Growth Equity Update

August 2025 – Edition 41

- A deep dive into Defence: We review the increasing commitment to defence spending in Europe and the US, the changing nature of defence spending and the new opportunities it presents for private capital.

- End of the peace dividend. The Stockholm International Peace Research Institute reports 2024 saw the steepest y-o-y rise in world military expenditure since 1988, up 9.4% to $2,718bn, with its share of world GDP up to 2.5%.

- A new type of defence spending. The experience of the Ukraine war has shifted the focus of incremental defence spending from traditional military platforms (tanks, warships, planes) to new technologies like AI, robotics, autonomous solutions, quantum computing and cybersecurity.

- And new companies to do it: As the UK Ministry of Defence recently pointed out Today, much of the best innovation is found in the private sector [and] increasing prevalence of dual-use technologies [means] there is a deep range of partners. to bring in alongside prime contractors, from technology and innovation startups and scale-ups to small and medium-sized enterprises [and] private investors.

- YTD global VC investment in defense businesses is up 2.5x yoy at $28.4bn, according to Pitchbook, after 17% growth in 2024.

- We look at the VC investors in defence, some of the emerging companies in this field and this year’s biggest venture capital raises in defence.

- OpenAI reopens its $40bn round. We look at the dynamics and at the $116bn raised in growth equity for AI LLM businesses alone since the start of 2023.

- July VC raises maintain the momentum: July saw 42 US venture capital raises of $100m or above, raising $13.1bn up 2.2x yoy. Europe’s $4.2bn was up 15% yoy.

Click here to download a PDF version of Growth Equity Update

Coming off Defence

In defence sourcing ‘business as usual is no longer an option’ UK Strategic Defence Review 2025

The Russian invasion of Ukraine at the start of 2022 pitched Russia into open warfare in Europe for the first time since 1945 and has heightened geopolitical tensions around the world. In turn these have been exacerbated by the conflict in Gaza and fears of Chinese aggression against Taiwan.

Since the start of 2025, the new Trump administration has made it clear that its support for Ukraine is not unambiguous and that it expects Europe to shoulder the burden of its own defence rather than to rely on the US to pick up the tab for European security.

Responding to US Vice President JD Vance’s speech at the Munich Conference in February this year, in which he affirmed the US’s commitment to European security while emphasising the need for Europe to increase spending on its defence, Boris Pistorius, the German defence minister responded.

‘Last year, Germany committed two percent of its GDP to defence. Within just two years, we nearly doubled our investments in procurement, other European nations have made similar successful efforts. Security guarantees the future for all of us and for the next generation. We have the responsibility to invest in the future for Germany. That means further increasing our defence spending. We need substantial financial means that cannot simply be cut out of the current budget. Excluding defence spending from our national debt limit is, therefore, inevitable. Security is not a short-term expenditure; it is a long-term commitment. That is why I am developing a ten-year program. We need to make defence spending more predictable. That means achieving next-generation security at the European level.’

The new US approach has accelerated a trend in increased defence spending already apparent since the outbreak of the Ukraine conflict.

The Stockholm International Peace Research Institute notes that world military expenditure rose 9.4% to $2,718bn in 2024, the steepest year-on-year rise since 1988. The share of the world’s GDP devoted to military expenditure increased to 2.5%.

In 2024 military expenditure by the 32 NATO members was $1,506 billion, 55% of the total. European NATO members spent $454bn or 30% of total NATO spending, up 8.9% yoy and up 16% on 2023, ranging from +0.4% for Spain to +43% for Romania.

In 2014 all NATO members committed to spending 2% of GDP on the military by 2024. In 2023 this guideline was revised to ‘at least’ 2.0% of GDP. In 2024 they spent 2.2%. Of the 32 NATO members, 18 spent at least 2% cent on their militaries in 2024, up from 11 in 2023, the highest number since the guideline was introduced.

At its 2025 Summit in The Hague, the NATO countries made a commitment to investing 5% of GDP annually on defence and security related spending by 2035 with at least 3.5% of GDP to resource core defence requirements and 1.5% of GDP annually to protect critical infrastructure, defend networks, ensure civil preparedness, innovate, and strengthen the defence industrial base. This should mean at least an additional €350bn of defence spending on the existing base of c€400bn.

Looking at spending trends in some of the key countries:

Germany’s military spending rose in 2024 by 28% as it continued to implement an extra-budgetary fund of €100bn created in 2022 to boost the military budget.

The UK has pledged to spend 2.5% of GDP on the military by 2027—a change from the initial target of 2030—and has a long-term goal of raising this to 3.0%.

French military expenditure rose 6.1% in 2024, reaching $64.7bn, equivalent to 2.1% of GDP. The increase aligned with the 2024–30 Law on Military Planning that aims to strengthen France’s strategic autonomy and adapt its arms industry to a ‘war economy’ sustained by industrial innovation.

Poland’s military spending rose 31% in 2024, to $38.0bn with the 4.2% of GDP that this represents, being the highest level in Western Europe and above the 2023 government target of 4.0%.

Sweden joined NATO in 2024 and increased its military expenditure 34% in 2024, to $12.0bn immediately reaching 2.0% of GDP.

Ukraine’s military expenditure grew by 2.9% to $64.7bn, 54% of total Ukrainian government spending in 2024.

The USA’s military spending rose 5.7% to $997bn, 66 % of total NATO and 37% of world military spending in 2024.

World military expenditure, by region, 1988–2024 – 9.4% increase in 2024

Source: SIPRI Military Expenditure Database, Apr. 2025

Source: SIPRI Military Expenditure Database, Apr. 2025

In June 2025, the EU issued Readiness 2030 – a white paper for European defence known as the ReArm Europe Plan. It targets €800bn as the amount Member States aim to mobilise to finance what it calls ‘a massive ramp-up of defence spending’ while giving EU countries more financial flexibility.

