float company the weighting is (5% x 3) 15% of its listed market value.

What are the implications? This means that if the owners of a company about to undertake an IPO want to release just a small amount of equity – say 5% - they can do this and the company will still be included in the NASDAQ 100 Index assuming the top 40 size criteria is met

The likely impact of these rule changes is:

- The threshold for a company to rank in the top 40 constituents of the NASDAQ-100 (NDX) is a c$100bn market cap. All of SpaceX, OpenAI, and Anthropic, based on their most recent funding round valuations, would easily reach this criterion.

- The IPOs of such companies can be conducted, if desired, with a free float of less than 10% with these companies still being eligible for inclusion in the NASDAQ 100 index.

- These companies would be eligible to enter the NASDAQ 100 almost immediately post IPO. Instead of waiting for multiple months and potentially over a year for inclusion, these new IPOs would be eligible to enter the NASDAQ 100 index just 15 trading days post IPO.

These rule changes may potentially underpin the IPO processes of big upcoming flotations where the sale of less than 10% of the equity is envisaged. The potential impact of these changes is

- Active investors, who are the price formers in an IPO, will likely find encouragement to bid aggressively for such a stock in the IPO. They will know that the newly IPOed ‘megacompany’ will be included in the NASDAQ index even if less than 10% of its stock is sold.

- Even with a slim free float of less than 10% the ‘megacompany’ will be ‘overweighted’ by a factor of 3x. So, if 5% of a ‘megacompany’s stock is floated, its index weighting will reflect 3x that amount or 15%.

- This creates a natural ‘shortage’ of stock for passive investors who are c40% of funds under management (source Thinking Ahead Institute – November 2025). By their nature they do not take part in price formation, buying shares only after they have entered the relevant index.

- Critically the active investors will not have to wait long for the passive buying pressure to emerge. After just 15 trading days the passive funds will need to come in and buy stock.

- This potentially creates an incentive for active funds to bid aggressively in the IPO for stock with the knowledge that a subsequent spike in the share price will be met by ‘forced’ passive buying of a stock in natural short supply just 15 days later.

Market risk will remain (geopolitics, interest rates etc). Valuation risk will remain – AI style assets are typically highly rated. Yet the key is that these are stocks with a potential natural following (interest in the AI phenomenon is very high) and the period in which things must not go wrong for active investors is relatively short (15 working days).

The upshot is that

- The prospect of successful IPOs at a high valuation is improved.

- Short term active fund managers can expect a ‘pop’ in the IPO price with the arrival of ‘natural’ passive buyers needing to buy more stock than is readily available.

- Company insiders stand to benefit from a higher valuation for their shares.

- This is particularly relevant if the usual minimum holding periods are waived; sale of shares by insiders will not reduce the ‘stock shortage’ as that stock would become free float and enjoy the 3x multiplier effect.

- There is a benefit to the listing exchange from increased market and listing fees.

Everyone a winner? The short end of the straw is potentially grasped by ultimate owners of passive funds who are obliged by their nature to buy the newly IPOed stock at whatever level it has been driven to post IPO in anticipation of the need to fulfil the implied stock shortage.

Market concentration - what if you are not an AI business?

‘The top 1% of companies by valuation now absorb a third of all venture capital deployed. The bottom half get 7%, technically “venture-backed” but also kind of like sitting in the parking lot at a concert and claiming you saw the show’. - Lux Capital Q1 2026 report.

We have regularly charted the overall buoyancy of the VC market. Our Rothschild & Co Monitor indicates, for instance, that US raises of $100m+ in Q1 2026 were at$246bn at 3.5x the value of Q1 2025.

One of the debates though is to what extent the buoyancy of the overall market is felt by all participants, a point made vigorously by Lux Capital in its Q4 2025 Report.

Concentration across the venture landscape: ‘We see concentration across the venture landscape. Our long-expressed view of the coming extinction and involuntary exit of small VC funds (“minnows”) is empirically underway. Active VC firms declined 25% from around 8,000 in 2021 to 6,000 last year. First-time funds averaged just $7 million—less suited to venture and more a restaurant opening. The minnow extinction will accelerate and further concentration will follow. At the other end, the “Megas” are gathering assets at an increasing pace as predicted.

The surviving firms—including Lux—will enjoy less competition, better pricing power and most importantly, compounding relationships with coveted founders whom allocators will pursue for exposure and direct co-invests.’

Concentration in deals: The concentration of private capital is only matched by the concentration in equities. Nearly $340 billion flowed into U.S. deals, the second-highest amount ever, yet it was packed into the fewest deals of the decade, with nearly half the capital concentrated in a few dozen deals over $500 million. The top 1% of companies by valuation now absorb a third of all venture capital deployed. The bottom half get 7%, technically “venture-backed” but also kind of like sitting in the parking lot at a concert and claiming you saw the show.

Half of all venture money went to 0.05% of deals, while half of all LP capital went to a handful of funds.

A couple of interesting charts from the Pitchbook- NVCA US Q1 Venture Monitor to illustrate this.

