The AI-driven surge

Amidst all the macro and political events on stage last week, the spotlight was on a single stock. It received a standing ovation.

Nvidia's revenues almost quadrupled in the final quarter of 2023 – largely due to its data centre division – while its net income increased nearly nine-fold to $12 billion. Its share price has increased by 60% this year, after more than tripling in the prior calendar year (overall, it has risen over five-fold since the start of 2023). Its market capitalisation is now roughly $2 trillion, though it is still only two-thirds of the biggest player, Microsoft.

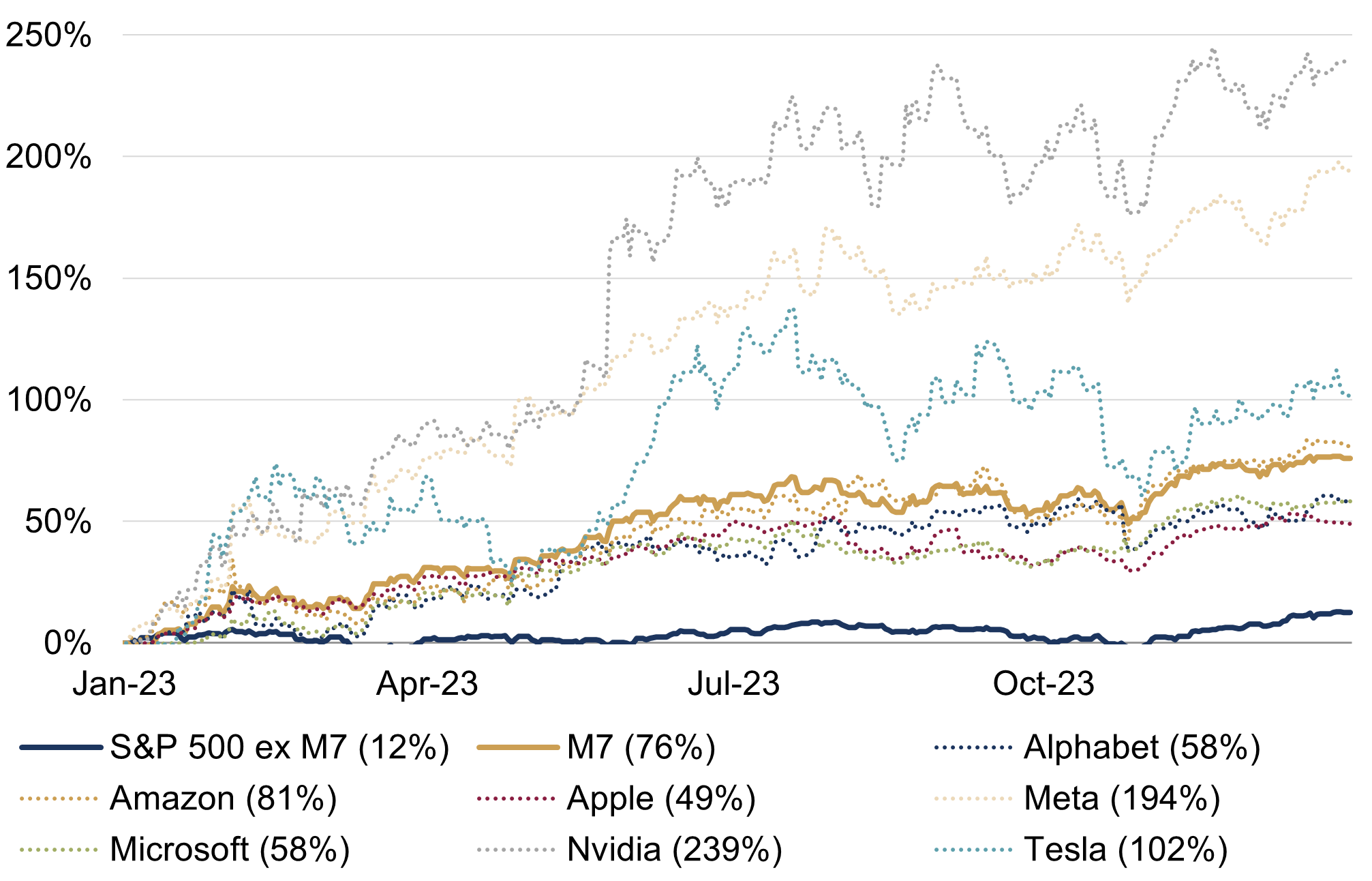

This semiconductor juggernaut is part of the so-called 'Magnificent Seven' – a US 'technology' cohort which also consists of Alphabet, Amazon, Apple, Meta, Microsoft and Tesla. Remarkably, the Magnificent Seven rose by 76% on a market-cap weighted basis in 2023 – after a sharp sell-off in the prior year – while the remaining 493 stocks in the S&P 500 were up by 12% (figure 1).

Figure 1: US stock market returns

2023 total returns (USD, %)

Source: Rothschild & Co, Bloomberg

It is perhaps a little unusual to see these 'technology' names outperform given the sharp rise in long-term interest rates – and the subsequent impact this might have on the value of their future cashflows. This sector is often thought of as 'long duration': it can be particularly vulnerable to interest rates, as its cashflows extend a long way into the future due to its high expected growth.

However, the Magnificent Seven are mega-cap names which were already very profitable to begin with, while their large cash balances and little debt mean they could have even benefitted from higher interest rates in some respects. Interest rates have been rising from extremely low levels that were arguably never priced-in to begin with. And perhaps most importantly, breakthroughs in 'Generative Artificial Intelligence (GAI)' – reflected in the launch of ChatGPT in late 2022 – have the potential to greatly boost these firms' future profitability.

Narrow market leadership

A highly concentrated US market advance is not a new phenomenon – for instance, the run up to the dot-com bubble at the turn of the century; and more recently, the 'FAANG stocks' during the post-pandemic rebound.