It aims to achieve this by:

Activating the national escape clause of the Stability and Growth Pact, allowing Member States to increase defence spending. A 1.5% GDP increase in defence budgets could create nearly €650bn in fiscal space over four years.

Launching a €150bn loan instrument - Security Action for Europe (SAFE) - that will help countries invest in key defence areas like missile defence, drones, and cyber security. The funds will be raised on capital markets.

Supporting the European Investment Bank Group in widening the scope of its lending to defence and security projects and accelerating the Savings and Investment Union to mobilise private capital so that the European defence industry is not reliant on public investment alone.

As well as the quantum of defence spending the way in which the money allocated is being spent is also changing. Here is an extract from the UK’s ‘Strategic Defence Review 2025 - Making Britain Safer’. It highlights how the experience of the Ukraine war has shifted the focus of incremental defence spending from traditional military platforms (tanks, warships, planes) to new technologies such as AI, robotics, autonomous solutions, quantum computing and cybersecurity.

Technologies that are redefining warfare

Source: UK Strategic Defence Review 2025 - Making Britain Safer’ – July 2025

Source: UK Strategic Defence Review 2025 - Making Britain Safer’ – July 2025

It observes.

Autonomous and uncrewed (land and aerial) systems are now an essential component of land warfare, …. A ‘20-40-40’ mix is likely to be necessary: 20% crewed platforms to control 40% ‘reusable’ platforms (such as drones that survive repeated missions), and 40% ‘consumables’ such as rockets, shells, missiles, and ‘one-way effector’ drones. Investment in attack and surveillance drones should be prioritised, along with counter-drone systems.

The report highlights that in defence sourcing ‘business as usual is no longer an option’ and emphasises a role for technology and innovation startups and scale-ups.

Today, much of the best innovation is found in the private sector, while the increasing prevalence of dual-use technologies has widened the net of potential suppliers that can contribute to Defence outcomes. There is a deep range of partners outside Defence that it must work to bring in alongside prime contractors, from technology and innovation startups and scale-ups to small and medium-sized enterprises, private investors, and the trade unions.

The increase in the quantum of defence spending and the shift in the nature of the spend, on the one hand to intelligent systems and on the other to lower cost, but highly effective tools like drones, presents a substantial opportunity for venture companies and their backers.

Pitchbook figures show that global defence related VC funding reached $50.9bn as the growth equity market peaked in 2021. Along with the market it fell back sharply to $34.1bn in 2022.

Global defence related VC funding grew 17% in 2024 and was up 2.5x yoy in H1 2025 at $28.4bn putting it on track to exceed the 2021 levels. The $19.1bn committed in Q2 2025 grew just over 3x yoy.

Global Defence tech VC deal activity

Source: Pitchbook- Geography Global – As of 30 June 2025

Source: Pitchbook- Geography Global – As of 30 June 2025

Defence Tech VC deal activity by quarter

Source: Pitchbook- Geography Global – As of 30 June 2025

Source: Pitchbook- Geography Global – As of 30 June 2025

The next chart gives a sense of where this money is being directed.

Defence Tech VC deal activity by segment – Software, drones, connectivity and Space

Source: Pitchbook- Geography Global – As of 30 June 2025

Source: Pitchbook- Geography Global – As of 30 June 2025

Advanced computing and software are the leading category followed by Autonomous systems with sharp growth in each of unmanned aerial vehicles (UAV), unmanned ground vehicles (UGVs) and most recently unmanned surface vessels (USVs) as well as in counter drone technologies. The growth in spend in sensing, connectivity & security demonstrates investor focus on foundation technologies behind modern defence capabilities.

With the shift in state backed priorities has come a shift in VC and growth equity investor attitudes towards defence investment.

Until recently VC funds might look to avoid defence related investments on both ethical and commercial grounds. On ESG, as well as potentially having their own concerns, funds had to be wary of restrictions by LPs and other investors on investment into defence related businesses. The new environment is leading to a shift in attitudes. The UK’s FCA, for instance, declared in March 2025 that the financial sector plays a vital role in supporting all sectors, including defence.

There is nothing in our rules, including those related to sustainability, which prevents investment or finance for defence companies. There is a move to rebadge ESG as ESSG with security the additional embodiment in the formula. These figures from Morningstar indicate that 35% of Europe’s ESG funds held defence stocks in Q1 2025, up from 25% four years earlier. Many funds look for ‘dual use’ technologies – applications with both a civil and defence capability – aerial drones typically fall neatly into this category.

European ESG funds – 35% own defence stock

Source: Morningstar Direct, Morningstar Sustainalytics

Source: Morningstar Direct, Morningstar Sustainalytics

Commercially VC funds may have eschewed defence as it was seen as a difficult sector in which to invest – suffering from the ‘peace dividend’, capex and hardware heavy, with government and institutional buyers with slow decision cycles, with heavy scrutiny of margins by the buyers of product and operating in a market dominated by big platform defence contractors.

Many of these factors are now being swept away as governments race to adopt the private sector and new technology businesses as key components of the new defence procurement environment.

Indeed, we are seeing the emergence of funds specifically oriented to defence investment. Thus, in May the European Investment Fund announced a €40m investment in the Keen Venture Partners’ European defence and security Tech fund under the Defence Equity Facility and the InvestEU Space mandate.

The Keen Ventures fund has a focus on early-stage companies within the defence and security sectors and aims to invest in information superiority, cyber defence, robotics, AI, autonomous systems and space technologies such as securing satellite communications, satellite image analysis, and defence of space assets.

Alexander Ribbink, at Keen Venture Partners commented the opportunity to add the power of tech entrepreneurs with the full support of venture capital to the European defence ecosystem is huge.