Concentration amongst venture funds

In Q1 2026, $47.8bn was raised across 172 funds, a relatively encouraging total against the total of $66.7bn for the whole of 2025. There is though substantial concentration amongst a handful of funds. Six managers - Andreessen Horowitz ($12bn), Thrive Capital ($10bn), Founders Fund ($6.2bn), Battery Ventures ($3.25bn), Kleiner Perkins ($3.5bn) and Lux Capital ($1.5bn) - together raised $36.4bn, or 76% of the quarter’s total capital. All the remaining funds accounted for less than 25% of the Q1 capital raised.

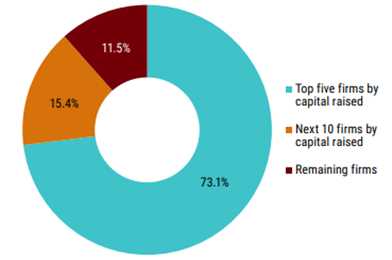

US - Five firms raise 73% of new US commitments in q1 2026

Source: Pitchbook NVCA Venture Monitor - March 31, 2026

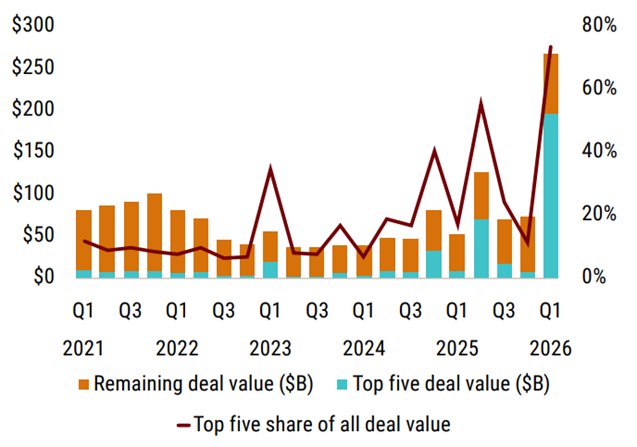

Concentration in deals

There is a matching effect in the concentration of deals. The top five US deals by value elicited $195bn, 78% of the total raised in the quarter.

Top five US raises by value in Q1 2026 – AI and related

Source: Rothschild & Co

Top 5 deals as a share of all US VC deal value by quarter

Source: Pitchbook NVCA Venture Monitor - March 31, 2026

How much has this changed? Using our Rothschild & Co Deals Monitor we can look at fundraising split into three categories – AI, AI related sectors (autonomous vehicles, robotics, data centres, legal tech) and ‘Other’ -everything else.

US fundraising - 'other sectors' see a 64% increase in funding 2025 vs 2024 ($bn)

Source: Rothschild & Co

We see that ‘pure’ AI raises have risen from 37% of deal value in 2024 to 57% in 2025 and 78% in Q1 2026 – albeit boosted in Q1 by the extraordinary $122bn raised for OpenAI.

AI related sectors – We limit these to four (autonomous vehicles, robotics, data centres, legal tech), defining them as sectors very closely associated with AI development. There is a case for including other sectors – quantum computing and semiconductors spring to mind – but we have resisted the temptation. The four AI-related sectors are more sporadic in their fundraising – 12% of the total in 2024, 5% in 2025 and 8% in Q1 2026.

‘Other Sectors’ - How is the non-AI part of the VC market doing?

This leaves us with the rest. In percentage terms it has seen a big fall away. ‘Other’ sectors were 50% of the US total in 2024, 38% in 2025 and just 13% in Q1 2026. The buoyancy of the venture market and the greater capital sums committed to it though make up the shortfall. Funding for these companies rose from $55bn in 2024 to $90bn in 2025, a rise of 64%. Even with the massive funding for Open AI in Q1 2026 funding for the ‘Other’ sectors was up 50% yoy to $33bn.

The numbers suggest that in the US a rising AI-fuelled VC tide is raising the ships in all sectors.

Looking at Europe, we see a market where AI has consistently taken a lower percentage of the overall available funding. Here ‘pure’ AI raises were just 6% of the value total in 2023, 7% in 2024, 11% in 2025 and 20% in Q1 2026. Indeed, AI related sectors (the same four as we defined for the US) have roughly kept pace with ‘pure AI’ rising from 2% of funding in 2023 to 8% in 2025 and 25% in Q1 2026 (large raises for the Nscale datacentre business and Wayve in Autonomous vehicles).

The overall market for fundraising has been more muted in growth terms than the US. Nevertheless, it has grown fast enough that while the percentage of funding going to the ‘Other sectors’ has slipped – from 92% in 2023 to 82% in 2025, actual funds raised in the ‘Other sectors’ rose from $29.3bn to $40.3bn (+38%) over those two years.

There was a further 5% yoy increase in Q1 2026 despite the percentage of funds raised for ‘Other Sectors’ slipping to 55%.

European fundraising - 'Other sectors' 38% increase in funding 2025 vs 2023

Source: Rothschild & Co

So, the takeaways from this are:

- The AI phenomenon with its substantial private raises, has helped to cement a super tier of VC firms which have the size, expertise and clout to get access to the AI deals that are driving the market. LPs anxious not to miss out on the perceived surge in value in AI are naturally concentrating their resources with those funds who offer access to the most desirable deals.

