Growth Equity Update

March 2026 – Edition 48

- Extraordinary February for US fundraising: February saw 66 US rounds of $100m+ raise $181bn, the biggest month ever for growth equity raises. It was a 24-fold increase on February 2025. YTD US fundraising is up 11.5x yoy at $216bn, just $18bn short of the total for all of 2025.

- In Europe 51 deals raised $4.8bn in February, +92% yoy. YTD raises are +36% at $10.1bn.

- February’s largest deals: We analyse three of the biggest deals of the month - OpenAI’s $110bn raise at a $730bn pre money valuation; Anthropic’s $30bn Series G at $380bn; Waymo’s $16bn raise at $110bn, plus in Europe, Wayve’s $1.2bn Series D at $8.6bn post money.

- UK National Wealth Fund - first new mandate investment: Under its new mandate the NWF, the UK government’s principal investor with £27.8bn of capital, will provide growth capital (£25m-£100m+) to scale businesses ‘with proven technologies, credible business plans, and strong management teams.’ Its first investment is $50m to AV company Oxa.

- Software and the ‘SaaS apocalypse’: Both the S&P500 Software and Services index and the S&P Listed Private Equity Index (software accounted for 18% of 2025 US private equity deal value) are down c16% ytd. Concerns over the impact of agentic AI mean Software and SaaS raises will be scrutinised even more fiercely for their potential vulnerability to AI disruption.

- Latest Lux report: The Q4 report from US VC firm Lux Capital (c$7bn in assets) observes ‘Audiences grok what many sector analysts haven’t yet comprehended: the next decade of wealth creation will look more like Landman than The Social Network: capital-intensive, physically constrained, and far more dependent on legal permitting and infrastructure access than genius coding…. The hero has changed: from the coder nerd moving fast and breaking things to the politically connected engineers navigating the brutal physics of the real world.'

- Iran conflict and public markets: Fast moving. War is bad for markets. The oil price at $100 is sparking inflation fears. The market has now swung round to fearing a Euro Area rate rise in 2026 while expectations for US rate cuts in June have faded.

- $29bn of impending raises. Our monitor of forthcoming rounds, depleted by recent big announcements, still charts c$20bn of impending raises in the US and $9bn in Europe.

Download a PDF version of the Growth Equity Update

February's big raises

February was a remarkable month for growth equity raises in the United States. Our Rothschild & Co Monitor of raises of $100bn or more counted 66 raises for a total of $181bn. Three raises comprised $156bn, 86% of the total. They were $110bn for Open AI led by NVIDIA, Amazon, and SoftBank; $30bn for Anthropic led by Coatue, Dragoneer, Founders Fund, GIC, Iconiq, MGX and DE Shaw and Waymo at $16bn led by Alphabet, Dragoneer, DST Global and Sequoia.

Let’s take a closer look at these three raises:

OpenAI – Compute, distribution, and capital.

$110bn in new investment at a $730bn pre-money valuation.

The OpenAI deal was announced by the company on February 27. Its statement observed that.

AI demand is surging across consumers, developers, and businesses. Meeting that demand and providing everyone access to our products requires three things: compute, distribution, and capital.

The funding includes $30B from SoftBank, $30B from NVIDIA, and $50B from Amazon. We’ve also signed a strategic partnership with Amazon and secured next generation inference compute with NVIDIA. Additional financial investors are expected to join as the round progresses.

The Amazon partnership: It’s a $50bn pledge but it doesn’t come all at once.

- The initial commitment is a $15bn investment in the form of OpenAI Series C preferred stock and payable by March 31.

- The remaining $35bn will follow in the coming months when certain conditions are met. Amazon has the discretion to commit these funds whenever it chooses. There are two events though that could automatically trigger the investment. These are a ‘mandatory funding event’ the nature of which is not spelled out by the filings. The other is an IPO of OpenAI – Amazon has five working days to buy the shares post the filing of a public S-1 by OpenAI.

There has been widespread speculation of an OpenAI IPO in 2026, and CEO Sam Altman reiterated on the announcement of this round that the company is ‘open to going public at the right time.’ The Amazon commitment is time-limited, expiring at the end of 2028 if an IPO hasn’t by then taken place.

In the self-referential world of these major fundings there are a series of agreements between buyer and client company. In this case there is a Joint Collaboration Deal. Maintenance of this is also a condition of the $35bn incremental investment. Open AI has now expanded its pre-existing $38bn cloud services deal with AWS to a $100bn eight-year deal including a commitment to use two GW of Trainium capacity. The Trainium AI chip is Amazon’s alternative to the NVIDIA GPU.

There is an agreement to form a ‘Stateful Runtime Environment.’ Here OpenAI models will run on AWS’s model platform, Amazon Bedrock. The environment allows the models to learn, manage context and recall previous work.

The Open AI commitment is part of the $200bn capex programme already announced by Amazon.