A new Estonian VC firm, Darkstar, is currently raising €25m with the intention of investing in purely military applications.

Amongst the most prominent funds investing in defence application is the NATO Innovation Fund. Described as ‘the world's first multi-sovereign venture capital fund,’ at €1bn it was the biggest venture capital fund to be launched in Europe in 2023.

Its stated purpose is to invest in start-ups developing cutting-edge technological solutions, leveraging the potential for commercial innovation to address critical defence and security challenges.

The Fund will invest €1bn in early-stage start-ups and venture capital funds that are working on dual use emerging and disruptive technologies of priority to NATO. The nine priority verticals identified by the NIF are artificial intelligence; autonomy; quantum; biotechnologies and human enhancement; hypersonic systems; space; novel materials and manufacturing; energy and propulsion and next-generation communications networks.

The Fund’s Limited Partners include 24 European NATO allies at the highest levels of government, venture capital, innovation, and defence. The NIF does not, as yet, include the United States although it has not ruled out joining at some stage. (The US already has a similar body, In-Q-Tel based in Arlington, Virginia which supports the CIA and other US intelligence agencies)

The NIF will make direct investments into start-ups located in any of the participating Allied nations and can also make indirect investments into deep tech funds with a trans-Atlantic impact. The style of the fund is that “It will provide patient capital to meet the needs and timelines of deep tech innovators and to secure an enduring future for the Alliance’s 1 billion citizens.”

The chair of the NATO Innovation Fund is Klaus Hommels, the founder and chair of Lakestar who has commented:

“As the importance of technology in all parts of our lives increases so does the need for digital and technology sovereignty. The NIF is the first multi-sovereign venture capital fund that will support emerging technologies and drive much needed innovation in areas touching the Alliance's objectives.”

The NIF will lead early-stage investments with initial cheque sizes of up to €15m. The intention is that the NATO network of c90 NATO-affiliated test centres and more than 6,000 Allied scientists will be available ‘to pressure-test solutions.’ There is an existing initiative within NATO, the existing Defence Initiative Accelerator for the North Atlantic (DIANA). The intention is that the NIF and DIANA will cooperate closely. DIANA has a network of 10 affiliated accelerator sites to support its accelerator programme.

Other prominent European defence investors include:

Project A is a Berlin based firm with AUM of €1.2bn which recently raised its fifth fund at €325m. Albeit a generalist investor, one of its key themes is ‘European Resilience -backing founders building companies for tomorrow’s European military’ – both dual-use and military equipment. It is an investor in two UAV businesses Quantum Systems and ARX Robotics as well as Vaeridion, an electric aircraft for short haul mobility. https://www.project-a.vc/approach/european-resilience

SmartCap based in Estonia (proximity to the Russian border clearly focuses the mind) has a €100m fund dedicated to strengthening Estonia’s defence industry by supporting the development of innovative technologies and backing high-potential defence producers that contribute to national security. It invests both through private funds and via direct investments into defence companies. It will not invest in VC firms that have restrictions on investing in weapons technology. It has invested €10m in Estonia’s Darkstar fund.

In Poland, the Expeditions Fund is ‘Investing in the Future of Security’ with a focus on cyber-security, defence/intelligence, autonomy, AI, quantum, privacy, communication solutions and space. It writes tickets up to €5m.

PrimaMateria the VC fund which is run by Spotify founder Daniel Ek is the largest shareholder in German defence AI business Helsing with a 16% stake. Helsing uses AI to develop applications for defence, focusing on all-domain defence innovation (air, land, sea, space, and cyber). June 2025’s $690m raise for Helsing led by Prima Materia was supported by Lightspeed and Accel and valued the business at $13.2bn. Helsing’s previous Series C raise in 2024 was for €450m.

PrimaMateria has backed multiple Helsing rounds. It observes Helsing was set up to build AI to serve our democracies and play a part in protecting them from harm. We share Helsing’s conviction that liberal democratic values are worth defending and that artificial intelligence will be an essential capability to keep us safe. https://primamateria.com/

Lakestar led by Klaus Hommels, an early investor in Helsing and Chair of the NATO Innovation Fund, is seeking $250m-$300m for a new defence fund. The fund will target companies operating in secure communications, autonomous systems, quantum sensing, and next-generation materials.

LuxCapital is raising a $200m fund Lux Defence Leaders, focused on defence tech. The firm was an early investor in US defence business, Anduril.

Mainstream funds are providing much of the firepower in defence company raises. The next Exhibit outlines the biggest raises in defence and related application in the first seven months of 2025 and identifies their lead investors.

We identify (in our tracked universe of US raises over $100m and European raises of $20m+) investment of $6.3bn on defence related businesses ytd.

US and Europe – c$6.3bn on Defence related raises in the first seven months of 2025

Source: Rothschild & Co Deal Monitor

Source: Rothschild & Co Deal Monitor

Amongst the backers of the biggest defence raises thus far this year are:

Peter Thiel’s Founders Fund led the Anduril $2.5bn raise with a $1bn contribution, the largest single investment made by the fund. Trae Stephens is the partner who oversees defence investments at the Founders Fund and is chair of Anduril. He observes in his essay ‘The Ethics of Defence Technology investment: An Investor’s Perspective’:

In debating the value of our investment in defence technologies, we cannot ignore the fact that if we allow others to build these technologies while we stand idle, we will lose the power to regulate their use, we will allow aggressive autocratic regimes to take the lead, we will voluntarily limit our power to deter harmful conduct (including genocide, repression, and interference with international norms), and we will cede to the most belligerent and authoritarian states the power to impose insidious legal and moral standards on the US and its allies without consequence.