- The AI surge in VC investing though has spread through the ecosystem. The VC market is a more buoyant place than it was in 2022 and 2023. AI related sectors have expanded fast.

- The market for capital for non-AI businesses is less dramatically buoyant but has still grown well, up 64% yoy in the US in 2025 and up 38% in Europe by value 2023-2025.

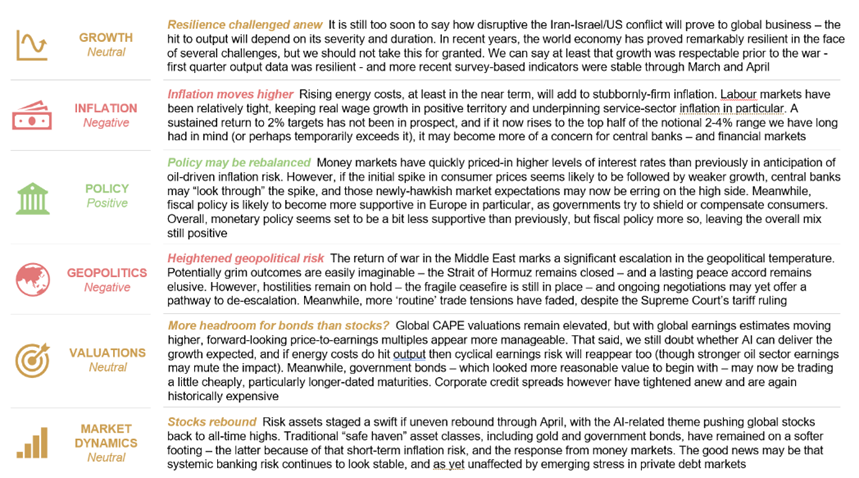

Public markets - Earnings outweighing geopolitics

In a sea of troubles, markets are responding positively to strong earnings

Public markets suffered in March on the outbreak of hostilities but have moved up sharply since the end of March on a combination of hopes of a de-escalation in the Gulf and against the background of strong earnings reports, particularly in the US.

The Iran conflict began with US/Israeli strikes on 28th February and in March the two major US indices, NASDAQ and the S&P500, both fell about 5%. In Europe the FTSE 100 Index was down 7% in March and the STOXX600 was down 8%.

Markets rallied from the end of March, presumably as commentators sensed the possibility of negotiations. Buoyed by the decision of the US to step back from the brink and not to ‘destroy civilisation’ in Iran on 8th April, NASDAQ is up 26% from March 30 to May 8th and the S&P500 is up 17%. European markets have rallied less with the FTSE 100 up 2% and the STOXX600 up 5% since March 30th.

This means that the relative strength of European indices versus US indices that had prevailed since the start of the year has been reversed. YTD NASDAQ is up 13%, the S&P500 is up 8% and the FTSE100 and STOXX 600 are both up 3%.

The FTSE Venture Capital Index has rallied 15% since the end of March but is still down 12% ytd largely reflecting the sell-off in the software and tech sectors caused by AI fears.

The market continues to walk a tightrope. The geopolitical risk from the Iran conflict remains with the continuous back and forth of peace proposals being punctuated by occasional flare ups in military action both in the Straits of Hormuz and in Lebanon. Although not at its peak levels of c$113 per barrel, WTI crude is still touching $100 per barrel.

The robust performance of the public indices since the end of March – and year to date – belies the negative implications of the Iran conflict, even if this has now peaked. Oil prices remain higher than they were prior to the conflict, some capacity has been destroyed, freedom of supply from the Gulf remains uncertain and supply chains have been disrupted.

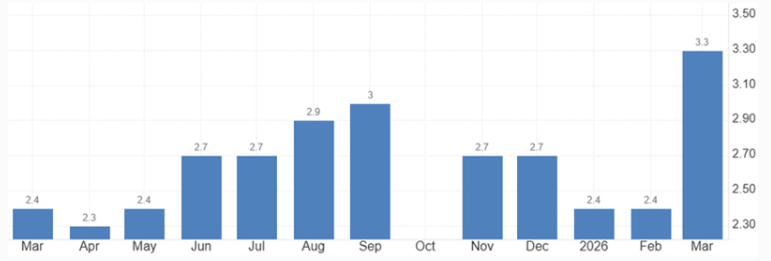

Headline inflation in March in the US jumped to 3.3% versus February’s 2.4%, the highest level for almost two years. The April figure emerged at 3.8%. One year ahead inflation expectations in the US are running at c3.6%- 4%, well ahead of the Fed’s 2% target and a sharp shift from the environment seen between November 2025 and February 2026.

US - Monthly Inflation trends %

Source: U.S. Bureau of Labor Statistics

While there is upwards pressure in US inflation, the US jobs market is doing surprisingly well. April’s non-farm payrolls saw jobs growth of 115,000. It was the first time in the second Trump administration that the figure had exceeded 100,000 jobs added two months running. The combination of a robust jobs market – a contrast to picture seen in 2025 - and rising inflation pretty much wipes out the case for further interest rate cuts. This is despite the impending arrival of President Trump’s nominee at the Fed; the choice of Kevin Warsh having finally been ratified by the Senate Banking Committee. He is due to start at the Fed on May 15th.

