Growth Equity Update

April 2026 – Edition 49

- Launch of PISCES: March saw the first trading in companies on the new PISCES (Private Intermittent Securities and Capital Exchange System) system. We review the workings of London’s ‘intermittent trading venue’ for private companies which seeks ‘to bridge the gap between private and public markets.’

- Storming Q1 for growth equity raises in the US: In the US Q1 growth equity fundraising hit $246bn, a record quarter, breezing past the 2025 full year total of $234bn. Almost half was for Open AI which announced $122bn of fundraising across February and March.

- Europe buoyant as well: Europe saw $7.7bn raised across 60 deals in March, the biggest month by value in the last five years and bringing the Q1 2026 total to $18bn, 60% up on Q1 2025 and the biggest quarter for European growth fundraising since 2021.

- Unicorn creation suggests buoyant valuation trends: Q1 2026 saw 15 new unicorns created in Europe, the highest level since Q2 2022. The 66 new unicorns created in Q1 in the US was double the number in Q1 2025.

- Initiatives to supply critical European late-stage funding. The European Investment Fund has launched its ETCI 2 initiative to create a €15bn fund of funds to unlock up to €80bn in scale-up capital across Europe. The EC’s €5bn Scaleup Europe Fund also launching Spring 2026 will invest directly into companies in strategic tech sectors looking for funding rounds of €100m+.

- Iran conflict and public markets: Fast moving. With the announcement of an uneasy truce NASDAQ is now flat since the start of the conflict at the end of February, the S&P 500 is down 1%, the FTSE 100 down c3% and the STOXX 600 down 4%. This robustness belies deteriorating prospects for interest rates and corporate earnings since the war began.

- $34bn of impending raises. Our monitor of forthcoming rounds is starting to rebuild after the substantial recent raises and charts an impending c$26bn of raises in the US including $8bn for defence tech, Anduril, and $8bn in Europe headed by $2bn each for AI coding business, Poolside and for Neura Robotics.

Download a PDF version of the Growth Equity Update

PISCES - Intermittently interesting

March saw the launch of the UK’s PISCES market for secondary shares in private assets

Faced with criticism around the falling number of listed companies, a dearth of IPOs and the drift of UK public companies to US exchanges, the UK has responded with a semi-regulated crossover market providing private companies with intermittent auctions for secondary shares.

March saw the first trading in companies on the new PISCES (Private Intermittent Securities and Capital Exchange System) exchange.

As part of the Mansion House Reforms launched in the UK by the then Chancellor Jeremy Hunt in July 2023 was a proposal for an ‘intermittent trading venue’ for private companies, a hybrid trading platform to allow private companies to trade periodically rather than continuously. The trading venue would seek ‘to bridge the gap between private and public markets.’

In its consultation paper on the proposals for the exchange, it was noted that:

Alongside the work the government is doing to improve public markets, the government also wants to ensure smaller companies can access capital and scale up, that we allow investors to take advantage of this shift to private markets, and ultimately that such companies can transition to public markets more easily.

The concept is similar to the Nasdaq Private Market, which launched in 2013 to provide investors and employees of private companies more opportunities for liquidity.

The key principles driving PISCES are:

-

PISCES incorporates elements from public markets, such as multilateral trading, and elements from private markets such as greater discretion over what company disclosures should be made public.

-

PISCES will accommodate ‘trading windows’ at chosen (monthly, quarterly, biannual etc) intervals. Its regulatory regime is designed to provide a degree of investor comfort like a clear price formation process, a regulatory and legal framework and investor protections.

-

Critically PISCES is limited to secondary trading and only professional investors will be allowed to participate – not retail.

-

Disclosure requirements specific to PISCES will apply shortly before and after each trading window, and there will be no requirement for information to be disclosed to the public. Instead, information must only be made available to investors who may trade during the window.

The concept is that participation on PISCES will support companies to scale up and grow, providing liquidity, helping shareholders, including employees, to realise their gains, and providing an opportunity for companies to rationalise their shareholder base. The hope is that better investor connections and investor familiarity will smooth the path to IPO in due course.

The key elements are:

Market operators and agents

PISCES Operators: PISCES is a concept which requires operators to design and conduct the auctions. The first such operator to be approved by the FCA was the London Stock Exchange joined shortly afterwards by JP Jenkins, part of InfinitX.

Registered Auction Agents: These firms are intermediaries licensed to trade shares on PISCES. They manage functions such as checking that investors meet the correct eligibility criteria, they control access to company information via a disclosure portal and, in the actual auction process, are responsible for submitting buy and sell orders into the Private Securities Market (PSM) auction system. They fulfil the equivalent role to a broker in public markets. Rothschild & Co Redburn, and several other firms, are RAAs.

So how does it work?

Secondary only: A PISCES platform operates only as a secondary market for the trading of existing shares. It cannot be used as a means of raising primary capital through issuing new shares.

Share buybacks are not presently allowed – although HM Treasury has pledged to keep this under review.

Auction process: The PISCES platform allows for multiple buying and selling orders to interact in the system in a non-discretionary matching system. The operators are obliged to operate a trade transparency regime so that investors can see that they are participating in a fair and orderly market.