Anduril offers a range of autonomous defence systems, and the AI based software that controls them. Its systems are powered by Lattice, an AI-based operating system that connects autonomous sensemaking and command & control capabilities with modular and scalable hardware components. Products include the Barracuda family of military drones, the Roadrunner reusable vertical take-off and landing (VTOL) Autonomous Air Vehicle (AAV) and the Dive-LD autonomous underwater vehicle.

The company raised $2.5bn in a Series G in June 2025 which valued it at $30.5bn, twice the valuation of its previous round. Revenues in 2024 doubled to $1bn. In February Anduril was granted the U.S. Army’s contract – with a headline value of $22bn - for developing new AR/VR headsets.

Founders Fund also led July’s $260m Series C by the defence machine parts company Hadrian, a raise supported by Lux Capital, Andreessen Horowitz, and Altimeter Capital.

Altimeter and Lightspeed were also backers of July’s $350m raise by Castelion which ‘designs, tests, and manufactures next-generation military systems rapidly and at massive scale to deter future wars’ and offers ‘affordable hypersonic weapons, built fast.’ It previously raised a $100m Series A that closed in January. Altimeter also led a $110m Series B for K2 Space in January. K2 Space has designed a high-power, high-payload mass satellite platform. Its solution aims to address the increasing demand for proliferated space applications, a dual use application that has attracted interest from commercial and national security customers.

Blackrock was the lead investor in the $300m round raised by dual use business Archer Aviation in February 2025. Archer was originally a developer of vertical take-off and landing VTOL aircraft for commercial use. In December 2024 it launched a defence division in with plans for a hybrid-propulsion VTOL aircraft aimed at military applications. Archer has a collaboration with Anduril to develop a hybrid gas-and-electric VTOL aircraft under the Archer Defence program which aims to secure DoD funding. Adam Goldstein, the founder and CEO of Archer, said “I believe the opportunity for advanced vertical lift aircraft across defence appears to be substantially larger than I originally expected. As a result, we are raising additional capital to help us invest in critical capabilities like composites and batteries to help enable us to capture this opportunity and more.”

Accel was one of the backers of the Helsing $600m raise in June. It also led the May 2025 $275m Series C for Chaos Industries alongside New Enterprise Associates. Chaos develops communications, radar and sensor technologies for military use with its core radar system Vanquish used for early warning and tracking drones, missiles, and aircraft.

General Catalyst, Elad Gil, a16z and 8VC were key backers of the $600m raise by Saronic Technologies in February which valued the business at $4bn, second only to Anduril in US defence start-ups. Saronic describes its mission as ‘redefining maritime superiority for the United States and its allies.’ Saronic develops autonomous surface vessels and will use the funds to build a new shipyard, Port Alpha, allowing it to expand its medium and large-class autonomous vessels- effectively water-borne drones.

General Catalyst MD Paul Kwan commented that ‘our mission is to help modernize our nation's defence and industrial resilience.’

8VC, alongside Washington Partners was also a key backer in the $250m Series D for Epirus, the counter electronics business in July. Epirus’s Leonidas system is high-power microwave technology tested by the DoD as effective in countering drones, drone swarms, and other electronics. At the announcement of its new $998m fund in July 8VC highlighted defence, where frontiers range from the electromagnetic spectrum to next-gen materials, to advanced maritime and ground autonomy as one of six key areas of focus.

A substantial amount of the money being raised in defence VC is for autonomous vehicles and drones. Saronic has seen the biggest raise in this field in 2025. There have been multiple other examples:

ShieldAI is a developer of software for autonomous aircraft and drones. It raised a $240m Series F in March at a valuation of $5.3bn with strategic investors L3Harris and Hanwha Aerospace and VC investors including Andreessen Horowitz, U.S. Innovative Technology, and Washington Harbour.

The company’s Hivemind proprietary AI software allows drones to operate autonomously. Its V-BAT vertical take-off and landing drone delivers, according to the company, combat-proven, expeditionary, strategic and tactical-level ISR (intelligence, surveillance, and reconnaissance) and targeting at a fraction of both the cost and logistical footprint of larger drones. V-BATs have been used in Ukraine and Shield cites contracts worth $100m plus for European government customers and a potential $200m five-year V-BAT contract with the U.S. Coast Guard

Notable drone raises in Europe a €160m raise by Munich based Quantum Systems in May this year led by Balderton Capital, with participation from Hensoldt, Airbus, and Bullhound Capital. Quantum produces AI-powered aerial intelligence systems for defence, emergency services, and industry. Its drones are currently used by NATO-aligned forces – including those in Germany, Ukraine, Australia, New Zealand, and Spain. Commercial applications of Quantum Systems’ solutions include mapping drones across mining, agriculture, and infrastructure with clients including RocketDNA and the Indian government’s Department for Science and Technology.

Also, in May Lisbon based Tekever raised €70m in a round valuing the company at above €1bn led by Ventura Capital, the NATO Innovation Fund and Baillie Gifford.

Tekever’s autonomous drone systems have been used for over 10,000 combat flight hours with the Ukrainian armed forces. It handles all aspects of its drone technology from airframe design and manufacturing to payloads, avionics, software, data, and AI. The company’s customers include the UK MoD, the Brazilian Navy and Colombia’s armed forces. Alongside the raise in May Tekever announced a plan to invest £400m in “research, infrastructure, and defence technology development in the UK”, in its Overmatch programme, on the back of its AR3 tactical UAV being commissioned as part of the RAF’s new StormShroud autonomous collaborative platform. Tekever has acquired a small airport in Aberporth, West Wales to facilitate its operations.

Germany’s ARX Robotics which raised €42m for its autonomous unmanned ground vehicles (UGVs) in a May round led by HV Capital and including Omnes Capital, the NATO Innovation Fund and Project A.

