Are oil prices pushing inflation higher?

Oil has been steadily trending higher this year – up nearly a fifth in 2024. It recently breached $90 a barrel (Brent), a five-month high, and is supposedly one of the factors behind US inflation’s stickiness.

It goes without saying that oil prices are volatile. Demand is driven not just by users, but by speculators too, while supply is affected by geopolitical tensions (and by OPEC’s various attempts to curtail output).

Current strength reflects both sides of the market. User demand may be firming up. Global growth has beaten expectations, and the depressed manufacturing sector seems to be picking up, raising the demand for raw inputs, in particular oil. Indeed, the wider commodities complex has been moving higher – not only industrial metals, such as copper and nickel, but we’ve also seen big surges in cocoa and coffee prices. Precious metal prices have also risen, led by gold, though this may be related to investment demand rather than their industrial applications.

Nobody can predict what happens next of course, but absent a big negative supply shock, a more dramatic move in oil and other commodity prices seems unlikely. So far, this modest upturn remains well within recent trading ranges, with most spot prices still down sharply from their 2022 highs.

Spot commodity baskets indexed

100 = Jan 2020, in USD

Source: Rothschild & Co, Bloomberg Past performance is not a reliable indicator of future performance. Correct to 5 April 2024.

As far as inflation is concerned, energy is the most important commodity. Oil, after all, is still the single largest component of global trade, a vital input and the principal fuel for transportation. That said, it would take a very big spike in the oil price to have a meaningful impact on headline inflation (let alone core prices).