Still, last year's AI-driven surge was the 'narrowest' in recent decades. The Magnificent Seven accounted for most of the S&P 500's 26% total return, and the contribution from these seven stocks to the overall index was more than a four standard deviation event – put simply, it was highly unusual.

The Magnificent Seven's lead over the remainder of the stocks in the S&P 500 has not been as pronounced this year – they are only ahead by five percentage points – as the bloc's performance has become more fragmented (Tesla is down by a fifth, for instance). Even so, other members within the Magnificent Seven have continued their ascent, with Nvidia alone accounting for more than a quarter of the S&P 500's year-to-date return. On the other side of the pond, European stock indices have also experienced historically concentrated returns this year (last year's returns were not that narrow). For example, ASML and Novo Nordisk have accounted for 40% of the Euro Stoxx 600 index's returns to date, and the contribution is closer to 60% if SAP and LVMH are included.

It's debatable as to how troubling a highly concentrated market advance is (assuming of course that it does not reflect anti-competitive practices). What matters to us as investors are aggregate earnings and market capitalisation. At the market level, it is average valuations that drive our decision to invest. If the stocks with the highest prices have the lowest earnings, it can feel a bit unsettling – that does not seem to be the case today, though.

This is not another dot-com bubble

The current GAI-driven stock market gains have been compared to the TMT bubble, which burst in 2000.

However, valuations back then were much higher. Some of the top 10 index contributors – such as Cisco Systems and Oracle – were trading on forward price-earnings (PE) multiples of more than 100X. There were even popular stocks which had no revenues, let alone earnings, and new metrics were created to justify their lofty price tags (a personal favourite was 'eyeballs' – how many views does a company's website generate?). Today, aside from Tesla, most of the Magnificent Seven cohort don't appear that expensive: for instance, the bloc's 12-month forward PE ratio is above 30X (meanwhile, Tesla's is almost double).