The UK’s Orca AI operates in the autonomous navigation market. The system was originally designed for the commercial market to navigate ships more fuel efficiently by using AI aligned to LEO satellite systems like Starlink. More recently the company has extended into defence applications. Its $73m raise in May was led by Brighton Park Capital, Ankona Capital and Hyperlink Ventures.

Israeli cargo drone company AIR raised $23m in July for its uncrewed cargo eVTOL aircraft. AIR’s uncrewed cargo eVTOL is designed to meet the growing demand for adaptable air transportation in industries such as cargo delivery, disaster response, contested logistics and remote access operations. AIR is involved in the U.S. Air Force’s Agility Prime programme.

Space and communications are a core aspect of modern defence capabilities. With the recent shift in relations between the US and European countries in the context of defence, European space sovereignty is becoming a big issue. Alternatives such as the European controlled OneWeb to the US controlled Starlink for satellite communications and defence applications are being sought.

The next exhibit looks at recent Space related raises, many of which have defence applications as part of their make-up. The Bulgarian company Endurosat builds modular, software-defined satellites for a wide range of commercial and government applications. It raised $49m in May led by Founders Fund. It is a typical dual use company with 350 customers including a number for defence applications. It contributes to the European Defence Fund’s REACTS project (Responsive European Architecture for Space), which aims to create a new space-based defence capability.

The NATO Innovation Fund is an investor in Germany’s Isar Aerospace whose military customers make up c20%-30% of the demand for its space rockets.

France’s Loft Orbital, a space infrastructure business, has a partnership with Helsing to develop a multi-sensor satellite constellation able to deliver real-time intelligence and situational awareness to European defence forces. The system is designed for critical missions such as border surveillance, troop movement tracking, and infrastructure protection.

The three largest US space raises in 2025 are all examples of dual use businesses with defence applications.

Impulse Space is a space tug business which is able to move satellites around in space. It observed when raising $300m in June in a round led by Linse Capital that Commercial operators need faster, more cost-effective ways to deploy and reposition satellites. Defence agencies require tactically responsive capabilities to stay ahead of evolving threats. It has a collaboration with Anduril to supply its Mira orbital transfer vehicle to support classified mission requirements.

The United States Space Force has selected Stoke Space to participate in its National Security Space Launch (NSSL) Phase 3 Lane 1 program, designed to expand its capacity to deliver critical space launch capabilities. The award enables Stoke to compete for a total of $5.6bn in national security launch contracts using its 100% reusable Nova rocket. Its $260m Series C in January was supported by investors including Breakthrough Energy Ventures, Glade Brook Capital Partners, Industrious Ventures, Leitmotif and Point72.

True Anomaly raised $260m in April led by Accel. The company says ‘True Anomaly was founded to develop and deploy defence products that meet the needs of a modern, contested space environment…. Our mission is to design and build autonomous systems to deter conflict and protect space for humanity, and we are fielding space defence products at the forefront of modern military tactics – terrestrial or otherwise.’

VC raises – Space and Defence applications – First 7 months of 2025

Source: Rothschild & Co Deal Monitor

Source: Rothschild & Co Deal Monitor

The message is that defence spending is growing sharply and new technologies and methods of conducting warfare are offering an opportunity to young, VC backed tech led companies to take a disproportionate share of this new spending from the traditional platform led defence contractors. VC investment in defence companies is accelerating and the trend appears likely to keep gathering pace as the world adapts to the new reality of heightened geopolitical tension and the realisation that regions, like Europe, will need to shoulder more of the burden and cost of their own defence rather than relying on the U.

Open AI $40bn round reopens

Since the November 2022 launch of Chat GPT, c$116bn has been raised for the leading AI large language model businesses.

At the end of March ChatGPT developer OpenAI announced that it had closed a $40bn round valuing the company at $300bn. It was the largest ever private fundraising round. The lead investor was SoftBank, which committed up to $30bn, with other backers including Microsoft, Coatue, Altimeter and Thrive.

OpenAI said it intended to use the new money to scale its compute infrastructure and “push the frontiers of AI research even further” as well as to support its role in the US Stargate AI investment programme.

The round is currently being fleshed out. SoftBank is committed to providing 75% of the total funding, or $30bn. Back in March, an initial $10bn was committed, Softbank contributing $7.5bn with $2.5bn coming in from other investors.

In the current phase, SoftBank has committed a further $22.5bn with $7.5bn being sought from other investors. Press supports suggest the strength of demand means the $7.5bn target has been exceeded with $8.3bn being raised, including a $2.8bn commitment from Dragoneer, the Californian tech focused fund as well as commitments from Blackstone, TPG, FMR and T Rowe Price.

Linked to the fundraise are two structural issues at OpenAI. The first is the planned restructuring of OpenAI into a for profit entity.

In December 2024 Open AI launched proposals to ‘1. Choose a non-profit / for-profit structure that is best for the long-term success of the mission; 2. Make the non-profit sustainable. 3 Equip each arm to do its part.’

At the time it said that

‘We have a non-profit and a for-profit today, and we will continue to have both, with the for-profit’s success enabling the non-profit to be well funded, better sustained, and in a stronger position for the mission.’

The core part of the plan was to move the existing for-profit into a ‘Public Benefit Corporation’ with ordinary shares of stock and the OpenAI mission as its public benefit interest. The PBC would require the company to balance shareholder interests, stakeholder interests, and a public benefit interest in its decision making, enabling OpenAI to raise capital with conventional terms.

After opposition to the plan to reduce the control of the non-profit these proposals were amended in May 2025 with Open AI having heard ‘from civic leaders and engaging in constructive dialogue with the offices of the Attorney General of Delaware and the Attorney General of California.’ The proposals had also received objections from Elon Musk and Meta.

OpenAI announced that it would abandon plans to remove the nonprofit entity’s controlling status. Instead, the for-profit entity would still become a PBC but would remain under control of the nonprofit.