At the start of the year with US inflation trending downwards the expectation was for at least two rate cuts in the US in 2026, taking the Fed rate down from 3.5%-3.75% to 3%-3.25%, with the first rate cut expected in June.

By contrast, FedWatch currently has a 96% certainty of rates remaining unchanged at 3.5%-3.75% at the next meeting on June 17. Indeed, if there has been a change in interest expectations it is that interest rates might actually rise.

FedWatch is showing a 9% expectation that rates might go up 25bps on the 28th of October 2026 meeting outflanking a 7.6% expectation that they might fall. By the December 9th meeting the expectation is 74% for rates unchanged at 3.5%-3.75%, a 20% chance of a rise and just a 6% chance of a fall.

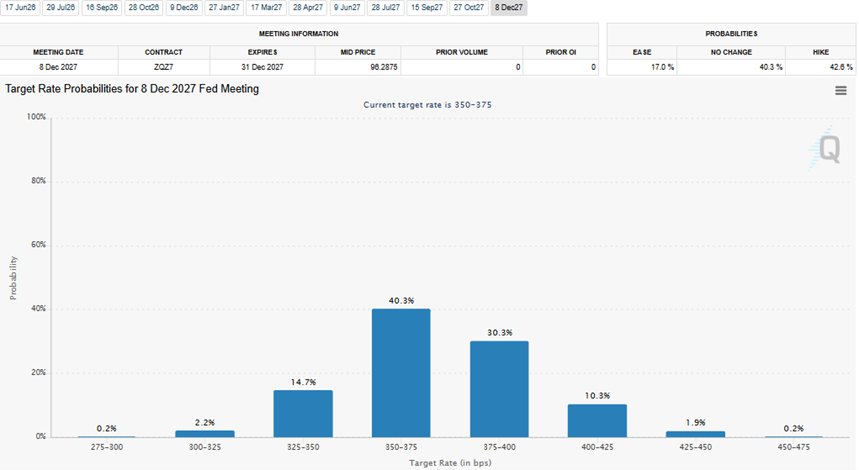

Even by the last Fed meeting of 2027 FedWatch shows just a 17% probability of a 25bps rate cut to 3.25%-3.5% with 40% at an unchanged 3.5%-3.75% and a 43% expectation of an interest rate raise.

Fedwatch - No US rate cuts expected by the end of 2027, a hike more likely than a cut

Source: CME FedWatch

The strength of the US markets since March 30th has been led instead by a very good Q1 earnings season with a strong weighting towards positive surprises and further upwards revisions to estimates for 2026 and 2027. The Magnificent 7 has led with particularly strong reports from Meta and Alphabet and with strong expected results from Nvidia still to come. With 90% of S&P 500 companies having reported, 84% of those having done so produced a positive Q1 EPS surprise and 80% a positive revenue surprise. While the Magnificent 7 has led, the market has been encouraged by the widening of earnings breadth.

As a result, earnings growth forecasts and year end S&P 500 targets have been revised upwards. Earnings growth of c27% in Q1 has led strategists sharply to raise their S&P500 earnings expectations for 2026. Updated expectations look for 2026 earnings growth of c22%-23% with 2027 growth seen around 15%. Magnificent 7 earnings are expected to rise in 2026 by c35% implying the balance of the S&P 500 will grow earnings by c12-15%.

These new 2026 earnings growth expectations of c22%-23% are well above forecasts at the start of the year that hovered at c13-15% p.a. for the next two years. It was on this mid-teens earnings growth expectation that typical year-end S&P500 targets of c.7,500 were predicated.

Now new, higher S&P500 year-end forecasts are starting to roll in. Yardeni Research – which looks for 22%/15% 2026/27 earnings growth- has set a new S&P500 year-end target of 8,250, up from 7,700. This exceeds the previous highest target of 8,000 shared by Deutsche Bank and Capital Economics. More prosaically RBC has raised its 2026 S&P500 target from 7,750 to 7,900 and HSBC is now at 7,650 having started at 7,500.

The European earnings season, if less spectacular, has also been solid. There are similar trends with a generally positive set of results with a leaning towards earnings beats and to upgrades. Consensus expectations for European 2026 earnings growth have firmed to around 14-15% from nearer 10-12% pre the Iran hostilities, with Energy companies leading the way but strong results also in semiconductors, Utilities, Autos and Software.

Also, as in the US, rising inflation is seen as a potential negative. Euro area inflation was 1.9% in February, 2.5% in March and 3% in April led by a sharp rise in energy costs at 10.9%. European interest rates are still at 2% but the expectation is that rates will now likely rise, starting with the June meeting. At the start of the year the expectation was that European interest rates would likely be held flat in 2026 whereas ECB Governing Council Member Martin Kocher commented recently that the ECB will need to adjust interest rates soon if the inflationary outlook does not significantly improve. The market has a c78% prospect of a 25bps rate rise at the June meeting and anticipates one further 25bps rise by the year end.