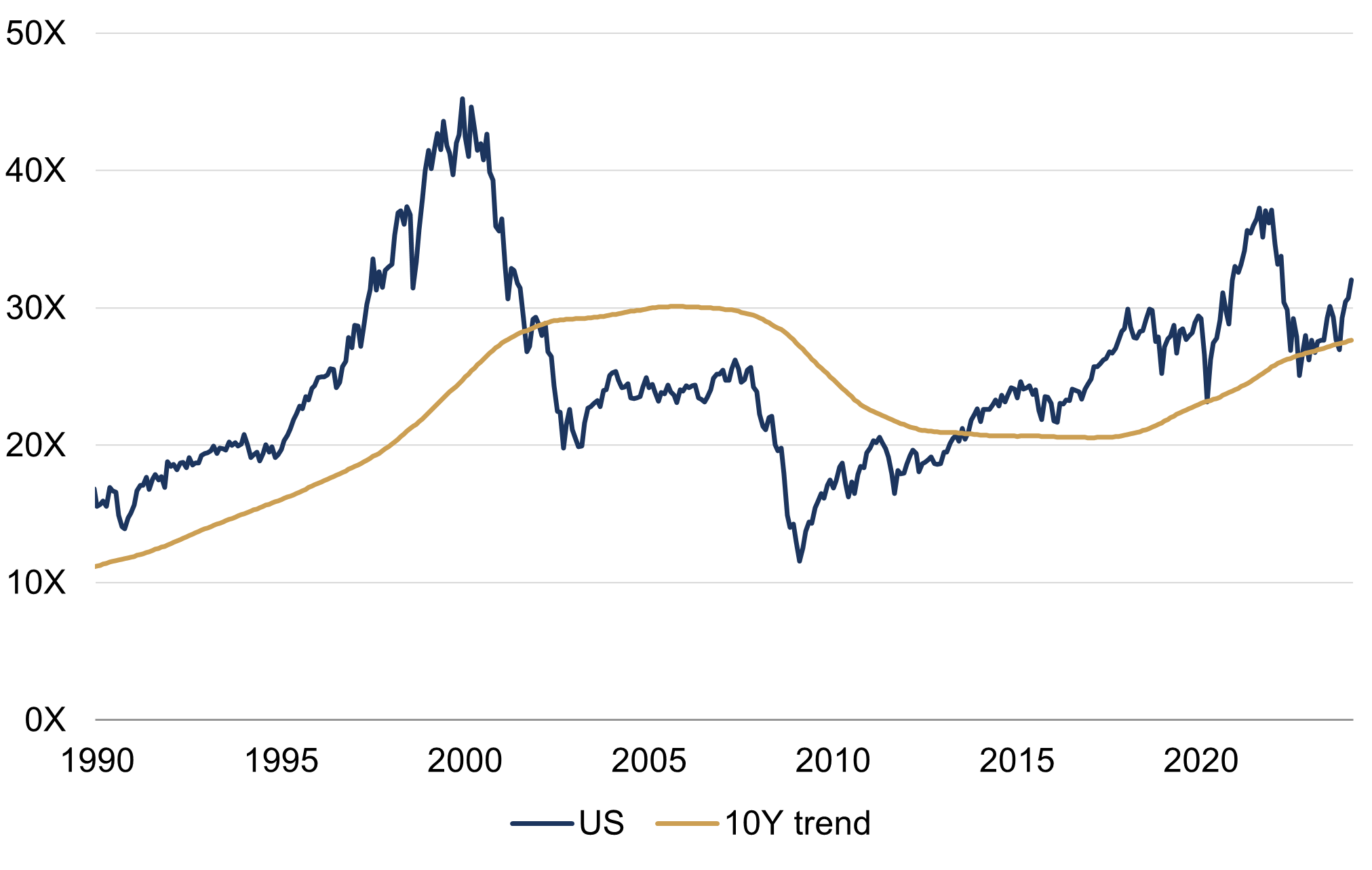

At the aggregate level, the US stock market does look somewhat expensive today, but not alarmingly so. Our preferred long-term valuation metric, the Cyclically-Adjusted PE (CAPE) ratio – which compares the inflation-adjusted price with the inflation-adjusted trend in earnings – reveals that US stocks are one standard deviation above their 10-year moving average (figure 2). During the dot-com bubble, they were more than two standard deviations above that threshold – and the level of the CAPE ratio was above 40X, compared to just over 30X today. Moreover, on an equal-weighted basis, the index appears inexpensive, suggesting that the average stock is cheaper than its Magnificent Seven peers.

Figure 2: US Cyclically-Adjusted Price-Earnings ratio

Relative to 10-year moving average (X)

Source: Rothschild & Co, Bloomberg, Datastream

Of course, stock market valuations are not a good short-term predictor. But they can matter more when they have been at extreme highs or lows, and so are ripe for a reversal. That does not appear the case this time.

Admittedly, last year's stock market rally was driven primarily by the big rerating in valuations, rather than earnings – implicitly, by expected jam tomorrow, not today. But the AI-driven improvements in the Magnificent Seven's fundamentals have started to show (as noted at the start). Return on equity – a gauge of profitability – is at a striking 30% on a 12-month forward earnings basis.

We think there is more substance behind today's rally. If there are parallels with earlier market fads, arguably the Nifty Fifty episode in the 1960s, characterised by large-cap 'growth' firms with high valuations, is a better comparison. The Nifty Fifty did eventually disappoint – but in the context of the stagflationary 1970s and early 1980s, rather than in a 'bubble bursting' way. Many of the stocks went onto perform again, as many of the businesses continue to produce cashflows today.

The cyclical and structural story

If the Magnificent Seven were to falter, the unremarkable valuations in other sectors and regions – and continued subdued expectations for growth and profitability – suggest that the global stock market might stumble, but not slump.