What about Microsoft? As we noted in the February Growth Equity Update, Microsoft was a major investor in the $40bn raise for Open AI in March 2025 and is believed to have a 27% stake in the business. It was not, however, an ostensible participant in this $110bn funding round. Nevertheless, OpenAI and Microsoft also put out a joint announcement on February 27. Despite announcing $110bn in new financing from different partners and new operating agreements with Amazon OpenAI was anxious to point out that:

‘Nothing about today’s announcements in any way changes the terms of the Microsoft and OpenAI relationship.’

This optimistic sentiment is reinforced by OpenAI observing that its Microsoft partnership remains ‘strong and central’ and that its ‘IP relationship continues unchanged’ (a key point as it underpins Copilot, Bing, and Azure Open AI) as do its revenue share arrangements.

Microsoft Azure ‘remains the exclusive cloud provider of stateless OpenAI APIs.' These are a basic form of AI prompt, unlike stateful APIs that can hold the thread of a connection across multiple interactions.

The October 2025 ‘Next Chapter’ announcement between the two parties stated, amongst other things, that ‘OpenAI can now jointly develop some products with third parties. API products developed with third parties will be exclusive to Azure. Non-API products may be served on any cloud provider means.’ This latest funding deal reinforces that with exclusivity dropped and OpenAI engaging now with other operational – and now financial – partners.

And NVIDIA? NVIDIA is a seeming ever present in AI related deals these days and this one was no exception. Despite OpenAI committing to work with Amazon on its rival chip Trainium to the NVIDIA GPU series, NVIDIA was in the round for $30bn. Again, there was a commitment by OpenAI to collaborate with NVIDIA.

‘We are also expanding our long-standing collaboration with NVIDIA, including the use of 3 GW of dedicated inference capacity and 2 GW of training on Vera Rubin systems. This builds on Hopper and Blackwell systems already in operation across Microsoft, OCI, and CoreWeave. Together, this capital and infrastructure expansion strengthens our ability to train and deploy frontier models at global scale.’

Nevertheless the $30bn appears to come in place of what had previously been a long-term commitment of up to $100bn agreed by NVIDIA with OpenAI in September 2025. This heads of agreement had envisaged NVIDIA investing $100bn in OpenAI in chunks of $10bn each as OpenAI bought NVIDIA processors in pursuit of its plan to amass 10GW of additional compute capacity. This now appears to have been replaced by a simple $30bn investment in Open AI stock.

And SoftBank? The $30bn investment will be made via the Softbank Vision Fund 2. SoftBank observes that post completion its cumulative investment in OpenAI is expected to total $64.6bn, representing an ownership interest of approximately 13%. The investment will be made in three tranches, payable on April 1, July 1, and October 1, 2026. SoftBank says.

‘The Follow-on Investment is expected to be financed initially through bridge loans and other financing arrangements from major financial institutions and subsequently replaced over time through the utilization of existing assets and other financing measures.’

Masayoshi Son, Chairman & CEO of SoftBank Group Corp emerged from the difficult VC markets of 2021-23 with an AI mission describing his view that AI superintelligence ‘will be ten thousand times more intelligent than humans and realized in about ten years. The realization of ASI, which will far surpass human wisdom, will mark a turning point in human history… ASI is the latest means by which we fulfil our mission to drive the evolution of humanity forward.’

On the latest OpenAI deal he commented: “AI is transforming the world at an unprecedented pace. OpenAI is a clear leader, with world-class technology and an unparalleled global user base, and we have strong conviction in its continued growth. Through this additional investment, we will accelerate OpenAI’s research and ecosystem expansion, while advancing our own ASI strategy.”

Responding to Masayoshi Son’s vision of what is good for everyone else, S&P Global lowered its outlook for SoftBank Group from stable to negative observing the $30bn OpenAI investment may hurt SoftBank’s liquidity and the credit quality of its assets. It commented

“The company’s investments in AI, including OpenAI, mostly involve fledgling startups and private companies that we believe are exposed to significant AI innovation risk and fierce competition… We see OpenAI as one of its investments with the weakest credit quality.”

For reference OpenAI had revenue of $13.1bn in 2025 and had negative FCF of c$8bn. Annual Recurring revenue (presumably December annualised) at end 2025 was $20bn. The company targets c$280bn of revenue by 2030, substantially larger than Meta’s 2025 revenue of $201bn. It had previously talked of ‘hundreds of billions’ by 2030. It is targeting $600bn in total compute spend by 2023. Press reports (the Information) suggest that 2023-28 OpenAI will report cumulate losses of $44bn before turning profitable in 2029.

Anthropic – ‘Claude is increasingly becoming critical to how businesses work’

$30bn Series G at a $380bn post money valuation

On February 12 Anthropic announced that it had raised $30bn in Series G funding led by GIC and Coatue, valuing Anthropic at $380 billion post-money. The round was co-led by D. E. Shaw Ventures, Dragoneer, Founders Fund, ICONIQ, and MGX. An A- Z of a further thirty blue chip venture firms (from Accel, through Menlo Ventures to XN) were cited on the announcement.