UK inflation was 3.3% in March up from 3% in February. Holding interest rates steady at 3.75% at the end of April the Governor of the Bank of England said that ‘higher inflation is unavoidable’ as a result of the conflict in the Middle East.

The BoE’s original expectation was that inflation would be back to 2% by April 2026. With inflation now on a very different trend, the start of the year anticipation of two 25bps interest rate cuts in 2026 has shifted to the expectation of two 25bps rises – most likely in July and September – taking rates up to 4.25%. It would be a 100bps adverse turnaround for the year end 2026 rate relative to start of year expectations.

Our Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian’s views on the current market outlook are summarised in the Exhibit

Source: Rothschild & Co

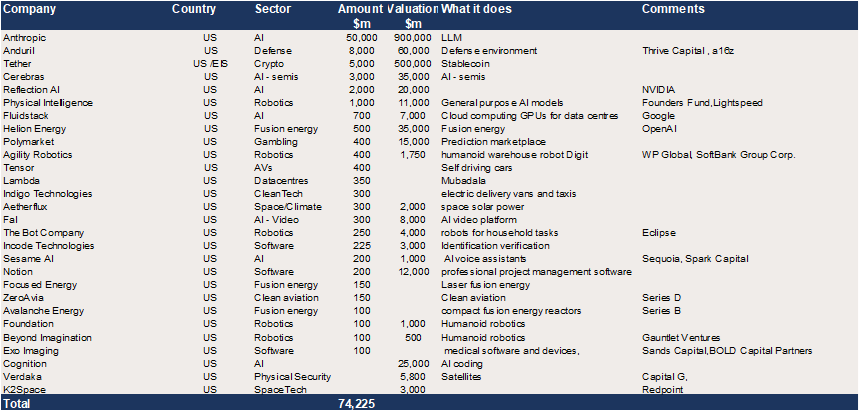

Fundraising outlook: c$82bn of potential raises

Pipeline is $74bn in impending US deals ($50bn Anthropic) and $8bn in Europe

The news that Anthropic - which has just raised immediate funding of $10bn from Google and $5bn from Amazon with deferred funding from the pair of another $50bn - is in the market for a further $50bn raise at a $900bn putative valuation, has boosted our monitor of impending US deals to $74bn.

Ex the Anthropic raise the total would be $24bn, down from $35bn last month, mainly due to the completion of a $10bn raise by Project Prometheus.

Cerebras, the AI semiconductor business enters the list with a projected $3bn raise.

Otherwise, the top of the US list continues to see defense business Anduril seeking to raise $8bn at a $60bn valuation with Thrive Capital and a16z.

Reflection AI provides tools to create personalized AI that can chat and interact like a person. The NVIDIA backed business is looking to raise $2bn at a $20bn valuation.

News on the possibility of Tether, the US/El Salvadorean stablecoin issuer, raising c$5bn and possibly more at a putative $500bn valuation has gone quiet. Reports had suggested that the company might delay its fundraising if the $500bn valuation target was not reached.

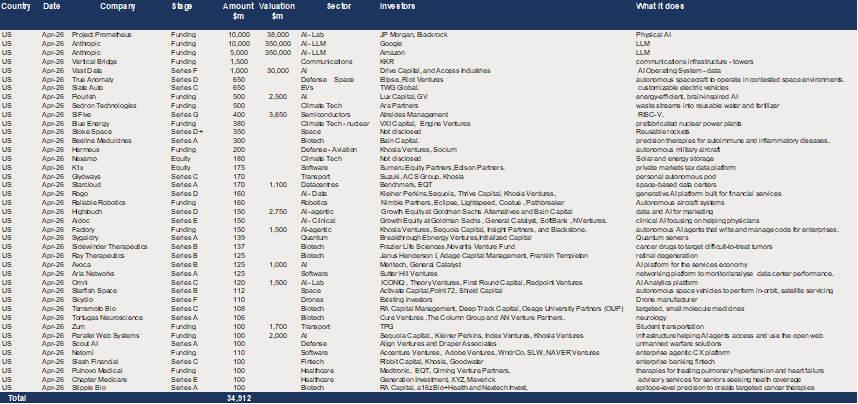

US Growth Equity – c$74bn in reported upcoming raises

Source: Rothschild & Co; press reports

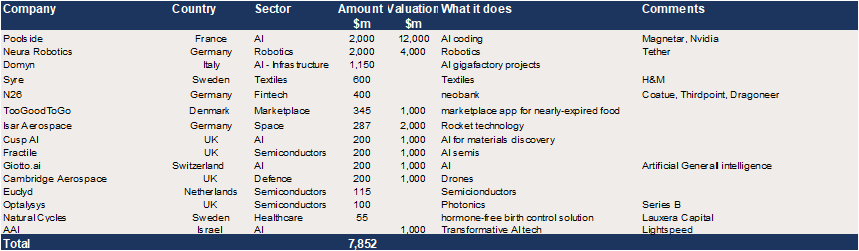

In Europe the total of identified impending raises drops from $8.3bn to $7.8bn.