Periodic auctions: The platform is intended for periodic auctions in secondary shares of private companies. Trading is to be intermittent – defined as ‘occasional, not frequent and of limited duration.’ This implies trading could be monthly, quarterly, annually, or simply ad hoc.

Running an auction – Participating companies are allowed to:

- Choose when their shares are traded

- Who is allowed to buy the shares. Participants should be professional and sophisticated investors.

- The company can select a price range, defining a minimum and maximum price.

- Choose who receives information about the company and the transactions.

No restriction on sellers: Although companies can restrict who buys their shares, the reverse is not true. On the sell side the company is unable to restrict an existing investor from selling at a trading event. All existing shareholders of participating companies, including company employees, will be able to sell shares.

A bespoke disclosure regime: Companies are required to produce ‘core information’ ahead of a trading event. This information will include:

- A business and management profile.

- Financial statements.

- An update on any recent events or changes.

- Information about the company’s share capital, including major shareholders, beneficial owners, and employee share schemes.

- Details about directors' transactions in the shares of the company and their trading intentions for the upcoming trading event.

- Information on major contracts and material company-specific risks.

- The company is also asked to supply information on any price parameters being applied at the trading event.

- It also is required to provide historic trading data and information regarding commitments on holding future trading events.

There is a much lighter disclosure regime than would be required in public markets and it is fashioned around the concept of a ‘negligence standard’ which simply requires officers of the company to believe that the information it is providing is true and not misleading.

The information being supplied to would-be investors in a PISCES trading event is not required to be made public. Instead, it can be made available in a secure environment – typically a data room to which permissioned access is given for those investors chosen to participate in the auction.

PISCES trades are exempt from stamp duty and stamp duty reserve tax.

The London Stock Exchange’s version of PISCES, its Private Securities Market (PSM) will use its existing public markets technology for trading, including the LSE Order Book and CREST settlement system. This will be complemented by some features from private markets. Thus, company information will be uploaded to a disclosure portal hosted by the LSE and will only be accessible to eligible investors. The disclosure requirements set by the FCA are intended to be proportionate to and reflect that the companies using the Private Securities Market will be private.

Originally HMG hoped that PISCES would be up and running by the end of 2024. Instead, the first company to be traded on PISCES was QPlay, a small UK board games company owned by the Velocity Capital EIS. The shares were listed on the JP Jenkins PISCES platform on March 18 2026, and the auction remained open until March 24.

The LSE’s first auction on its PISCES compliant Private Securities Market (PSM) was launched on March 26 with the company being Tradable Private Equity (TPE). TPE is a TPEIC (pronounced T-Pick - a tradable private equity investment company) which will hold shares in Oxford Science Enterprises as its sole asset. Oxford Science Enterprises - which is not listing - is a £1.3bn investment company commercialising scientific research from Oxford University with a portfolio of over 100 tech companies. The TPEIC is entirely independent of OSE. The TPEIC facilitates structured secondary liquidity through permissioned auctions on the PSM.

The nature of the first two listed companies to list on PISCES reflects a degree of caution about trying out this new listing venue. Commentators have observed that there is “a long queue of companies willing to go second.”

How users of the LSE’s Private Securities Market interact

Strong Q1 fundraising trends

A record quarter in both the US and Europe.

Q1 2026 saw buoyant growth equity markets on both sides of the Atlantic. In the US Q1 fundraising hit $246bn, breezing past the 2025 full year total of $234bn. Almost half was for Open AI which announced $122bn of fundraising across February and March.

In Europe, the total for Q1 2026 fundraising was $18bn, 60% up on Q1 2025. It was the biggest quarter since 2021, easily beating the previous high of $12.9bn posted in Q2 2022.

The US – Q1 total fundraising at $246bn exceeds the full year 2025 total

The Q1 total for US fundraising at $246bn was driven by the intense activity in AI related raises. By sector AI led by some distance both in terms of number of raises, 35, and the value at $193bn.

The chart shows the top ten raises by value in the US in Q1. Of the top eight by value, seven are for AI businesses, with only the $16bn raise for autonomous vehicles business Waymo in fourth spot interrupting the procession. The final two raises in the top ten are both for defense businesses, highlighting the surging private capital interest in the sector in the new environment of US brinkmanship in world affairs.

The three biggest raises were all for AI LLMs – the initial $110bn OpenAI raise announced in February, the $30bn Anthropic raise in the same month and the $20bn raised for xAI in January. The fifth largest raise was the additional $12bn added to the Open AI raise in March. $3bn of this additional amount was raised from private investors. XAI also had a $3bn follow on raise in February.

Databricks which helps customers connect their data with AI models to launch custom agents, raised $7bn in February and Thinking Machines Lab secured a substantial investment from NVIDIA.

The top 10 US growth equity raises by value – Q1 2026

Viewed by sector AI raises amounted to 78% of the Q1 funding total, above the 2025 run rate of 57% with the difference being the size of the Open AI funding.