It is believed to be a requirement of the Softbank portion of the $40bn fundraise that the shift from non-profit status should be completed by the end of calendar 2025. Without this happening the Softbank portion of the funding could fall to $10bn. Open AI’s CEO Sam Altman has said that SoftBank remains committed to its full investment under the revised restructuring proposed in May.

Microsoft also has a substantial ownership position in OpenAI. The two companies have a contract running to 2030 which dictates the operating relationship between the two businesses encompassing revenue sharing agreements that flow both ways. Microsoft has exclusive rights to sell access to OpenAI’s models. It is entitled to a 20% share of Open AI revenues up to $92bn.

Microsoft has rights to OpenAI IP (including model and infrastructure) for use within products like Copilot. The OpenAI API is exclusive to Azure, runs on Azure and is also available through the Azure OpenAI Service.

These arrangements are currently being renegotiated. At stake is the issue of ‘artificial general intelligence’ (AGI) or human-like intelligence. This is the point the AI model has the ability to self-teach. At present it is understood that Open AI has the ability to end Microsoft’s access to new models at the point at which the AI board declares that the company has reached AGI capability. The current negotiations, designed to extend the relationship beyond 2030 will encompass this. It is believed Microsoft will end up with a stake of c30% in Open AI.

Growth Equity investor appetite for LLM and foundation models AI raises remains substantial. The next table rounds up the investment total for LLM and related businesses since the start of 2023. It indicates that around $116bn has been raised for such companies since the start of 2023, the wave of investment having been sparked by the November 2022 launch of Chat GPT.

In that time Open AI has raised $56.6bn. A flurry of funding in the last 15 months has raised $19bn for xAI. Anthropic has received c$11bn of investment from a combination of Amazon and Google plus c$3.7bn from other investors. Scale AI is a data annotation company which enables models to build AI applications. It has raised $15.3bn across two rounds since May 2024, most of the funding coming from Meta.

There is a fall way in the scale of funding after that to the $5bn raised by the two ‘talent ‘AI raises, the $3bn raised for Safe Superintelligence and the $2bn for Thinking Machines Labs. Both of these companies were founded by former Open AI executives and are both pre-products.

The leading European LLM business in fundraising terms is France’s Mistral which has raised $1.2bn across three rounds starting with a $113m seed round in June 2023, just a few weeks after its launch.

Sandbox AQ which uses quantum computing techniques to develop quantitative artificial intelligence models for enterprises, has raised $950m over three rounds with the most recent round valuing it at $5.75bn.

Perplexity, a GenAI search engine has raised $450m in four rounds since the start of 2023. Its imputed valuation rose from $2.5bn in its $250m round led by NEA and IVP in April 2024, to $18bn in its $100m round led by Nvidia and SoftBank in July 2025.

Elsewhere Hippocratic AI which develops LLMs for healthcare raised $141m in January 2025. Runway which has developed a range of generative AI models for media production raised $308m in April 2025.

In Europe, the issue of data sovereignty has emerged since the second Trump administration began. German business Aleph Alpha announced a $500m raise in November 2023 to develop data sovereign LLMs. It emerged subsequently that just $110m of this was in equity with the rest in the form of research grants. The company has subsequently shifted its focus to developing a ‘generative AI operating system’ to sell to B2B customers, helping enterprises to roll out AI disciplines within their businesses.

French business H raised a $220m seed round in May 2024 to develop ‘frontier action models to boost the productivity of workers.’ Three of the company’s five co-founders departed three months later. The CEI Charles Kantor then left in June 2025 and was replaced by a former Palantir executive.

The appetite for LLM investment remains strong. As well as the reopening of the OpenAI round there are several more raises in the works. Not content with its four raises since May 2024, xAI is said to be seeking a further $10bn at a $200bn valuation with the Saudi PIF said to be the potential core investor.

Anthropic is also in the market for another raise - this time of c$5bn at a valuation of $170bn with ICONIQ said to be in position to lead. It was last valued at $62.5bn in its $3.5bn March 2025 raise.

French LLM business Mistral is said to be looking for a $1bn raise with Abu Dhabi’s AI fund MGX potentially the lead for a round which would value the business at c$10bn. This would virtually double the funding received by the business to date. Some press reports (Business Insider, Sifted) see an alternative outturn – the acquisition of Mistral by Apple for c$15bn – the logic being that Apple is the only major tech giant not to have yet invested in an LLM business. Apple might help with scale. OpenAI is said to be on track for $12bn in ARR in 2025, Anthropic for c$5bn and Mistral for c$100m.

AI LLM businesses - $116bn raised since the start of 2023

Source: Rothschild & Co

Source: Rothschild & Co

Markets – Europe to the fore

Lower US interest rate hopes come to the fore.

Once again, despite everything thrown at them. markets remained robust in July and reverted to their ‘normal’ hierarchy with NASDAQ leading the way up 4.5% in the month. The S&P500 and the STOXX 600 were up 1% and the FTSE 100 up 4%.

YTD to end August, in local currency terms, NASDAQ leads the way, up 12.5%, the FTSE 100 and the S&P 500 are up 11% and the STOXX600 is up 8%. Funds flows indicate that the brief swing towards European markets and away from the US that occurred in the aftermath of Liberation Day have now reversed – the flow of funds is once again predominantly towards the US.

The FTSE Venture Capital Index which measures the performance of the US venture capital industry, with a strong sector weighting towards technology, fell 2% in July and to mid-August is up 19% ytd.

What is driving the most recent bout of enthusiasm as we move through August is the prospect of falling interest rates in the US. This comes from a combination of factors.

- The weak employment data that persuaded the US President that the head of the US Bureau of Labor Statistics should be replaced, appears to have been received more readily by markets, which sees weak jobs numbers as a precursor to lower interest rates.