The upcoming raises list remains headed by the expected $2bn raise for the French AI coding business Poolside led by Magnetar and NVIDIA. German business, Neura Robotics, whose flagship 4NE1 Mini humanoid robot has both consumer and industrial applications is looking to raise $2bn at a $4bn valuation. Stablecoin company Tether is said to be supporting the raise.

Italian LLM and AI infrastructure business, Domyn, is said to be raising $1.15bn in an upcoming Series B.

Dropping off the list of impending raises is Ineffable Intelligence of the UK after its $1.1bn seed round.

European Growth Equity – c$7.8bn in reported upcoming raises

Source: Rothschild & Co; press reports

Fundraising - Surge continues

Another $5.9bn raised in Europe in April and $35bn in the US

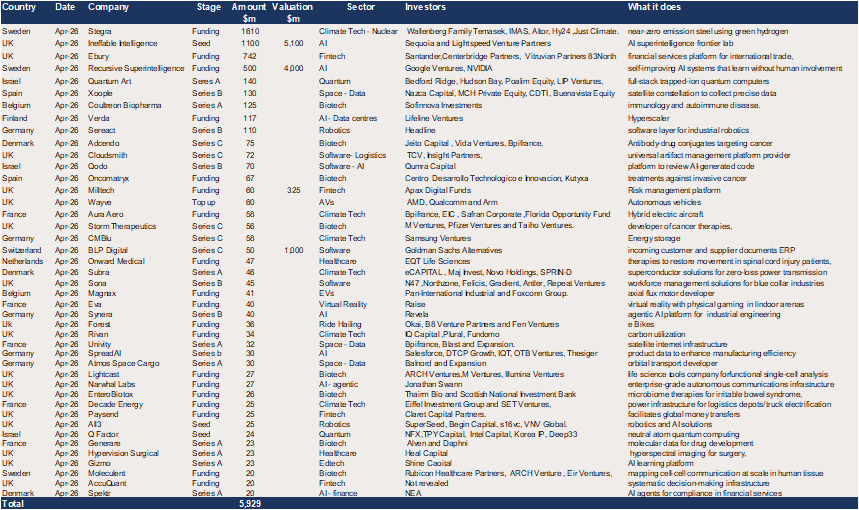

The surge in overall fundraising on both sides of the Atlantic continued in April. In Europe there were 43 rounds of $20m+ raising a total of $5.9bn. In context this is the fifth biggest month for fundraising in the 52 months since the start of 2022. The yoy percentage increase of 156% versus the $2.3bn raised in April 2025 was the biggest monthly yoy increase of that 52-month period. Year to date fundraising in Europe is 75% ahead of the 2025 total at $23.7bn (vs $13.6bn).

In the US $34.9bn was raised in April in $100m+ deals, topping the $30.2bn raised in March and 4.1x ahead of the $8.5bn raised in March 2025. The ytd date total at $281bn is now 3.6x greater than the $77.9bn raised to the end of April 2025.

In Europe Climate Tech unusually saw the biggest raise of the month. The $1.6bn raise for Stegra (formerly H2 Green Steel) was a blast from the past. Substantial rounds for major Nordic green projects were a commonplace in 2023 when Northvolt raised $1.3bn in August 2023 and Stegra $1.65bn in September 2023, another $330m in January 2024 plus $3.9bn of debt. The collapse of Northvolt in November 2024 meant such raises have typically dried up.

The most recent raise for Stegra is a €1.4bn funding led by Wallenberg Investments. The Swedish family investment vehicle is making a €250m equity investment and is being joined by Temasek and IMA with the consortium likely to take a majority stake in Stegra. Existing shareholders are also supporting the round including Altor who will be the second largest owner post deal, as well as Hy24 and Just Climate.

The deal is to rescue a complex project which has substantial up-front costs. Marcus Wallenberg, Chair of Wallenberg Investments, said:

“This is an industrial project of clear importance to Sweden. Based on our thorough assessment, we see a commercially viable way forward. That said, this remains a major and complex undertaking, and success will depend on strong execution across many dimensions. Taking these complexities into account, we enter this endeavour with a willingness to be deeply engaged going forward.”

Stegra was founded in 2020 with the intent to build a large scale low-carbon steel plant in Boden capable of producing five million tonnes of green steel annually. Stegra says the new financing gives it “a fully funded path to complete the construction and commissioning” of the plant.

Outside of Stegra the largest Climate Tech raise of the months was a more typically sized $58m for German energy storage business, CMBlu.

By sector AI again saw the largest total of raises at €1.83bn. There were two notable raises for frontier lab businesses. These are not at anything like the scale of the raises for the US counterparts OpenAI, Anthropic, xAI and other US peers but are indicative of increased funding percolating through to European businesses developing large-scale foundational AI models, an activity largely restricted to Mistral in Europe hitherto.

Ineffable Intelligence, a company founded in late 2025, has raised a $1.1bn seed round at a valuation of $5.1bn. It is one of the largest seed rounds ever in Europe. The business is led by David Silver who previously led the reinforcement learning team at Google DeepMind and who is a Professor of Computer Science at UCL. He has stated that he will donate all equity gains that he might make from the company to high impact charities.

The intent at Ineffable Intelligence is to develop AI systems through reinforcement learning, effectively AI that learns through trial and error rather than by absorbing human-generated text.