AI related sectors were also well represented. Notably a single raise, the $16bn for Waymo, pushed Autonomous Vehicles into second place in terms of sector raises. Robotics, with just short of $4bn across eight raises led by the $1.4bn for SkildAI and the $935m for Apptronik, was the fifth largest sector. Legaltech with a $200m raise for Harvey, and quantum with $130m for Photonic, chipped in. Taking the related sectors into account, AI and related raises were $213bn, 87% of the quarterly total.

Notably there were no substantial US equity raises for datacentres in Q1, with the emphasis in that part of the market having moved to debt funding.

Defense has been developing fast as a destination for VC funding and the sector moved up into third place by value in Q1 with nine raises totalling just over $6bn.

The largest of these was the $2bn raise for Shield AI led by Advent and JP Morgan at a valuation of $12.7bn. It previously raised a $240m Series F in March 2025 at a valuation of $5.3bn with strategic investors L3Harris and Hanwha Aerospace and VC investors including Andreessen Horowitz.

ShieldAI is a developer of software for autonomous aircraft and drones with its Hivemind software allowing drones to operate autonomously and its V-BAT vertical take-off and landing drone delivering ISR (intelligence, surveillance, and reconnaissance) and targeting at a fraction of both the cost and logistical footprint of larger drones.

Saronic Technologies raised $1.75bn in a deal led by Kleiner Perkins valuing the company at $9.25bn. It previously raised $600m in February 2025 at a $4bn valuation. Saronic describes its mission as ‘redefining maritime superiority for the United States and its allies’ by developing autonomous surface vessels. It is building a new shipyard, Port Alpha, allowing it to expand its medium and large-class autonomous vessels- effectively water-borne drones.

Software: Despite the ‘SaaS Apocalypse’ disruption to confidence in software business models caused by the advent of agentic AI applications, the sector remained a prominent destination for VC raises in Q1. It ranked fourth in terms of funds raised (it was in second place in the whole of 2025) with 23 raises garnering $4.4bn. The software raises were led by a substantial $450m round by the restaurant commerce enablement platform inKind. The vibe coding business Replit raised a $400m Series D at a $9bn valuation led by Georgian Partners. It previously raised $250m at a $3bn valuation in September 2025. Clickhouse, the real-time analytics and data warehousing company, raised $400m in a Series D led by Dragoneer at a valuation of $15bn.

Q1 – $246bn of US Growth equity fundraising ranked by sector value of raises

Robotics: There has been an explosion of interest in Robotics in recent months. In the whole of 2025 $3.8bn of VC funding went to robotics. That figure was exceeded by the $4bn raised in Q1 2026. There were eight raises of $100m+ and three substantial raises of $500m or more. The largest raise of these was the $1.4bn for Skild AI which makes foundation models for robots. The concept is that Skild’s software and foundation models can be retrofitted to a variety of robots and tasks without the need for substantial additional training. The robots then operate on a learn-as-you-go basis. The January round was led by Softbank and Nvidia at a valuation of $14bn. It previously raised a $135m Series B at a valuation of $4.5bn in July 2025.

In February there was a substantial Series A of $935m for humanoids robotics company Apptronik led by VB Capital Group and Capital Factory at a valuation of c $5.3bn. The raise was originally announced as a $350m Series A in February 2025 but was expanded, according to the company, due to inbound investor interest. Apptronik has partnered with Google DeepMind, logistics business GXO, and Mercedes Benz in its pursuit of an embodied AI solution. The aim is that Apptronik powered robots can respond to their environment rather than following fixed automation patterns.

Mind Robotics, a spin out from EV manufacturer Rivian raised $500m at a c$2bn valuation in a Series A led by Accel and Andreessen Horowitz. Like Apptronik it is focused on industrial robotics. It says:

“Existing industrial robotics can perform repeatable, dimensionally stable tasks, but a large share of factory value-add work requires human-like dexterity, adaptation, and physical reasoning that classical robotics cannot address. Mind Robotics is building the AI foundation—models, hardware, and deployment infrastructure—to close that gap.”

Other notable sectors and raises – We pick out three:

Space: The Artemis mission around the moon has seen 1970s style interest in space exploration. Q1 has also seen a rash of space related deals with eight raises in the US for a total of $1.9bn.

In March Colorado based Sierra Space raised $550m in a Series C led by Luminarx Capital at an $8bn post money valuation. The company describes itself as a defense-tech space company. Its contract wins include $450m to build four satellites for a National Security customer and a $740m contract to build 18 missile warning, tracking, and fire control satellites. It claims to have contracts with all eight space procurement agencies within the Department of War and Intelligence Community.

Axiom Space is a space infrastructure company that organises private astronaut missions to the International Space Station and builds commercial space station modules. It has a $140m contract from NASA as part of its Next Space Technologies for Exploration Partnerships (NextSTEP) programme to build a habitable spacecraft to be attached to the International Space Station. Its $350m raise in February led by Type One Ventures and the QIA will.

‘Advance its mission to deliver the successor to the International Space Station (ISS) and ready its next-generation spacesuits for the United States' return to the Moon for the first time in more than 50 years.’

Vast is also building space station infrastructure. It raised a total of $500m in March 2026 including a $300m Series A and $200m in debt in a deal led by Balerion Space Ventures with participation from IQT and the QIA.