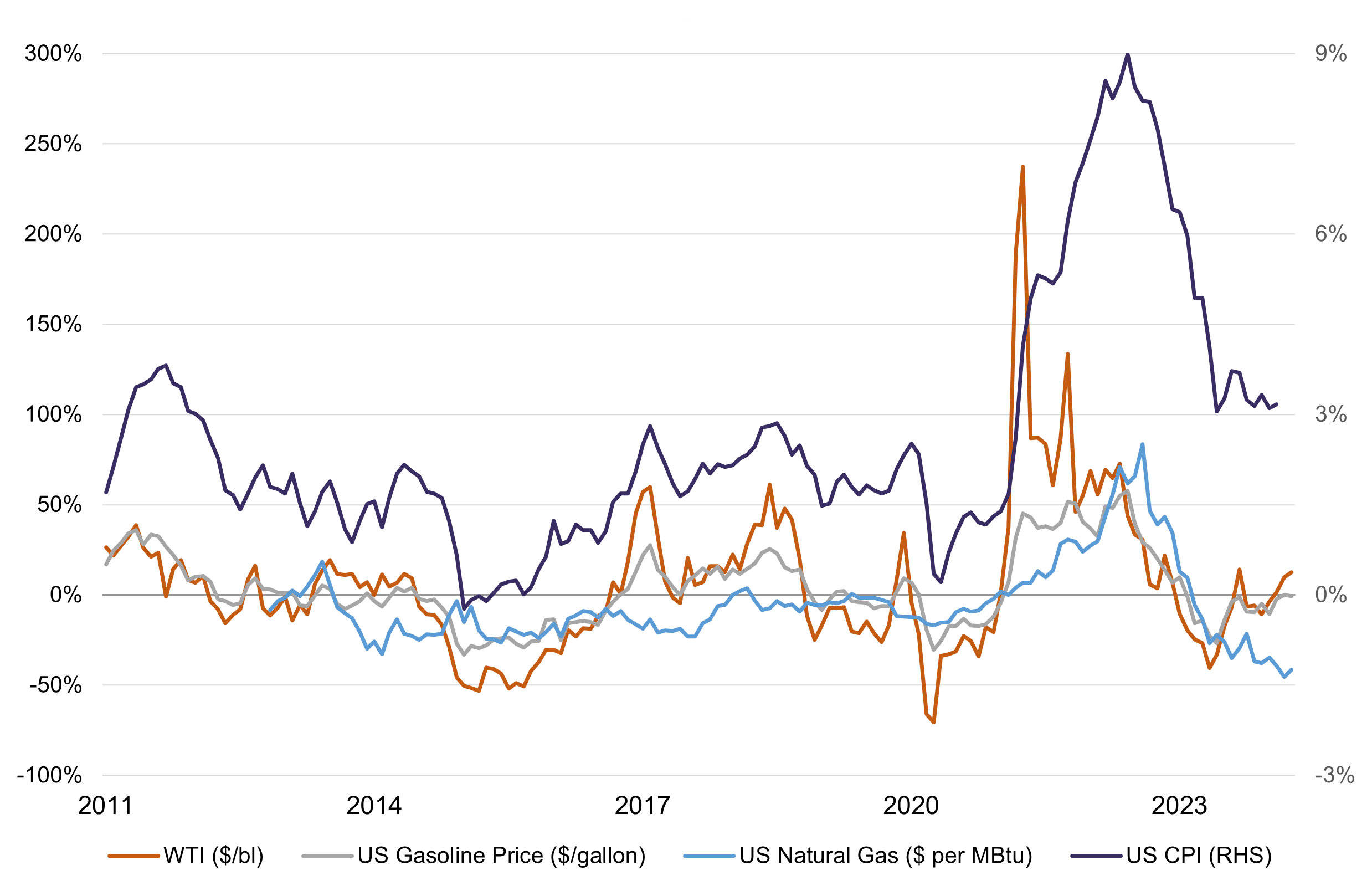

The direct energy components of the CPI account for nearly a tenth of the US basket (similar in the eurozone and UK). But even at their (nominal) peak in March 2022, when oil prices touched $128/barrel, the 72% year-on-year increase only corresponded (somewhat belatedly) to a third of the increase to the US CPI – contributing three percentage points to the peak US inflation reading of 9.1% in June 2022. Less than a year later, energy prices had reversed and were firmly deflationary.

Of course, energy is not just about oil – recent volatility in natural gas and refined fuels has been more important in Europe, for example. And the recent spurt in oil prices needs to be placed in context. For example, US gasoline prices – the main energy-related concern for US consumers – are only up a tenth in 2024, and at $3.63/gallon are still one third below their 2022 peak. US natural gas prices – which never moved as dramatically as their European counterparts in the early stages of the Ukraine war – are currently flirting with three-decade lows.

Selected US energy inputs and headline US CPI

Year-on-year changes, %

Source: Rothschild & Co, Bloomberg Past performance is not a reliable indicator of future performance. Correct to 5 April 2024.

Despite the rise in crude prices, then, inflation seems unlikely to surge anew. As a result, bond markets have so far been relatively unconcerned on this account – longer dated breakeven inflation rates have been edging higher but remain well anchored in the 2-2.5% range. And we doubt that this is the reason why shorter-dated interest rate expectations have been rising: central banks usually see oil-related economic effects as transitory and tend to focus on underlying rates of inflation mostly. Instead, resilient growth – and unambiguously strong labour markets – is what is most likely staying their hands on rate cuts. Strong demand, not oil prices, is what is mostly driving the ‘higher for longer’ interest rate narrative.

One silver lining to higher oil prices is what it might mean for corporate earnings. In the big stock market indices, there are more producers of oil than users of it, and we will start to see improvements in producers’ earnings and cashflows. Admittedly some of this is likely already in the price – energy (and commodity producing) sectors have outperformed in the past month or so (which partly explains why the ‘value’ stock cohort have been retracing some of their lost ground).

Ready to begin your journey with us?

Speak to a Client Adviser in the UK or Switzerland

Past performance is not a guide to future performance and nothing in this article constitutes advice. Although the information and data herein are obtained from sources believed to be reliable, no representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by Rothschild & Co Wealth Management UK Limited as to or in relation to the fairness, accuracy or completeness of this document or the information forming the basis of this document or for any reliance placed on this document by any person whatsoever. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, targets, estimates or forecasts contained in this document. Furthermore, all opinions and data used in this document are subject to change without prior notice.

Read more articles

-

Rothschild & Co impulsa su crecimiento en España con la incorporación de Álvaro Santos en el área de Wealth Management

Press releases

El nuevo nombramiento refuerza las capacidades locales y supone un paso más en la expansión del negocio de banca privada en España.

-

Geopolitics Blog: Christmas Season: Reasons to be cheerful

Insights

In our latest geopolitical blog, Mark Sedwill, Chair of Geopolitical Advisory at Rothschild & Co offers his reflections on six strategic reasons for Christmas confidence.

-

Five key questions for a carefree retirement

Corporate

Planning for retirement early helps secure your finances and gives you the freedom to enjoy travel, hobbies or family time. These key questions can guide you

-

Growth Equity Update

Insights

This is the latest Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory. 52% of the $63.4bn raised by the US growth equity market in Q4, up 31% yoy, was for AI companies. Datacentres, defence and crypto made strong showings. In this edition we look at the rise of the prediction marketplaces, Polymarket and Kalshi. Polymarket’s $2bn November raise at an $8bn valuation was up from $1.2bn in January. Kalshi’s valuation was $2bn in June and $11bn in November. We predict what’s ahead for them in 2026.

-

Global Advisory: Rothschild & Co Redburn Review - December 2025

Insights

Rothschild & Co Redburn have shared their final review of 2025, where they discuss all these questions, and more.

-

Building international leaders in the mid-market

Private Assets