Some observations

It’s a $30bn round, but not all of it is new. The Anthropic announcement notes that the round ‘includes a portion of the previously announced investments from Microsoft and NVIDIA.’ Those announcements were made in November 2025 when NVIDIA committed $10bn and Microsoft $5bn to Anthropic. It is not clear how much of that $15bn subtotal is included in the $30bn figure announced this time.

Investment and partnerships: In the November announcement Anthropic pledged to scale its Claude LLM on Microsoft Azure. Anthropic committed to purchase $30bn of Azure compute capacity and to contract additional compute capacity up to one gigawatt. Anthropic and NVIDIA announced a collaboration on design and engineering, aimed at optimizing future NVIDIA architectures for Anthropic workloads. Anthropic made an initial compute commitment of up to one gigawatt of compute capacity with NVIDIA Grace Blackwell and Vera Rubin systems. Amazon remained Anthropic’s primary cloud provider and training partner.

What about Coatue? They like Anthropic. The team led by Thomas Laffont observes.

‘At Coatue, we focus on big ideas – our belief is that in technology, a select few companies produce the disproportionate share of outcomes. Each decade and architectural shift produces a handful of companies that have the potential to reach trillion-dollar market caps. We believe Anthropic is one of them.

As we draft this post, we’re burning through Opus tokens, building Claude Skills to web-fetch earnings transcripts, and getting a series of Claude Code agents to run data analysis scripts for hours in the background.

At Coatue, we have the privilege of experiencing technology shifts earlier than most. With 35 data scientists and engineers, we are still early in unlocking Claude’s full potential, yet it is already reshaping how we operate – and how many other organizations do as well.’

It also produces a couple of handy charts. The first one both highlights the scale of the capability advance in the latest Claude Opus 4.5 model and plays into the fears of the ‘SaaS apocalypse’ for software companies we wrote about in the last Growth Equity Update.

Coatue highlights that ‘One fun chart we like to update is Claude Code activity on public GitHub repos [ A public repository where you can store your code, revisions, and files…Ed]. The chart shows the percentage of Claude commits over time, with a sharp inflection following the launch of Sonnet 4.5.’

As Coatue observes Fall 2025 marked a clear acceleration.

And what about revenues? From a standing start in January 2023 Anthropic is claiming a $14bn run rate in mid-February 2026 (the last month’s revenue x12?), up from $1bn for the same metric in January 2025.The company gets about 80% of its business from enterprises. Anthropic notes,

‘The number of customers spending over $100,000 annually on Claude (as represented by run-rate revenue) has grown 7x in the past year. …. Two years ago, a dozen customers spent over $1 million with us on an annualized basis. Today that number exceeds 500.’

Waymo – ‘the age of autonomous mobility at scale has arrived’

$16bn raise valuing the company at $126bn post money

On February 2nd autonomous vehicle company Waymo raised $16bn at a $126bn post money valuation in a round led by Alphabet, Dragoneer, DST Global, and Sequoia and including significant investments from Andreessen Horowitz and Mubadala and eleven other high profile venture firms. At the same time Waymo reaffirmed Alphabet’s ‘sustained support as our majority investor.’

Employing a slightly unfortunate phrase in the context of road safety, Waymo observes that

‘This infusion of capital will ensure we are positioned to move forward with unprecedented velocity.’

Alphabet and Waymo: Alphabet is the key player in the Waymo story as it is the majority owner of the business. The company was originally Google’s self-driving project which started in 2009. It was established as a separate entity, still owned by Google (now Alphabet), and given the Waymo name in 2015. It is reported in the ‘Other Bets’ division of Alphabet.

Introducing new investors: Gradually outside shareholders have been introduced into the Waymo share capital with successive raises of $2.5bn, $3.5bn and in October 2024 a $5.6bn Series C valuing the business at $45bn. This brought total external investment to $11.6bn. At the same time Alphabet committed to a further $5bn multiyear investment in Waymo.

The new round brings in a further $16bn to the business. It appears to be all from external investors. Alphabet remains the ‘majority investor.’

At the time of the 2024 raise Waymo One’s ‘robotaxi’ ride hailing service operated in San Francisco, Phoenix, and Los Angeles, and in partnership with Uber, in Austin and Atlanta. The service was extended to Miami in January 2026. In total there were 15 million trips in 2025.

The intention, backed by the new funding, is to launch in 2026 in Dallas, Denver, Detroit, Houston, Las Vegas, Miami, Nashville, Orlando, San Antonio, San Diego, and Washington. There are also plans to launch the first international services in London and Tokyo.

Wayve - Autonomy for any vehicle, anywhere

$1.2bn Series D at a post money valuation of $8.6bn

And finally, a European raise, the $1.2bn Series D for Wayve, the largest raise in Europe since Mistral’s $2bn in September 2025. The round was led by Eclipse, Balderton and SoftBank Vision Fund 2. It was supported by Ontario Teachers’ Pension Plan, Baillie Gifford, British Business Bank, Icehouse Ventures, and Schroders Capital and other global institutional investors.