Like Axiom, Vast builds space stations with its Haven-1 single-module space station due to launch in early 2027 and the multi-module Haven-2 station to follow. It also has a contract for a private astronaut mission to the ISS due in mid-2027. Worryingly founder Jed McCaleb has clearly not read Philip K Dick’ s ‘Martian Timeslip’ or ‘The Three Stigmata of Palmer Eldritch’…

‘Vast was founded with a long-term vision of billions of people living and thriving in space. Achieving a goal of this magnitude requires deliberate stepping stones, and our strategy of building, testing, and iterating with real hardware is delivering results. It is exciting to welcome additional investors who recognize Vast’s long-term potential and share our belief in making this vision a reality.’

Prediction markets: We wrote about the rise of Kalshi and Polymarket in our December 2025 Growth Equity Update. The two prediction market gambling businesses operate on a blockchain infrastructure with Polymarket historically focused on international markets and Kalshi on US markets. Both though are expanding in the US and international markets, and their US regulatory status has evolved. Kalshi is licensed by the Commodity Futures Trading Commission (CFTC) which regulates the US derivatives markets. Polymarket has lacked the legal status to operate in the US but recently acquired a CFTC-licensed exchange, QCEX, and has relaunched.

Their status though remains controversial after a series of remarkably well-placed bets made around US government actions including the intervention in Venezuela and the timing of the US attack on Iran.

In early March the CTFC’s Market Oversight Division launched a formal rulemaking process for what kinds of events can be included in prediction market contracts and under what conditions. Democratic Congress members have introduced the BETS OFF act looking to ban events connected to military operations and government actions. Some individual states have looked to restrict the prediction markets based on their activities amounting to unlicensed wagering - Massachusetts, Nevada, Arizona and Michigan are prominent in this respect. California has focused on insider trading issues with Governor Newsom signing an order to bar state officials from using non-public information to profit in prediction markets.

Polymarket raised $2bn in November 2025 at an $8bn valuation, up from $1.2bn in January. Kalshi’s June 2025 Series C valued it at $2bn, while its $1bn November 2025 raise was at $11bn.

In March this year Kalshi raised a further $1bn in a round led by Coatue Capital at a valuation of $22bn, twice the November level and 11x its valuation in June 2025.

Consumer apps: A couple of interesting raises in consumer apps.

Whoop is a wearable fitness tracker. The wearable band measures various health metrics such as sleep, strain, heart rate, stress and recovery, and is aimed at athletes and people interested in fitness. Its subscription-based model has the information accessed by an app rather than on the band. At the end of March, it raised a $575m Series G at a $10.1bn valuation in a deal led by 2PointZero Group, the QIA, Mubadala, and including Cristiano Ronaldo. The valuation is up from $3.6bn in its 2021 $200m round.

One of its rival businesses is Europe’s Oura, the wearable ring business which raised $900m in October 2025 at an $11bn valuation.

Cloaked raised $375m in a Series B led by General Catalyst and Liberty City Ventures in March. Cloaked is a consumer-focused privacy company whose platform has three key elements. Its virtual identities generate unlimited unique phone numbers, email addresses, and passwords on demand, shielding personal data before it is exposed. Its data removal feature automatically eliminates personal information from data brokers and people-search sites, cutting off years of accumulated exposure. Call Guard, its AI-powered call screening, detects and blocks spam, scam, and fraudulent calls in real time. Arjun Bhatnagar, co-founder comments.

"We've disguised more than 10 million identities, removed over a billion records from data broker sites, and screened more than 40 million calls – and we're just getting started."

Europe - Q1 2026 fundraising was $18bn, 60% up on Q1 2025

Europe’s Q1 fundraising of $18bn was 60% up on Q1 2025 and represented the biggest quarter for European growth fundraising since 2021, easily beating the $12.9bn of Q2 2022. In context is represented just 7% of the amount raised in the US in Q1.

AI topped the sector rankings with 19 raises totaling $3.5bn. There were three raises of over $500m. Advanced Machine Intelligence (AMI) Labs led by Yann LeCun, who was the key architect of Meta’s AI strategy, is looking to develop ‘world models,’ sophisticated, forward thinking AI systems capable of planning complex actions. In March the company raised $1.03bn at a pre money valuation of $3.5bn. led by Cathay Innovation, Bezos Expeditions, Temasek and Nvidia. The French business is a ‘talent raise’ being pre-product and pre-revenue.

The Israeli business Vast Data’s $1bn round at a $30bn valuation was in a mix of primary and secondary. The company’s AI operating system is a platform designed to unify and orchestrate storage, database, and compute resources, optimising the infrastructure required to support advanced AI workloads and large-scale data processing. It positions itself as "the Operating System for the Thinking Machine."

Eleven Labs raised a $500m Series D in February led by Sequoia at a valuation of $11bn, three times the level of its January 2025 round. Eleven Labs has developed from an initial focus on AI text-to-speech technology to speech-to-text, sound effects, dubbing, music, and conversational AI.