David Silver comments

“We are creating a super learner that discovers all knowledge from its own experience, from elementary motor skills through to profound intellectual breakthroughs. This super learning capability - the ability to endlessly discover knowledge and skills, without relying on human data - will be driven by the world’s most powerful reinforcement learning algorithms.’

The round was backed by Sequoia and Lightspeed with NVIDIA and Google also contributing. Interestingly the UK Sovereign Fund and the British Business Bank also contributed.

University College London had a good month. Tim Rocktäschel, Professor of AI at UCL and until recently a Principal Scientist at Google DeepMind, is one of the founders of Recursive Superintelligence which raised $500m at a $4bn valuation in a funding round led by Google Ventures and NVIDIA. The company’s strong founding team includes co-founder Richard Socher, previously Salesforce.com’s chief scientist plus a group of former OpenAI, Google and Meta scientists. Albeit using different approaches, like Ineffable, Recursive aims to develop AI systems that improve without human intervention. The aim is to automate all of the elements of the frontier AI development pipeline.

Also, like Ineffable, Recursive is just a few months old, having been founded in late 2025. Both are good examples of an AI talent-raise where the funding pursues individuals, a concept and a team rather than revenues or product. Stopping for a moment on valuation Recursive has twenty staff and a valuation in this round of c$4bn, implying a valuation of $200m per member of staff. Maybe it should employ some more people….

Three other features to note in Europe’s April raises:

- Are we seeing the delayed effect of the SaaS Apocalypse? There were just four software raises in April picking up a total of $237m with the largest being a $72m raise for the UK’s Cloudsmith, a universal artifact management platform which manages and maintains software in a period of rapid AI software development. Part of the issue may be a renewed caution about the prospects for SaaS and software businesses in the age of AI. The other factor is that software businesses now self-identify as AI businesses, making the category tougher to discern.

- There was a substantial fintech raise with Ebury, a financial services platform for international trade, raising $742m from a consortium including Santander, Centerbridge Partners, Vitruvian Partners and 83 North. Ebury’s platform enables payments in more than 140 currencies across 160 countries. Santander is the majority owner of Ebury, will invest $50m and retain a 55% stake.

- There was a notable top up raise by autonomous vehicle business Wayve which secured an extra $60m from AMD, Qualcomm and Arm after its $1.5bn raise at a valuation of $8.6bn in February.

Europe – 43 raises of $20m + in April for a total of $5.9bn

Source: Rothschild & Co

In the US the $34.9bn raised in April continued a sequence of remarkable months for US VC fundraising. In the eight months since September only one month, December, has fallen short of $20bn fundraising. A total of $380bn of US fundraising has taken place in that period, an average of $47bn per month.

AI once again dominated in April with £27.5bn of the $34.9bn raised, 79% of the total. There were four $1bn plus raises.

Anthropic appears twice on the April list with two raises, one of $10bn and one of $5bn. These follow the $30bn Series G in February supported by Coatue, Dragoneer, Founders Fund, GIC, Iconiq and others at a $350bn valuation. Google has re-entered the fray with an agreement to invest up to $40bn in Anthropic, with $10bn up front and $30bn contingent on performance. We reflect the $10bn in our April number. The investment is at the same $350bn valuation. After the announcement of the funding, Anthropic struck a deal with Google in early May in which it committed to spend $200m with Google Cloud over the next five years.

The second Anthropic appearance in the April list is for a $5bn investment by Amazon. Again, it is a circular deal with Amazon investing $5bn immediately in Anthropic with the promise of a further $20bn over time. Anthropic in turn has committed to spend $100bn on computing resource from Amazon. Anthropic will secure up to 5 gigawatts (GW) of capacity to train its AI models, including Trainium, Graviton and the upcoming Trainium 3 chips. Amazon previously invested $8bn in Anthropic.

As we write this Anthropic is said to be contemplating a further $50bn round at a valuation of $900bn, a level that would top the $850bn valuation of OpenAI in its March funding round.

A further $10bn was raised in April for Jeff Bezos’s Project Prometheus in a round led by JP Morgan and Blackrock. It swiftly followed on from the $6.2bn it raised in November 2025. The latest round valued the company at $38bn. Project Prometheus is training models on real-world experimental data, robotic interactions, and engineering workflows, targeting industries including aerospace, automotive, advanced manufacturing, and drug discovery.

Finally Vast Data raised $1bn in its Series F at a valuation of $30bn, up from the $9.1bn Series E valuation in late 2023. The round was led by Drive Capital and Access Industries and included Fidelity Management & Research Company, NEA, and NVIDIA. Vast Data has designed the VAST AI operating system to unify data, compute, and real-time processing into a single system.

Three other factors to note in April

- As in Europe it was a light month for software raises. There were just three rounds for software businesses raising a total of $410m.

- Defense raises continued to attract good support. There were three raises totalling $950m with the largest of these being the $650m Series D of True Anomaly, a developer of autonomous space craft to operate in ‘contested space environments.’

- Space related raises are attracting a steady flow of VC money with the reusable rocket maker Stoke Space gathering a $350m Series D+ and Starfish Space, a developer of autonomous space vehicles for in orbit satellite services, $112m in a Series B.