Commercial players also involved: Microsoft, NVIDIA and Uber participated in the round. Uber is potentially committing another $300m which would take the total raise up to $1.5bn. This is dependent on plans for multi-year deployments of Wayve-powered robotaxis on the Uber network. The intention is to scale to more than 10 markets globally with the launch of the first service in London in 2026, with broader international rollout to follow.

Nvidia has been working on product development with Wayve since 2018. Wayve’s Gen 3 platform uses the Nvidia Drive AGX Thor in-vehicle compute autonomous vehicle kit. In turn the Nvidia Drive kit is built on Arm NeoverseV3AE CPUs. Softbank, one of the leaders of the round, is the c90% owner of Arm.

The Gen 3 platform will allow Wayve to offer eyes-off advanced driving-assistance systems and Level 4 (fully driverless) features.

Wayve uses Microsoft Azure, Azure Databricks, Azure AI infrastructure, and the Azure Kubernetes service to connect thousands of GPUS into a flexible supercomputer to train and validate its AI model for autonomous driving. In October 2025, Wayve and Microsoft signed a new deal extending Wayve’s use of Azure services under a Strategic Framework Agreement.

Automotive partners as well: Automakers Mercedes-Benz, Nissan, and Stellantis also participated in the raise. Each plan to use Wayve’s technology. In April 2025 Nissan announced it would use Wayve’s self-driving software to support its ProPilot advanced driver-assistance system starting in 2027.

Some Updates

The National Wealth Fund – first new mandate investment is in Oxa

In our last edition we outlined the new strategy of the UK’s National Wealth Fund. The NWF is the UK government’s principal investor and policy bank with £27.8bn of capital, whose strategic aim is ‘mobilising finance, unlocking growth’.

The NWF will provide growth capital to scale up businesses ‘with proven technologies, credible business plans, and strong management teams.’ Its focus is on later funding rounds looking to take minority positions investing alongside institutional investors and seeking to unlock further significant finance over time. Its private investments typically exceed £100m and must be a minimum of £25m.

The first investment we have seen under the new plan is the NWF’s participation in Oxa’s $103m Series D round. Oxa is a developer of autonomous vehicle technology (it’s been a big month for such companies). The investment will enable Oxa to focus on commercialising solutions for Industrial Mobility Automation (IMA), which involves the automation of repetitive industrial driving tasks. It will also support the development of Oxa’s physical AI and robotics technology, notably its configurable self-driving software, Oxa Driver, and its development toolchain, Oxa Foundry.

One of the fifteen sectors earmarked for investment by the NWF is artificial intelligence and Oxa fits firmly into this bracket. The UK Government’s recent Advanced Manufacturing Sector Plan sets a target for the UK to become “a global leader in scaling up innovation and automation.”

Advanced Manufacturing, Digital and Technology and Transport form three core pillars of the National Wealth Fund’s new priority sectors, with this investment marking its first investment into Advanced Manufacturing since it was explicitly added to the mandate.

The NWF committed $50m to the round which was also supported by N Ventures (NVIDIA) and existing shareholders IP Group, Hostplus and bp Ventures. The second close of Oxa’s Series D is expected by the end of June.

Oliver Holbourn, the CEO of the NWF commented:

“The National Wealth Fund’s investment will give Oxa the support it needs to accelerate the scale and deployment of its ground-breaking technology, unlocking the potential in connected and autonomous mobility. This could provide a significant boost to growth and productivity in the UK, creating an industry worth billions of pounds, generating thousands of well-paid jobs and providing significant productivity benefits across many sectors.”

The SaaS Apocalypse and growth equity markets

We wrote extensively in the last Growth Equity Update about the market’s fears for software businesses at the hands of agentic AI disruption. The immediate Stock market focus has shifted to geopolitical issues and the military assault on Iran. The ramifications of the ‘SaaS Apocalypse’ though play out in the background. The S&P500 Software and Services index remains down around 16% ytd. Our sense is:

- The response is more calibrated than initially seen. Companies have crafted messages to investors outlining what they see as their defensive moats against AI business model disruption. Typically, these rest around entrenched positions with customers, understanding of intricate workflows, the mission critical nature of systems, proprietary data, the ability to link different public and proprietary data sources, privacy and security concerns, and the sheer disruption effect of changing systems.

- In some areas this is working. Legal data provider RELX, which we wrote about in the last Growth Equity Update, fell 22% in the period 2nd February -11th February but then rallied to close the month 3% higher than the start of February.

- What we are seeing is, we think, some cautious buying of fallen angels after an initial rather indiscriminate assault on potentially AI disrupted companies.

- Otherwise, we continue to see fund managers adopt the HALO (hard assets, low obsolescence) approach, favouring sectors and companies with real world assets deemed unlikely to be impacted by AI disruption – the so called ‘banks, tanks, and basics’ approach.

- The SaaS Apocalypse is not operating in isolation. The Stock Market has the pressing concern of the outbreak of hostilities in Iran and the spiking of the oil price to above $100 a barrel. In this environment the market’s response to the potential issues for software companies relying on per seat usage, on productivity tools or which employ complex user dashboards, becomes more muddied. The issue though will remain with us.