- The July inflation number of 2.7% was lower than expected chiefly due to lower prices for oil and gas. Most of the underlying indicators – notably the Fed’s preferred core inflation figure went the wrong way. The numbers also showed little discernible impact as yet from tariffs – one of the factors cited by the Fed as a reason for caution in further lowering interest rates.

- Political pressure on the Fed to cut rates, symbolised by the uneasy pictures of the President and the Fed Chair standing in white hard hats on a building site arguing over which projects had or had not been included in the estimated cost overruns of an HQ refurbishment.

The political pressure has been maintained with the appointment of Stephen Miran, the chair of the White House’s Council of Economic Advisers, to a vacant seat on the Fed. Miran is a supporter of the Trump administration’s tax cuts and has downplayed the risk of tariff cuts promoting inflation saying that he doesn’t have ‘tariff derangement syndrome.’ President Trump is also considering candidates to replace Fed Chair Jay Powell when his term ends in May 2026.

There are clear indications from the administration that it thinks interest rates should be significantly lower. In mid-August, the US Treasury Secretary Scott Bessent declared that interest rates should be 150-175 basis points lower than they currently are and recommended ‘we could go into a series of rate cuts here, starting with a 50-basis point rate cut in September.’ President Trump has said that ‘I think we should be paying one percent right now.’

This last remark was before the July 30th meeting at which the Fed kept interest rates steady at 4.25%-4.5% for the fifth meeting in a row. Unusually two of the twelve FOMC committee members voted against the decision, both backing a 25bps rate cut. The decision to hold rates came after figures showing that the US economy had grown at a robust 3% in Q2 2025 but before the disappointing July jobs number. Produced on August 1 it showed non-farm payrolls rising by just 73,000 versus market estimates of 100, 000. The May and June numbers were also sharply downgraded (June from 147,000 to 14,000 and May from 144,000 to 19,000 – jointly a downwards revision of 258,000). The unemployment rate ticked up to 4.2% from June’s 4.1%.

On August 12th, the July US inflation number came in 10bps lower than expected at 2.7%. Core inflation, which excludes energy and shelter costs, rose to 3.1% from June’s 2.9%. Services inflation remains sticky (and rising) with the Fed’s favoured super-core (core services ex shelter) having risen from 2.7% as recently as April to 3.2% in July. The Fed’s inflation target is 2%.

Post the jobs numbers and reinforced by the headline inflation data the market is now at a 99.9% chance (FedWatch) of at least a 25bps rate cut at the Fed’s September 17 meeting. Thereafter there are two more meetings this year (October 29 and December 10). The market has pencilled in a further rate cut at the October meeting (71% probability) with a 30% prospect of a third rate cut at the December meeting. Overall, this means the consensus market prediction is – as it was pre July 30th - of an expectation of two 25bps rate cuts by year end, except brought forward to September and October and with the outside chance either of a jumbo cut or a third cut in December.

The prospect of falling interest rates (cheaper money) and an economy moving along robustly has sent share prices stronger, despite concerns over the solidity of the outlook and testing valuations.

Meanwhile the market has shrugged off the impact of the imposition of tariffs on recalcitrant countries who had not reached a reciprocal trade deal by the start of August (Switzerland did particularly poorly) and the increase of secondary tariffs for countries like India deemed to be supporting Russian oil exports. The market particularly welcomed the extension of the pause on incremental tariffs on China imports by a further 90 days until November 10.

Mixed signals in the UK where June inflation rose to 3.6% versus market expectations of 3.4%. Core inflation (ex-energy and food) was at 3.7%, up 20bps from May and services inflation was 4.7%. The Bank of England has warned that inflation is likely to peak at 4% in September, twice its target rate.

Nevertheless, continued weak economic figures with GDP negative in April and May meant that the Bank of England cut interest rates by 25bps to 4% at its meeting on August 7th. It was a close call with a 5-4 second round vote after the first was tied (albeit it was four for ‘no cut’, four for a 25bps cut and one for a 50bps cut). These discouraged markets given the ‘genuine uncertainty’ according to BoE governor Andrew Bailey about the rate of future rate cuts albeit the path ‘continues to be downward.’ Despite UK GDP subsequently rallying to 0.3% growth in Q2, the market still expects one more interest rate cut by the end of 2025 although with less certainty – c75% versus 90% before the BoE meeting.

In Europe, the ECB held interest rates at 2% at its July 24th meeting, pausing a string of rate cuts. It was a unanimous decision and appeared to express some caution ahead of the imposition of US tariffs on August 1. Inflation remained subdued at 2% in July, for the second successive month running at the ECB’s target rate. Expectations, which had been for two more cuts of 25bps by the end of 2025, have moved to just one cut. The sense from the press meeting post the announcement was that the ECB sees the European economy in a good place – inflation at the target 2%, GDP growth levelling out but with a lot of uncertainty either way, casting doubt therefore on the previous assumption that interest rates would continue to fall.

Rothschild & Co strategist Kevin Gardiner summarises the current key drivers of the market in this graphic:

Source: Rothschild & Co

Source: Rothschild & Co

July – VC Momentum sustained

US up 2.2x yoy by value in July; Europe up 15%yoy

US VC raises in July 2025 up 122% on July 2024: July saw 42 US venture capital raises of $100m or above, raising $13.1bn versus the $5.9bn raised in July 2024.

The two largest deals were for AI companies with xAI garnering an investment of $2bn from SpaceX (they all count…) and LLM start up Thinking Machines Lab an initial $2bn. In total there were ten AI deals raising $4.99bn, 38% of the monthly total.

Another $966m was raised for the AI related field of datacentres with the third largest raise overall being $835m for infrastructure and data centre solutions provider, 5C Group.