Software occupied second spot in terms of the value of raises, its $2.4bn total boosted at the start of the year by the unusually large (for a software company) $1bn raise by the Octopus Energy spin out Kraken which was valued at $8.65bn. Kraken, the ‘modern operating system for utilities’ supplies energy software to utility companies. The round was led by D1 Capital, Fidelity International and Teachers Ventures.

The Dutch travel software company Mews raised $300m in a Series D funding round that valued it at $2.5bn and which was led by EQT Growth, with new investors Atomico and HarbourVest. The French accounting software business Pennylane, which targets start-ups and SMEs in Europe, raised $205m in a round led by TCV and Blackstone Growth.

Datacentres: Based in the UK, Nscale is an AI hyperscaler with its data centre sites supporting LLM platforms. Its $155m December 2024 raise was one of the largest European Series A rounds in that year. The company described its $1.1bn October 2025 raise as the largest Series B in European history. In March 2026 it raised a $2bn Series C at a valuation of $14.6bn led by Aker ASA and 8090 Industries and including Nvidia. Founder and CEO Josh Payne commented:

"Over the next 5 years, Artificial Intelligence will be integrated into every industry, every product, and every job. Accelerating drug discovery, extending human life, autonomizing travel and robotics, lifting productivity, and driving massive growth. This is leading to the largest infrastructure buildout in human history. Nscale is leading this buildout. We are building this foundation that the market sits on, the engine of superintelligence.”

The hyperscaler will use the proceeds to further its deployment of large-scale AI infrastructure across Europe, North America and the Middle East, enabling the rapid rollout of the company’s “AI factory” data centres for projects like Stargate UK and Stargate Norway, and the expansion of its vertically integrated AI cloud platform.

Autonomous Vehicles: In the same month that Waymo was raising $16bn, its European counterpart Wayve raised a $1.2bn Series D, the largest fundraise in Europe since Mistral’s $2bn in September 2025. The round was led by Eclipse, Balderton and SoftBank Vision Fund 2. Microsoft, NVIDIA and Uber participated. Uber is potentially committing another $300m to take the total raise to $1.5bn. This is dependent on plans for multi-year deployments of Wayve-powered robotaxis on the Uber network. The intention is to scale to more than 10 markets globally with the launch of the first service in London in 2026, with broader international rollout to follow.

Fintech was the fifth largest category for fundraising in Europe in 2025 and held that position in Q1 2025 with 18 raises totalling $1.2bn. There were led by a $170m Series C for the debt capital markets data business 9fin led by HarbourVest and CPP Investments; a $155m Series D for Allica Bank, a UK challenger bank for SMEs led by Ventura Capital, GLG and Sona AM; and a $117m (€100m) raise for Italian rental advance company Rent2Cash.

Elsewhere Biotech continued to see a solid profile of raises with 18 deals raising $1.06bn. Climate Tech slipped to seventh ranking (it was fourth by value of raises in 2025) with 14 deals raising $868m. The large deals that were common in this sector in 2021-23 continue to evade it with the biggest deal in Q1 being $225m for the German grid-scale battery energy storage systems business, Terralayr.

Buoyed by AI interest, semiconductors were prominent with eight deals raising $853m with rounds of $200m+ for each of Axelera AI, Kandou AI and Olix Computing. All three are focused on inference chips.

LegalTech, another AI led sector, saw four deals raise $695m with the key one being the $550m raised for Swedish legaltech, Legora, the key rival to Harvey of the US which raised $200m this quarter.

As in the US, Defence is becoming more prominent as a VC funded sector. The main area of European fundraising is in drones with Roark Aerospace ($210m) Harmattan ($200m) and SensofusIon ($53m - anti drone systems) all focused on this area.

Overall, the European funding market remains more diverse than its US counterpart. Whereas US ‘pure’ AI raises were 78% of the total in Q1, in Europe the equivalent figure was just 20%. If we look at AI and related industries (AVs, robotics, quantum, data centres, legaltech) the US total was 87% of the value of raises. In Europe it was 45%.

Q1 2026 – European Growth equity’s $18bn of fundraising ranked by sector

Unicorn creation suggests buoyant valuation trends

The buoyant conditions for fundraising in Europe are reflected in the level of creation of new unicorns. Q1 2026 saw 15 new unicorns created in Europe. As the chart, sourced from Pitchbook, shows this is the highest level of European unicorn creation since Q2 2022, when 22 unicorns were created. Between Q3 2022 and Q4 2025, unicorn creation ranged between three and nine per quarter.

European Unicorn creation – 15 in Q1 2026, highest since Q2 2022

The fifteen Q1 unicorns are outlined in the table. It is a diverse bunch with two AI businesses, and several more AI oriented operations including Olix Computing in semiconductors, the AI datacentre operator Nscale, quantum computing operation Pasqal, and Neura Robotics. There are two fintechs, the crypto market-maker Keyrock, and debt analytics business, 9fin.

The valuations of defence businesses in this environment are highlighted by the $1bn valuation given to drones’ business Uforce in its first raise of $50m. Roark Aerospace, another autonomous defence systems business, attracted a valuation of $1.8bn.

There is one new software unicorn and two in cybersecurity.