- The ripple effects of the ‘SaaS apocalypse’ are being seen through the private capital market already, with scrutiny on both private equity businesses and private credit funds who are large holders of software assets or software company debt. The software sector, according to Pitchbook, accounted for 18% of US private equity deal value in 2025. The S&P Listed Private Equity Index of publicly quoted PE businesses is down 16% ytd. Shares in Ares, Apollo, Blackstone, Blue Owl, and KKR are down 26%-35% ytd. CVC – which took care to point out in its FY 2025 activity update that ‘Software represents 7% of FPAUM, well below the industry average’, is down just 18% ytd.

- What about the growth equity market? At its simplest level, the concerns over the impact of agentic AI on software businesses will be greater scrutiny and scepticism around proposed software raises. Software and SaaS raises will be scrutinised even more fiercely under the lens of their potential vulnerability to AI led disruption. It will be an extra hurdle to climb in the fundraising process for such businesses.

Feedback from private investors suggests both additional caution in relation to the software sector but also consideration around differentiation and the potential to look for value. Here are some snippets of feedback.

- Bar has gone up on software; multiples have come down.

- Very unlikely to look at trades in the software space.

- In the current market the bar has gone up around new investments, but we are still looking for deals.

- The temporary dislocation is overblown but there is talk of a broader valuation reset between public and private companies.

- Greater focus on thesis and defensiveness of the story and AI risks. Looking also more for business enablers and best in class businesses

- Cautious around valuations

- In the world of AI, financial services are seeing more demand as more defensible.

- We are spending time distinguishing within software, which ones generally have a moat, access to data; regulatory barriers are important.

- There’s been a mismatch between buyer and seller price expectations over the last couple of years– we have started to see sentiment around this shift in the last few months.

- We see software dislocation as an opportunity.

The Lux Letter

Lux Capital is a Silicon Valley and New York based venture capital firm with around $7bn in assets under management, focused on early and growth stage deep tech. In January, it announced it had raised $1.5bn for its ninth fund focused on new science, defence, tech, and AI.

Each quarter its founders issue a quarterly report outlining some of their views on the state of venture investment and markets. The Q4 2025 report written by founder Josh Wolfe and published on February 21 has attracted some attention. The report is here Lux Capital Q4 2025 Report.

It is just one fund manager and one view but it’s an interesting one. Its theme is concentration and its merits allied with its risk. It observes (the passages in italics are verbatim from the Lux report).

Public market concentration: Markets are concentrated in fewer companies. Capital is concentrated in fewer managers. On market concentration: five companies now represent roughly 30% of the S&P 500’s market cap. The top 10 exceed 40%—the highest concentration in 50 years.

Concentration of risk: Hyperscalers have hyperscaled their spending to over $600 billion in the year ahead. Only the Louisiana Purchase of 1803 has exceeded their spend as a percentage of GDP (3% vs 2.1%). The current wave of tech capex (now over $1 trillion) exceeds the Manhattan Project, the Apollo program, the interstate highway system, and rural electrification combined, even as revenues remain in the tens of billions. Until recently, debt was mostly absent, dampening risk and keeping things comparably sober. It has now arrived at the party and even brought a plus-one in the form of off-balance-sheet funding structures. Debt is just dilution in disguise.

Concentration across the venture landscape: We see concentration across the venture landscape. Our long-expressed view of the coming extinction and involuntary exit of small VC funds (“minnows”) is empirically underway. Active VC firms declined 25% from around 8,000 in 2021 to 6,000 last year. First-time funds averaged just $7 million—less suited to venture and more a restaurant opening. The minnow extinction will accelerate and further concentration will follow. At the other end, the “Megas” are gathering assets at an increasing pace as predicted.

The surviving firms—including Lux—will enjoy less competition, better pricing power and most importantly, compounding relationships with coveted founders whom allocators will pursue for exposure and direct co-invests.

Concentration in deals: The concentration of private capital is only matched by the concentration in equities. Nearly $340 billion flowed into U.S. deals, the second-highest amount ever, yet it was packed into the fewest deals of the decade, with nearly half the capital concentrated in a few dozen deals over $500 million. The top 1% of companies by valuation now absorb a third of all venture capital deployed. The bottom half get 7%, technically “venture-backed” but also kind of like sitting in the parking lot at a concert and claiming you saw the show.

Half of all venture money went to 0.05% of deals, while half of all LP capital went to a handful of funds.

Real assets versus software: Picking up on the HALO theme Lux observes that the entertainment people watch frequently reflects a shift in attitudes towards what works in the cycle.

So, what is today’s signal? Landman. The zeitgeist is shifting from people who code bits to people who extract atoms. From equity investment to debt financing. From cap tables to mineral rights. From Palo Alto garages to West Texas lease agreements. From "growth solves all" to "cash flow pays interest." It’s less nostalgic and more anticipatory cultural positioning.