Fintech continued its revival with $1.57bn of raises led by the $820m at a valuation of $7.5bn for ICapital. The financial operations platform Ramp raised $500m from ICONIQ at a $22.5bn valuation.

Healthcare – five deals raising $870m – and software 54 deals raising $831m – rounded out the leading sectors.

The US – $13bn of US venture backed raises of $100m+ in July

Source: Rothschild & Co

Source: Rothschild & Co

Europe - $4.2bn raised in July: The Rothschild & Co Deal Monitor registered 59 raises of $20m or more in Europe in July with a total value of $4.2bn, up 15% yoy. There were 12 deals raising $100m or more.

The leading sector in terms of value was Software with seven raises bringing a total of $749m with the $200m investment by Accel for Swedish software development platform Lovable the largest. Unusually telecoms was the second largest sector with $709m raised, the bulk of it the $675m funding for FTTP altnet City Fibre led by Goldman Sachs Alternatives.

Climate Tech had eight deals raising $577m. The largest was $162m for Swiss direct air capture carbon removal business, Climeworks. A cluster of five semiconductor raises many focused-on AI applications raised $322m led by $150m for supercomputing and AI focused SiPearl led by Cathaty Innovation. Rounding out the top five sectors three was $284m worth of raises in healthcare, including $110m for Aidoc led by General Catalyst, an AI led tool for helping doctors’ clinical decision making.

Reflecting its lesser role in the VC market in Europe, AI saw four raises for a total of $180m, the seventh largest sector. The biggest raise was for Genesis AI, a full stack robotics business led by Eclipse and Khosla Ventures.

Europe – $4.2bn of VC raises in July

Source: Rothschild & Co

Source: Rothschild & Co

Fundraising outlook: $28bn of potential raises in the hopper

Perhaps remarking the summer lull, as well as the still swelling enthusiasm for AI and related technologies, our monitor of impending raises has risen from c$10bn last month to $28bn.

Recent additions include yet another potential raise for xAI, this one said to be for $10bn at a valuation of $200bn led by the Saudi PIF. Not to be outdone Anthropic is said to be raising a further $5bn in a deal led by ICONIQ at a valuation of $170bn.

AI video generation business Luma is an addition to the list with a planned $1.1bn raise at a valuation of $3.2bn. Another AI video models business, Runway, joins the list with a possible $500m raise at a $5bn valuation to be led by General Atlantic. AI chip business Groq is seen raising $400m at a $6bn valuation.

A couple of interesting European additions to the list. Harmattan AI, a French battlefield drones and software business, is reportedly looking to raise US$200m to help fund a facility to build 10,000 drones per month. German AI business N8n is said to be in a hotly contested round of c$100m at a valuation that might be as high as $2.75bn

Growth Equity – c$28bn in reported upcoming raises

Source: Rothschild & Co; press reports

Source: Rothschild & Co; press reports

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts has led to increased optimism and enthusiasm for growth equity in 2025. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment led to a sharp impact on valuations in private markets. The scale of the fall in the FTSE Venture Capital Index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Outside the AI space the VC market is regaining confidence with a revival of interest in fintech, biotech and software being notable. Certain investors remain very active in the space with substantial funds to deploy. There remains substantial dry powder in the VC industry.

- The speed of the investment process has slowed since 2021-22. The level of diligence on new deals has stepped up.

- 2023 and 2024 saw more downrounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and on DCF and comparative based multiples.

Read the previous editions:

May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025, April 2025, May 2025, June 2025, July 2025

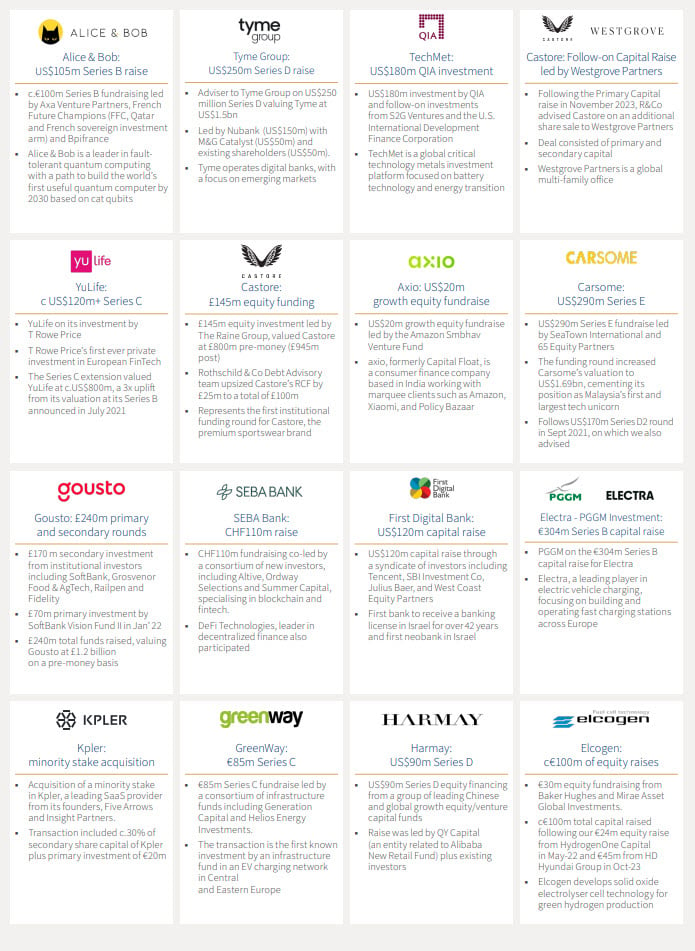

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Thomas Chung

Head of Private Capital, North America

thomas.chung@rothschildandco.com

+1 212 403 5559

+1 917 594 7208

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.