Europe – The 15 unicorns created in Q1 2026

North America is seeing a similarly buoyant rate of unicorn creation. Q1 2026 saw 66 new unicorns created, in this case the highest number since Q1 2022, just after the 2021 peak of the VC market. It is more than double the number of unicorns created in Q1 2025. As the chart shows recent quarters have seen a sharply rising trend in terms of US unicorn creation.

North America: Unicorn creation – 66 in Q1 2026, highest since Q1 2022

Europe launches €15bn fund of funds

The European Investment Fund’s ETCI 2 initiative targets a €15bn fund of funds to unlock up to €80bn in scale-up capital across Europe.

We have observed in recent editions the depressed state of fund raising for VC firms even as investment in growth companies has been in a robust state. According to Pitchbook, capital raised in 2025 for European VC vehicles reached its lowest point since 2014. It mirrors the trend seen globally. Reports suggest that 2026 has also started sluggishly for European VC firm fundraising.

Global VC fundraising activity – sharp decline in 2025

We have charted in other editions of the Growth Equity Update the nature and level of state support for the venture industry. The EU is also supportive. The European Tech Champions initiative was launched in 2023. As part of this, in the next few months the European Investment Bank (EIB) will launch a second iteration of its European Tech Champions Initiative (ETCI), with the aim of supplying critical European late-stage funding.

Its first fund of funds raised €3.9bn and has backed 14 €1bn+ funds from VC firms including Atomico, Headline and Eurazeo which in turn have invested in 35 European technology scale ups. This first ETCI fund of funds was backed by the EIB and six EU states - Germany, France, Italy, Spain, Netherlands and Belgium.

EIB President Nadia Calviño stated at the end of January that:

“We are currently working on the expansion of this very successful European Tech Champions Initiative, so that it can scale up and make a difference in closing the financing gap with the US."

A second fund of funds is planned which is intended to attract support from a wider range of EU states and to be much bigger in size at c€15bn. The aim is to attract a broader set of investors including insurers, commercial banks and pension funds, alongside the public backers with the EIF and EIB having already committed €1.25bn to the new fund.

The intention is to fortify the part of the capital markets that helps new companies scale with the aim being to help fund 100 “mid-size” funds (€300m-€600m) plus mega funds (c€1bn), with a first close planned for summer 2026.

ETCI 2 will invest up to €200m per fund, substantially more than the €60m average seen with the first fund. The European Investment Fund hopes that the €15bn fund of funds will unlock up to €80 billion in scale-up capital across Europe.

In addition, and sitting alongside ETCI 2, is the European Commission’s planned €5bn Scaleup Europe Fund. This initiative is also launching in Spring 2026. Its aim is to invest in strategic tech sectors like AI, biotech and quantum, investing directly into companies looking for funding rounds of €100m or more.

Public markets – Geopolitics and earnings

The end of February saw the start of the most recent conflict in the Middle East, and this dominated markets in March. War is not good for markets. As the Straits of Hormuz closed, oil prices rose sharply and equity markets retreated. On the 8th of April, having threatened to destroy civilisation in Iran, the US thankfully stepped back, and an uneasy truce is underway which has the potential to turn into a lasting peace deal.

Markets gyrated around the geopolitical news. In March the two major US indices, NASDAQ and the S&P500, both fell about 5%. In Europe the FTSE 100 Index was down 7% in March and the STOXX600 was down 8%.

The indices started to turn around the end of March and then rallied on the announcement of the step back from the brink and the truce. NASDAQ is now flat since the end of February, the S&P 500 is down 1%, the FTSE100 down c3% and the STOXX 600 down 4%.

Since the start of the year the FTSE 100 leads, up 7%, the STOXX 600 is up 2% and the S&P500/NASDAQ are down c1-2%. The FTSE Venture Capital Index is down 20%.

The robust performance of the public indices since the end of February – and year to date – belies the negative implications of the Iran conflict, even if this has now peaked. Oil prices remain higher than they were prior to the conflict, some capacity has been destroyed, freedom of supply from the Gulf remains uncertain and supply chains have been disrupted.

The most obvious impact is the inevitable effect on inflation. The US CPI report for March, released on April 10, showed inflation at 3.3% versus the February read of 2.4% (and 2.5% core). The inflation figures though have less impact than normal as the market has already decided that the prospect for further US interest rate cuts in 2026 have all but disappeared. Expectations are that inflation will remain above 3% over the next year.

At the start of the year with no war, with the impending replacement of Fed Chair Jay Powell with Kevin Warsh (still not ratified) and with US inflation trending downwards towards the Fed’s 2% target and touching the lows of the previous five years, the expectation was for at least two rate cuts in the US in 2026, taking the Fed rate down from 3.5%-3.75% to 3%-3.25%, with the first rate cut expected in June.

FedWatch now has a 95% certainty of rates remaining unchanged at the June 17 meeting and a 67% expectation that rates will still be unchanged after the last meeting of the year on 9 December. Indeed, the market does not presently expect a rate cut until the September 2027 meeting.