US and Canada – 41 $100m+ deals raised $34.9bn in March

Source: Rothschild & Co

Our views on the state of the venture capital markets

This revival of the growth equity market has been led by the US and by a surge of interest in artificial intelligence model providers and for companies using AI to transform a range of underlying industries.

At the same time the venture industry has re-adopted strong underlying approaches to investment with companies in most sectors striving to achieve a better balance of growth, profitability and cash flow. The underlying quality of the cohort of VC backed companies has improved.

Our summary of the outlook

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, quantum, semiconductors, new energy sources like nuclear and fusion) supporting the development of AI.

- The influence of AI is percolating through many other industries such as drug discovery, defence, robotics, legal tech, autonomous vehicles, and cybersecurity fuelling a broader advance in the growth equity market.

- Overall, the VC market is regaining confidence with the strength of interest with fintech, blockchain/crypto and biotech reviving strongly.

- There is a burgeoning interest in defence industries from investors with both the tense geopolitical political environment, the advances in AI applications and the experience of the combat in Ukraine contributing to investor focus. By contrast, ClimateTech, while still a substantial sector has become less prominent both as a result of some high-profile failures and being less favoured politically in the US under the current administration.

- Fund raising for venture capital firms remains subdued. Fund raising is concentrating into larger, established firms. US VC fundraising in 2025 was concentrated in larger firms and at near decade lows.

- The speed of the investment process has slowed down since 2021-22. The level of diligence on deals has stepped up. This is true even in the ‘hot’ parts of the market like AI. Outside these areas it is marked – processes take time, downside protection is sought.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on the combination of growth and profitability (or a rapid path to it) and on free cash flow.

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025, April 2025, May 2025, June 2025, July 2025, August 2025, September 2025, October 2025, November 2025, December 2025, January 2026, February 2026, March 2026, May 2026

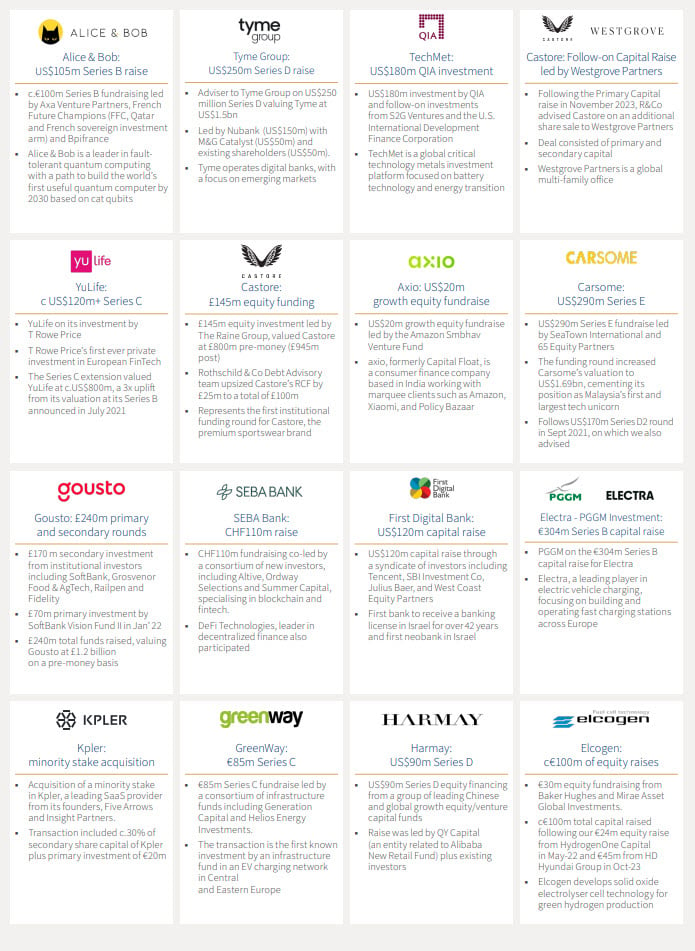

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Mark Connelly

Co-Head of Global Market Solutions

+1 212 403 5500

+1 917 297 5131

Chris Hawley

Global Head of Strategic and Private Investors.

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Capital Markets Europe

+44 20 7280 5088

+44 7542 477 291

Antoine de Guillenchmidt

Co-Head of Equity Capital Markets Europe

+44 20 7280 5377

+44 7907 712 978

Pete Nicklin

Co-Head of Equity Capital Markets Europe

+44 20 7280 1668

+44 7912 395 294

Laura Klaassen

Head of Private Distribution

+44 7926 905 488

Thomas Chung

Head of Private Capital, North America

+1 212 403 5559

+1 917 594 7208

Tim Brenton

Director of Private Distribution

+44 20 7280 1351

+44 7788 395 556

This document is being provided to the addressed recipients for information only and on a strictly confidential basis. Save as specifically agreed in writing by Rothschild & Co Equity Markets Solutions Limited (“Rothschild & Co”) this document must not be disclosed, copied, reproduced, distributed or passed, in whole or in part, to any other party.

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.