Audiences grok what many sector analysts haven’t yet comprehended: the next decade of wealth creation will look more like Landman than The Social Network: capital-intensive, physically constrained, and far more dependent on legal permitting and infrastructure access than genius coding. If capital goes where it’s welcome and stays where it’s well-treated, then this cultural moment—of pickup trucks and long drives to oil rigs with massive machinery that must be manned and maintained—anticipates a gusher of cash to physical assets (beyond just data centres) that are air gapped from software systems, isolated from AI disruption, and immune to automation. The hero has changed: from the coder nerd moving fast and breaking things to the politically connected engineers navigating the brutal physics of the real world.

Public markets - More conflict in the Middle East

The very end of February saw the start of the most recent conflict in the Middle East, and this has dominated markets so far in March. War is, simply put, not good for markets. The initial orderly retreat in market indices after the preliminary strikes shifted into a broader risk off move as the realisation came through that the conflict could be of lengthy duration and as the oil price spiked above $100 a barrel.

The rise in the oil price and in European natural gas prices have sparked fears of renewed inflation.

Bond yields rose markedly and the US dollar strengthened. Although still outperforming ytd the European markets’ outperformance of the US faltered as Europe is seen as more vulnerable to rising oil prices relative to the largely self-sufficient US.

At time of writing (March 9th) the FTSE 100 is up 2% ytd and the STOXX 600 is up 1%. The SP 500 is down 2% ytd and NASDAQ down 4%. The FTSE Venture Capital Index is down 12% ytd.

The mid-January BoA Global Fund manager survey had identified geopolitical risk as the greatest risk in markets, even above the risk of an AI bubble. At the same time, it measured global investor sentiment to be at its most bullish since June 2021.

As a result, there is substantial room for disappointment as the ramifications of the war with Iran are considered.

There was an unexpectedly strong rise in Euro Area inflation in February – up to 1.9%, well ahead of market expectations of 1.7%. Together with rising oil prices as a result of the Iran conflict, this has raised fears that the Euro area, instead of dropping rates, might be obliged to increase interest rates at some point in 2026.

Inflation in the US is still a concern as the secondary impacts of the oil price increase on other commodities like fertilisers are considered. US inflation had been trending downwards towards the Fed’s 2% target and are touching the lows of the last five years. The Iran conflict though has sparked a sharp reversal in the direction of inflation expectations with the market now expecting short term inflation rates to trend back up towards 3%.

Markets now expect US inflation to trend back up towards 3%

Clearly this has implications for the interest rate outlook in the United States. However so do the unemployment numbers. The market was surprised by the unexpectedly weak jobs report for February announced on March 6th. February saw the US lose 92,000 jobs (expectations had been for a rise of 55,000). The unemployment rate rose to 4.4% from 4.3%. Previous jobs reports totals were revised downwards with 69,000 jobs cut from the tally that had been announced for December/January combined.

The inflation expectations – if not yet the actual reports- are a disincentive to rate cuts. The unemployment numbers are an incentive. The third factor coming into play is Kevin Warsh as the new chair of the Fed. President Trump in December 2025 made it clear that a ‘litmus test’ in his choice of the new Fed chair would be their willingness to cut Fed rates.

The current Fed rate is at 3.5%-3.75%. The next Fed meetings are on March 18th and 29th April. The market’s view that there will be no rate changes at these meetings has strengthened. In mid-February Fed Watch had an 89%/79% chance of no rate change in the March/April meetings. Those figures have now strengthened to 97%/85%.

The key is the June 17 meeting – the first under the new Fed chair. In mid-February FedWatch had a 60% chance of a rate cut (49% of 25bps, 11% of 50bps) at this meeting. This has now reversed with a 63% chance of no rate cut, 33% at a 25bps cut and 4% at a 50bps cut.

In mid-February, the most favoured anticipated rate at the end of 2026 (the last meeting of the year is 9 December 2026) was 3%-3.25%, suggesting the market’s core expectation was 50bps of rate cuts in 2026. The most favoured anticipated rate is now 3.25%-3.5%, just a 25bps rate cut.

Our Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian’s views on the current market outlook are summarised in the Exhibit.

Fundraising outlook: c$29bn of potential raises

Big deals deplete the pipeline to c$29bn

At the start of the year, we identified c$160bn of impending raises in the US and Europe. Some big deals in February, notably the $100bn for OpenAI, $30bn for Anthropic and $16bn for Waymo plus, in Europe, the $1.2bn for Wayve, has depleted that number. We chart c$20bn of impending raises in the US and $9bn in Europe.

In the US we can see four impending deals of $1bn plus. The defence business Anduril is the most prominent VC backed defence business of the last couple of years. It is seeking to raise $8bn at a $60bn valuation with Thrive Capital and a16z leading the round. Also in Defence, Shield AI, a developer of autonomous vehicles is raising $1bn at a valuation of $12bn in a deal led by a16z.

Reflection AI provides tools to create personalized AI that can chat and interact like a person. The NVIDIA backed business is looking to raise$ 2bn at a $20bn valuation.

Tether, the US/El Salvadorean stablecoin issuer is raising c$5bn and possibly more at a putative $500bn valuation.