The next debate will be about the level of earnings expectations. As we saw when we reviewed Wall Street strategists’ 2026 forecasts at the start of the year, earnings growth optimism was one of the mainstays of their bullishness on markets. Typically, year-end S&P500 targets of c.7,500 was predicated on strong earnings growth of 13%-15% pa in the next two years. Indeed, for the upcoming results season Wall Street strategists expect earnings growth of c13% with outsize contributions from Energy and tech stocks.

With the market apparently relaxing about geopolitical effects it may be time once again to think of the negative effect on Magnificent 7 earnings of the burgeoning capex requirements of the hyperscalers and the potential impact of the SaaS Apocalypse on the outlook for other tech companies’ earnings.

Meanwhile inflation is reported sharply higher in the Euro area. The March reading was 2.5% up from 1.9% in February on the back of a 4.9% rise in energy costs. February had already seen an unexpectedly strong rise in Euro Area inflation with the 1.9% well ahead of market expectations of 1.7%. At the start of the year the expectation was that European interest rates would likely be held flat in 2026. Just prior to the Iran ceasefire this had switched to an expectation of three 25bps rate rises in 2026. There is still an expectation of two 25bps rate rises by the end of the year.

A similar picture is seen for the UK where start of the year expectations of two 25bps interest rate cuts in 2026 have shifted to the expectation of a singe 15bps raise in rates.

The implication is that markets have overall continued to move ahead ytd, more noticeably in Europe than the US, but conditions in terms of the likely interest rate environment plus the effect of geopolitical effects on supply chains, costs and confidence have worsened.

Our Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian’s views on the current market outlook are summarised in the Exhibit.

Fundraising outlook: c$34bn of potential raises

Pipeline remains firm with c$26bn of impending US deals and $8bn in Europe.

Despite another strong month of deals in March the backlog of US impending deals has risen from $20bn to just over $26bn.

Heading the list is the defense business Anduril which is seeking to raise $8bn at a $60bn valuation with Thrive Capital and a16z leading the round. There were a couple of big defense deals in March, Shield AI, the developer of autonomous vehicles raising $2bn and autonomous ship business Saronic raising $1.75bn.

Project Prometheus, Jeff Bezos’ ‘AI for the physical economy business’ is reportedly raising a further $6bn having landed $6.2bn as recently as February. Separately reports suggest that Mr Bezos is also trying to raise a $100bn fund to acquire parts of companies likely to be disrupted by AI. It is reportedly in discussion with sovereign wealth funds as part of this plan.

Reflection AI provides tools to create personalized AI that can chat and interact like a person. The NVIDIA backed business is looking to raise $2bn at a $20bn valuation.

Tether, the US/El Salvadorean stablecoin issuer, is raising c$5bn and possibly more at a putative $500bn valuation. Reports suggest that the company has initiated a two-week period for investor commitments and may delay its fundraising if the $500bn valuation target is not reached.

Other additions to the list this month are Aetherflux, a solar power in space business looking to raise $300m at a $2bn valuation and Fal, the AI video business looking to raise $300m at an $8bn valuation. Deletions from the list due to their recent raises include Shield AI ($2bn), Replit ($400m) and Harvey AI ($200m).

US Growth Equity – c$26bn in reported upcoming raises

In Europe, the total of identified impending raises drops from $9bn to $8.3bn

The upcoming raises list remains headed by the expected $2bn raise for the French AI coding business Poolside led by Magnetar and NVIDIA.

Added to the list is a planned is an up to $2bn raise for the German business, Neura Robotics at a $4bn valuation. Stablecoin company Tether is said to be supporting the raise. Neura’s flagship humanoid robot is the 4NE1 Mini – almost six feet tall, capable of carrying up to 220 pounds and to move at three miles per hour, with both consumer and industrial applications.

Italian LLM and AI infrastructure business, Domyn, is said to be raising $1.15bn in an upcoming Series B. Ineffable Intelligence of the UK is run by David Silver who pioneered AlphaGo at Google DeepMind. His approach to LLMs is that they cannot achieve superintelligence by being trained on human data but must instead use reinforcement learning – teaching itself instead. It plans a $1bn raise at a $4bn valuation to be led by Sequoia with NVIDIA, Google and Microsoft also said to be set to participate.

Also added to the list is a possible €250m ($287m) raise for Germany’s Isar Aerospace at a c€2bn valuation. The company is planning the second test launch of its Spectrum rocket. Its planned launch on March 26 has been delayed.

Dropping off the list of impending raises are Nscale, the UK datacentres business which raised $2bn in March, Advanced Machine Intelligence (AMI) Labs led by Yann LeCun, who was the key architect of Meta’s AI strategy, which raised $1.03b, higher than the expected $575m; and legaltech Legora which raised a $550m Series D.

European Growth Equity – c$8.3bn in reported upcoming raises

Fundraising - The onwards March

A record month for Europe with $7.7bn raised; US chips in another $30bn

March was another strong month for VC and growth equity fundraising on both sides of the Atlantic.

Europe saw $7.7bn raised across 60 deals, the biggest month by value since 2021, surpassing the $7.1bn of September 2025. The amount raised was double the $3.85bn of March 2025.

In the US, the total of $30.2bn raised in March 2026 is down 40% on the $50.7bn raised in March 2025, when OpenAI chipped in a $40bn raise. It is still a substantial number, being the sixth largest month since the start of 2024.