Over a longer timeframe, there is no doubt that the latest AI developments are good news for stocks. Technological progress and innovation are ultimately the long-term drivers of economic growth, and key shapers of corporate profitability. The Nvidia CEO suggested that accelerated computing and GAI had reached a 'tipping point' at last week's earnings call. Even if this is an exaggeration, other companies stand to benefit from the positive externalities associated with the sector's productivity-boosting breakthroughs.

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

The perils of making predictions

Quarterly Letter

History is littered with examples of people making predictions that later turned out to be inaccurate. How can we become better at forecasting the future? Our Quarterly Letter delves into this topic to investigate some of the perils of making predictions.

-

Rothschild & Co’s UK Wealth Management business names James Morrell as Deputy CEO

Actualités

The newly created Deputy CEO role will provide increased capacity at a senior level to help meet the growing demand for Rothschild & Co’s wealth management services from existing and future clients.

-

Rothschild & Co wins Western Europe's Best Bank for Advisory from Euromoney

Récompenses

This is the second consecutive year we have been named Western Europe's Best Bank for Advisory, reflecting the breadth of our capabilities across M&A and financing advisory across the region.

-

Growth Equity Update

Publications

The July edition assesses the condition of Growth Equity at the year’s halfway stage. H1 was again tough for fundraising for VC firms. Q2 though was much stronger than Q1 and into July with the mood amongst VC funds, and their fundraising, bolstered by the surge in appetite for AI related investments.

-

Rothschild & Co hires Brandon Aebersold and Parry Sorensen as Managing Directors in North America

Actualités

Senior hires bolster the firm’s Restructuring team in the United States.

-

Asset Management: Monthly Macro Insights - July 2024

Market Commentary

Business confidence fell at the end of Q2-24, casting doubts on the positive momentum going into the second half of the year, while rising political uncertainty add to an already complicated conduct of monetary policy.