US Growth Equity - c$20bn in reported upcoming raises

In Europe, the upcoming raises list is now headed by the expected $2bn raise for the French AI coding business Poolside led by Magnetar and NVIDIA. Nscale, the UK datacentres business which raised ‘the largest ever Series B in European history’ at $1.1bn in September 2025 is said to be looking for a further $2bn in a Series C round.

Three AI businesses are raising funds. Italian LLM and AI infrastructure business, Domyn, is said to be raising $1.15bn in an upcoming Series B. Ineffable Intelligence of the UK is run by David Silver who pioneered AlphaGo at Google DeepMind. His approach to LLMs is that they cannot achieve superintelligence by being trained on human data but must instead use reinforcement learning – teaching itself instead. The $1bn raise at a $4bn valuation is being led by Sequoia with NVIDIA, Google and Microsoft also said to be set to participate.

Advanced Machine Intelligence (AMI) Labs led by Yann LeCun, who was the key architect of Meta’s AI strategy, is looking to develop ‘world models,’ sophisticated, forward thinking AI systems capable of planning complex actions. This intended ‘talent raise’ will be based in Paris and is looking at an initial $575m raise at a $3.5bn valuation.

European Growth Equity - c$9bn in reported upcoming raises

Extraordinary levels of fundraising in February

$181bn raised in a single month in the US

Remarkable levels of activity: Even before the $110bn OpenAI raise February was shaping up to be a remarkable month for fundraising in US growth equity. By the 26th of February US VC company fundraising had hit $70bn, 10x the amount raised in February 2024 and February 2025 – both of which were c$7bn. It was already the biggest month on record – beating the $50.7bn of March 2025 – which included the $40bn OpenAI raise. It included six raises of $1bn or more – Anthropic at $30bn, Waymo at $16bn, Databricks at $7bn, xAI at $3bn and World Labs and Cerebras at $1bn each.

At that point, the $110bn OpenAI raise was announced, valuing the business at $730bn pre money and backed by NVIDIA ($30bn), SoftBank ($30bn) and Amazon ($15bn initially). This brought the final monthly total to 66 rounds of $100m or more raising a total of $181bn. This is by some distance the biggest month ever for growth equity raises and maybe it will be the biggest to be seen for the foreseeable future with the likes of OpenAI planning to move to the public markets for future funding.

For the record, February 2026 saw fundraising increase 24-fold on the same month in 2025. Year to date US fundraising is up 11.5x over the same period in 2025 at $216bn. Indeed the $216bn is just $18bn short of the entire amount raised in 2025.

Eight of the top ten deals in the month were AI related with autonomous vehicle business Wayve coming in at third with a $16bn raise valuing the business at $126bn and robotics company Apptronik at eighth raising $935m for its humanoid robotics.

Outside of AI and related the ninth slot was taken by space company Stoke Space, which provides reusable space rockets and whose technology has considerable interest for defence. At tenth position Boulder Colorado based Vero Broadband is a communications company rolling out fibre to the premise. Tied in tenth place is MatX, a manufacturer of custom semiconductors for LLMs.

In total AI raises amounted to $153.8bn, 85% of the monthly total. Despite the recent violent public market rotation, software was the second largest category in the month with ten rounds raising just over $2bn, led by a $450m raise for restaurant commerce enablement platform inKind, $300m for fault tolerance software business Temporal Technologies backed by a16z, and $300m for aviation automation business Skyryse led by Autopilot Ventures.

ClimateTech chipped in $1.7bn of raises across seven rounds led by $450m for fusion energy business Inertia Enterprises and $425m for lithium-ion battery recycling business Redwoods Materials. Robotics, a branch of AI, was well represented with three rounds raising $1.35bn led by a substantial Series A of $935m for humanoids robotics company Apptronik led by VB Capital Group and Capital Factory.

Four raises in the Space Segment accounted for $1.24bn of funding led by the $610m raise for Stoke Space and a $350m raise for Axiom Space, a developer of human rated space infrastructure.

US and canada - 66 deals raised a record $181bn in February

In Europe 51 deals raised a total of $4.8bn in January, a 92% yoy increase on the $2.5bn raised in February 2025. The biggest deal of the year so far was the up to $1.5bn raised for the autonomous vehicle start up Wayve at an $8.6bn valuation. The round was backed by Softbank, NVIDIA and Uber with automakers Mercedes Benz, Stellantis and Nissan also participating. A key feature of Wayve’s technology is that it can operate in a wide range of vehicle types.

The Wayve raise was the second $1bn plus European funding round so far in 2026 after the $1bn raised for the software for utilities business Kraken in January. There were only two $1bn+ European rounds in the whole of 2025 (Mistral $2bn and Nscale $1.1bn) and we had to wait until September for them. In 2024 there was only one $1bn + raise – and that was also for Wayve at $1.05bn.

There were seven rounds for AI businesses raising a total of $0.95bn. These were led by the $500m for Eleven Labs, the AI voice generation business whose round was led by Sequoia. Fundamental A, a lab focused on the structured data produced by enterprises, raised $255m.