Europe – 60 raises of $20m + in March for a total of $7.7bn

US and Canada – 55 $100m+ deals raised $30.2bn in March

Our views on the state of the venture capital markets

This revival of the growth equity market has been led by the US and by a surge of interest in artificial intelligence model providers and for companies using AI to transform a range of underlying industries.

Ast the same time the venture industry has re-adopted strong underlying approaches to investment with companies in most sectors striving to achieve a better balance of growth, profitability, and cash flow. The underlying quality of the cohort of VC backed companies has improved.

Our summary of the outlook:

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, quantum, semiconductors, new energy sources like nuclear and fusion) supporting the development of AI.

- The influence of AI is percolating through many other industries such as drug discovery, defence, robotics, legaltech, autonomous vehicles, and cybersecurity fuelling a broader advance in the growth equity market.

- Overall, the VC market is regaining confidence with the strength of interest with fintech, blockchain/crypto and biotech reviving strongly.

- There is a burgeoning interest in defence industries from investors with both the tense geopolitical political environment, the advances in AI applications and the experience of the combat in Ukraine contributing to investor focus. By contrast, ClimateTech, while still a substantial sector has become less prominent both as a result of some high-profile failures and being less favoured politically in the US under the current administration.

- Fund raising for venture capital firms remains subdued. Fund raising is concentrating into larger, established firms. US VC fundraising in 2025 was concentrated in larger firms and at near decade lows.

- The speed of the investment process has slowed down since 2021-22. The level of diligence on deals has stepped up. This is true even in the ‘hot’ parts of the market like AI. Outside these areas it is marked – processes take time, downside protection is sought.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on the combination of growth and profitability (or a rapid path to it) and on free cash flow.

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025, April 2025, May 2025, June 2025, July 2025, August 2025, September 2025, October 2025, November 2025, December 2025, January 2026, February 2026, March 2026

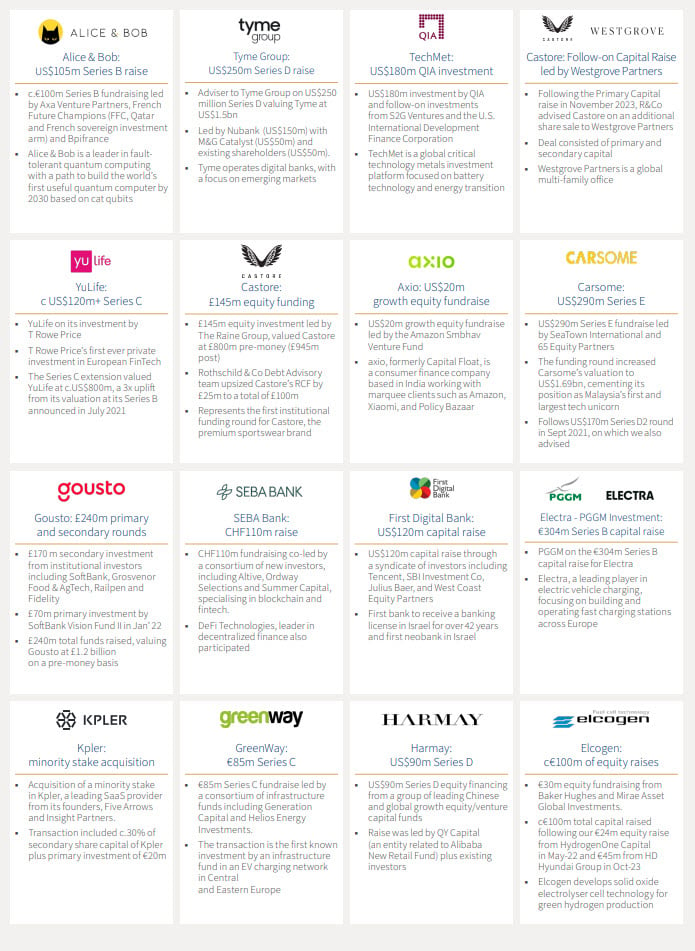

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Mark Connelly

Co-Head of Global Market Solutions

+1 212 403 5500

+1 917 297 5131

Chris Hawley

Global Head of Strategic and Private Investors.

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Capital Markets Europe

+44 20 7280 5088

+44 7542 477 291

Antoine de Guillenchmidt

Co-Head of Equity Capital Markets Europe

+44 20 7280 5377

+44 7907 712 978

Pete Nicklin

Co-Head of Equity Capital Markets Europe

+44 20 7280 1668

+44 7912 395 294

Laura Klaassen

Head of Private Distribution

+44 7926 905 488

Thomas Chung

Head of Private Capital, North America

+1 212 403 5559

+1 917 594 7208

Tim Brenton

Director of Private Distribution

+44 20 7280 1351

+44 7788 395 556

This document is being provided to the addressed recipients for information only and on a strictly confidential basis. Save as specifically agreed in writing by Rothschild & Co Equity Markets Solutions Limited (“Rothschild & Co”) this document must not be disclosed, copied, reproduced, distributed or passed, in whole or in part, to any other party.

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.