AI related industries were prominent. There were two raises for AI semis businesses. Axelera AI of the Netherlands raised $250m for its inference chips and the UK’s Olix Computing raised $220m at a $1bn valuation for its photonics for inference. Legaltech Lawhive raised $60m for its Lawrence interface which carries out consumer legal tasks and there was a $23m raise for R3 Robotics.

‘Pure’ AI raises accounted for 20% of the value of February’s raises. The figure rises to 62% taking into account AI related industries.

Elsewhere. Software was the second largest category with nine raises amassing $430m of which the largest was the $75m raised for Tem, a Dutch business with marketplace software for the energy industry.

Europe - 51 raises of $20m + in February for a total of $4.8bn

Our views on the state of the venture capital markets

October 12, 2022, marked the low point for the S&P500 on the back of global inflation, rising interest rates, and increased geopolitical risk. It also ended the buoyant market conditions for the venture capital market that saw its activity and valuations peak in late 2021.

October 12, 2025, marked the third anniversary of the bull market that has seen the S&P500 rise by almost 90% and NASDAQ by 120%.

In that period the FTSE Venture Capital Index was up by almost 170% and since June 2025 has been back above its previous 2021 peaks.

This revival of the growth equity market has been led by the US and by a surge of interest in artificial intelligence model providers and for companies using AI to transform a range of underlying industries.

At the same time the venture industry has re-adopted strong underlying approaches to investment with companies in most sectors striving to achieve a better balance of growth, profitability, and cash flow. The underlying quality of the cohort of VC backed companies has improved.

Our summary of the outlook

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, quantum, semiconductors, new energy sources like nuclear and fusion) supporting the development of AI.

- The influence of AI is percolating through many other industries such as drug discovery, defence, robotics, legaltech, autonomous vehicles, and cybersecurity fuelling a broader advance in the growth equity market.

- Overall, the VC market is regaining confidence with the strength of interest with fintech, blockchain/crypto and biotech reviving strongly.

- There is a burgeoning interest in defence industries from investors with both the tense geopolitical political environment, the advances in AI applications and the experience of the combat in Ukraine contributing to investor focus. By contrast, ClimateTech, while still a substantial sector has become less prominent both as a result of some high-profile failures and being less favoured politically in the US under the current administration.

- Fund raising for venture capital firms remains subdued. Fund raising is concentrating into larger, established firms. US VC fundraising in 2025 was concentrated in larger firms and at near decade lows.

- The speed of the investment process has slowed down since 2021-22. The level of diligence on deals has stepped up. This is true even in the ‘hot’ parts of the market like AI. Outside these areas it is marked – processes take time, downside protection is sought.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on the combination of growth and profitability (or a rapid path to it) and on free cash flow.

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025, April 2025, May 2025, June 2025, July 2025, August 2025, September 2025, October 2025, November 2025, December 2025, January 2026, February 2026

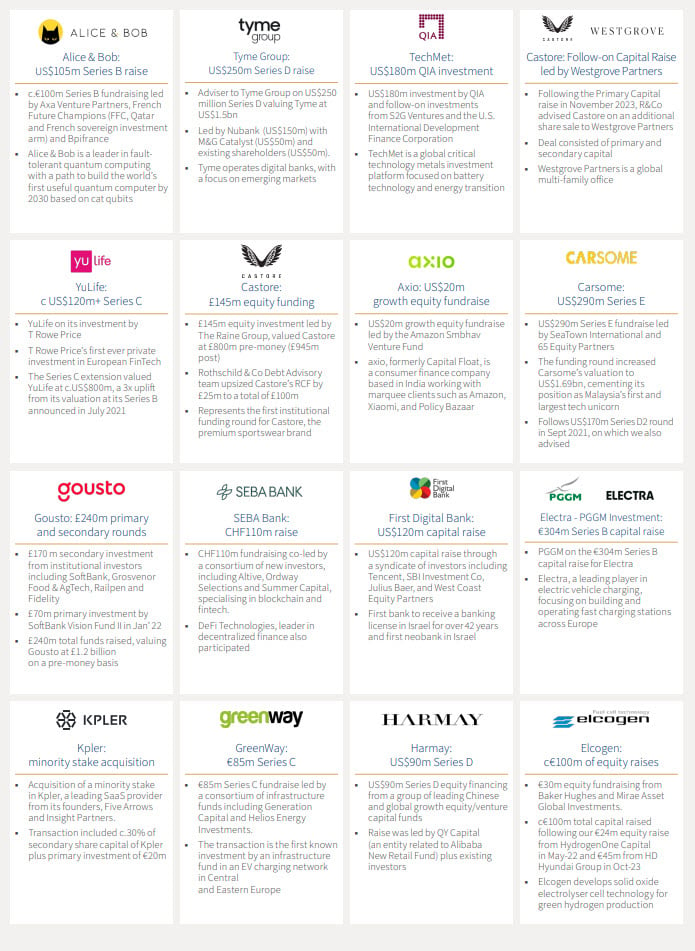

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised: