Private Assets: what are the stakes and challenges in terms of allocation in today’s increasingly polarised market?

Macroeconomic and geopolitical conditions have changed extensively in recent years. The rise in geopolitical tensions, recomposition of supply chains and issues associated with energy, commodities and strategic technologies have put an end to an environment of apparent stability.

In such a demanding yet clearer framework, private markets have solidified their central role in financing the economy and building robust asset allocations.

A growing, yet increasingly polarised Private Assets market

The global Private Assets market currently stands at nearly $19,000 billion, two-thirds of which are concentrated in Private Equity. This growth continues to be driven by a search for diversification and performance on the part of all investors, both institutional and individual alike,

It should be noted, however, that this momentum is paired with growing polarisation on the market. Nearly half of all capital raised over the last two years has been entrusted to roughly a dozen global asset managers. This concentration can largely be attributed to the increased complexity of transactions, the need for sourcing that makes a real difference, the growing role of operational support and the sophistication of reporting expected by investors. Larger funds benefit in that respect from specialised teams, established platforms, extensive sector expertise and sizeable capacities for contributing to the transformation of businesses, including certain smaller, specialised sector funds, which draw on comparable know-how in their target areas.

The length of fund-raising campaigns clearly underscores this paradigm. Top-quartile funds are still holding fast campaigns, often under a year, while less attractive funds are seeing their fund-raising periods grow significantly longer, sometimes exceeding two years. Even intermediate funds are subject to longer campaigns as investors grow more and more selective.

Depth of private market: a vast investment universe and attractive multiples

Although private markets are surging, they still represent just a fraction of trading on public markets. In the United States, Private Equity AuM only accounts for around 8% of market cap on the equity and government bond markets versus 6% in 2010. A significant climb, but still modest taken in proportion.

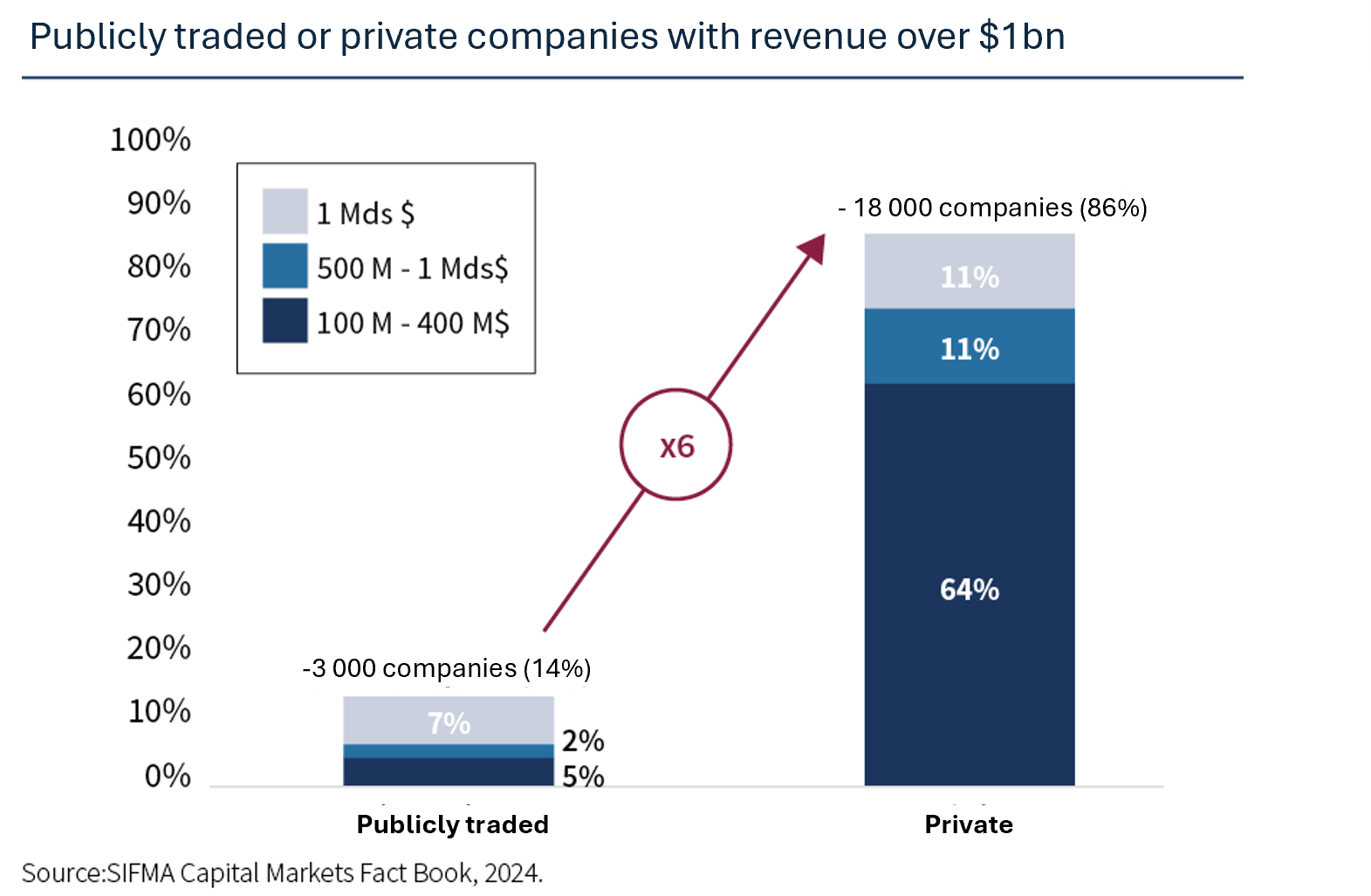

This viewpoint changes radically if you look at the number of potential investable companies. The United States boasts nearly 18,000 companies generating revenue of more than $100 million, whereas only 3,000 companies are publicly traded. In other words, 86% of larger companies are unlisted, forming a pool predominantly consisting of small/mid-market companies ($100 million to $500 million in revenue), which just so happen to be the usual targets for private equity. This universe offers an extremely vast array of opportunities to investors, with the kind of selection you simply cannot find on the public markets, provided of course that you have preferred access to deal flow and the necessary resources to choose and invest in companies over the long term.

Valuation and multiples: scales rebalancing, sparking more trading activity

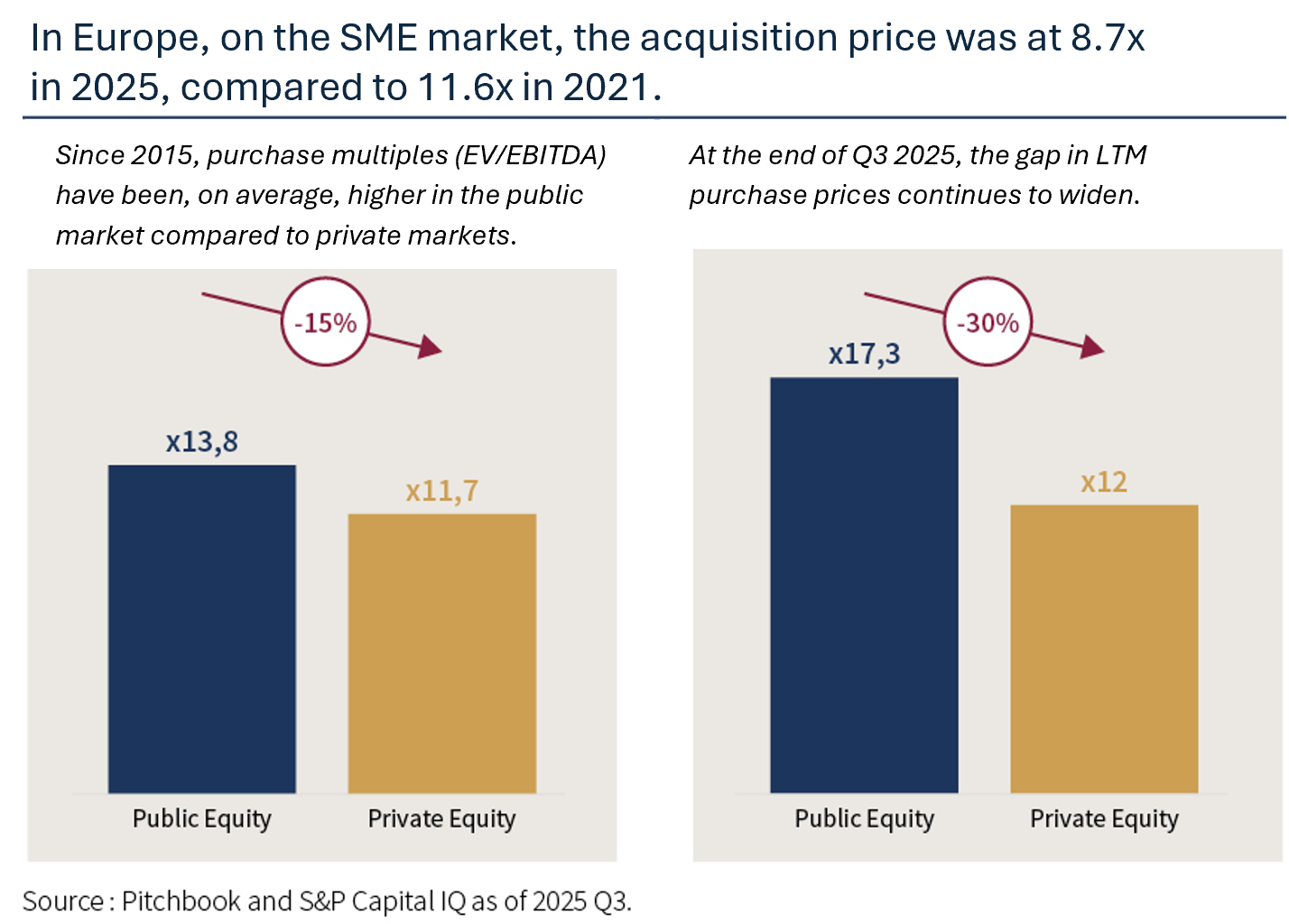

Looking at valuations, on average listed assets are trading at higher levels than unlisted assets. Historically, this difference can be linked to acquisition multiples (EV/EBITDA), which are higher on listed versus private markets.

In Europe, acquisition multiples on the SME segment dropped from around 11.6x in 2021 to 8.7x in 2025, a downtrend that helped restore common ground between buyers and sellers, which is critical in giving a jump-start to trading.

Renewed trading activity and new exit dynamics

After hitting a low point in 2023, trading made a big comeback in 2025. The global M&A market shot up in value, driven by a series of major deals, while the number of transactions held relatively steady.

Trade sales like these proved to be the main exit strategy, accounting for nearly two-thirds of all transactions, with IPOs suffering and still putting up marginal numbers in the current climate.

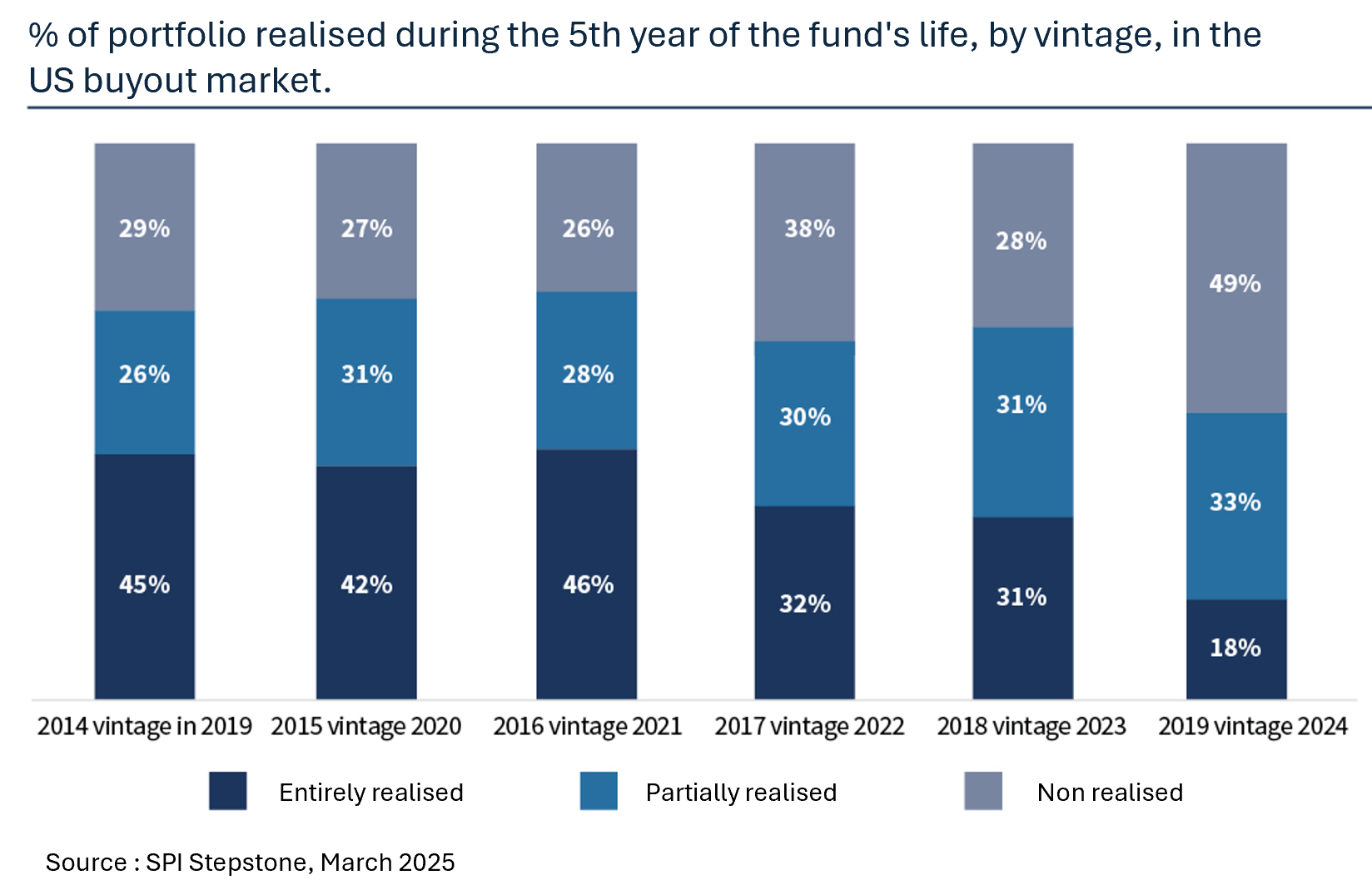

Right now we are seeing investment holding cycles get longer and people tending to sell when industry/strategy conditions are right, rather than setting a pre-defined holding period.

For example, in 2019, one fund had already sold 45% of its portfolio in Year 5 versus 18% in 2024.

A key contributor to this recovery lies in the transatlantic nature of investment flows. Close to 40% of transactions conducted in Europe involved a US buyer, highlighting the importance of doing a comprehensive assessment of private markets.

US investors and manufacturers are still very active in Europe, lured by higher valuations, strong sector positions and consolidation opportunities.

That being the case, you absolutely have to take a transatlantic and comprehensive approach to Private Equity, both in analysing opportunities and in building portfolios.

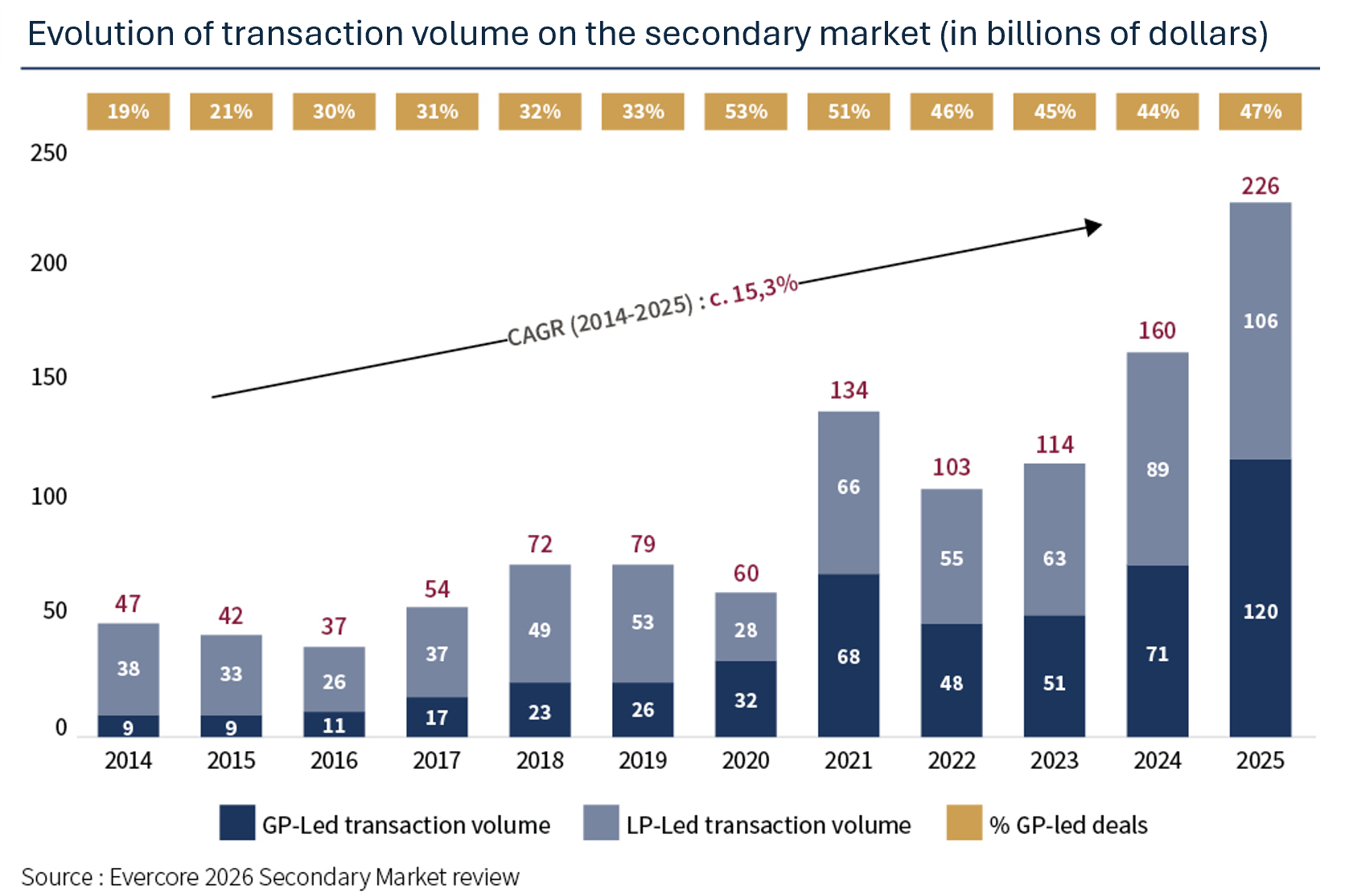

The secondary market can also be seen playing an increasingly central role. With an estimated annual volume of more than $230 billion in 2025, it makes a great tool for dynamic management of unlisted portfolios.

Today’s market is shaped by two complementary dynamics. “LP‑led” deals, initiated by investors, serve to trade portfolios at maturity or rebalance allocations. Meanwhile with “GP-led” transactions, initiated by fund managers (General Partners), investors can get cash distributions if they so choose while extending value creation in persistently attractive assets.

Cash pay-outs are a key factor in the current market environment. After an initial turnaround seen in 2024, the uptrend in distributions took hold in 2025. The overall improvement is a mixed bag, however: some funds are still paying out more than they are investing each year, while others are barely generating any cash pay-outs. This discrepancy has further polarised the market, with fund managers having previously paid lower dividends to their investors now understandably finding it harder to raise new capital. As it stands, distribution capacity has become a key factor in terms of credibility and continued operation for asset management companies.

Private Debt: a critical source of financing for unlisted companies and M&A deals

Private Debt has become one of the main pillars of financing for businesses, especially as banks are tending to steer away from funding LBOs. At nearly $2,000 billion worldwide, Private Debt AuM may still be lower than Private Equity AuM, but that number is steadily climbing. As a result of regulatory changes, since 2008, a portion of private debt activity has shifted away from traditional banks towards non-bank intermediaries, aka private lenders.

Private debt investments are selected on the basis of both the creditworthiness of the underlying companies and the alignment of the fund structure with the type of assets in question, particularly in terms of maturity. It is vital when choosing a fund to make sure the investment structure is appropriate and no promises of pay-outs are made that do not align with the illiquidity of the underlying private loans.

The gearing ratio should also be reasonable and comprehensively assessed, both for the target company and for any underlying operational firms. Lastly, investment discipline and risk management are vitally important, focusing in particular on minimising the loss ratio and obtaining high-quality underlying assets.

Furthermore, as an asset class Private Debt is structurally lower-risk than Private Equity, in that it prioritises capital structure, contractualisation of flows and better visibility on repayments. Private Debt strategies thus offer significant leverage for diversification and generation of recurring income.

Infrastructures: resilience and long-term visibility

Amid rising geopolitical tensions, the energy transition, accelerated digitalisation and sovereignty concerns, critical infrastructure needs (energy, transport, telecommunications, data, water) have taken on structural significance.

These assets generally tend to fulfil a specific purpose, while being subject to high barriers to entry, established regulatory frameworks and long-term contracts. This means they offer greater visibility on future cash flows, often indexed to inflation, making them all the more appealing in such macroeconomically uncertain times.

Globally speaking, funding requirements largely exceed currently projected amounts, leaving considerable room for private capital.

Allocation: selection and diversification still key in wealth management strategies

In the current environment, portfolio building relies first and foremost on an integrated approach, combining strategic asset allocation with well-planned diversification of exposures and rigorous selection of investable companies. Private markets offer a wide range of strategies boasting distinct, complementary characteristics and meeting different goals in terms of holding period, risk profile, flow visibility and value creation.

Each segment helps balance out the portfolio: i) Private Equity supports the growth and transformation of businesses over the long term, ii) the Secondary Market offers faster capital and better visibility on mature assets, iii) Private Debt generates recurring income and structures flows, and iv) Infrastructure gives you resilience, less correlation with economic cycles and protection against inflation. These features complement one another, making it easier to juggle performance, visibility and risk management over time.

In a particularly granular investment universe, the capacity for selection, access and sourcing can make all the difference. Exercising this capacity means, where necessary, adopting diversified approaches – mainly through secondary strategies or multi-fund programmes – in an effort to achieve an effective level of diversification without excessively increasing ticket sizes or calling for a disproportionate amount of investment capital. Discipline is key: over a given number of investment lines, the marginal improvement in risk reduction decreases, while the risk of performance dilution increases.

It is all the more important to be selective when you consider that performance dispersion tends to be significantly higher in Private Equity than in listed markets, and this trend has been gaining steam. This disparity makes it all the more critical to rigorously select fund managers, especially in such a highly fragmented market (the US market has more Private Equity funds than McDonald’s restaurants). In these conditions, only by taking a structured approach will you be able to identify top-quartile funds capable of simultaneously limiting the loss ratio and investing in the most profitable companies over the long term.

Track records in this case cannot simply be stripped down to a number on a page; they have to be analysed in terms of their construction, recurrence and ability to deliver value creation above and beyond the initial business plan. For that, you need teams capable of showing real operational expertise, tailoring their strategies to varying environments and generating performance over time in any market cycle. You also have to keep a close eye on DPI (Distributed to Paid-In), a key metric used to measure how well a fund manager converts value created into real cash for investors.

To that end, complementary methods are used to structure exposures, combining targeted primary market investments with more diversified solutions tailored to certain highly fragmented segments such as US small/mid-caps. This approach combines depth of exposure with overall portfolio visibility.

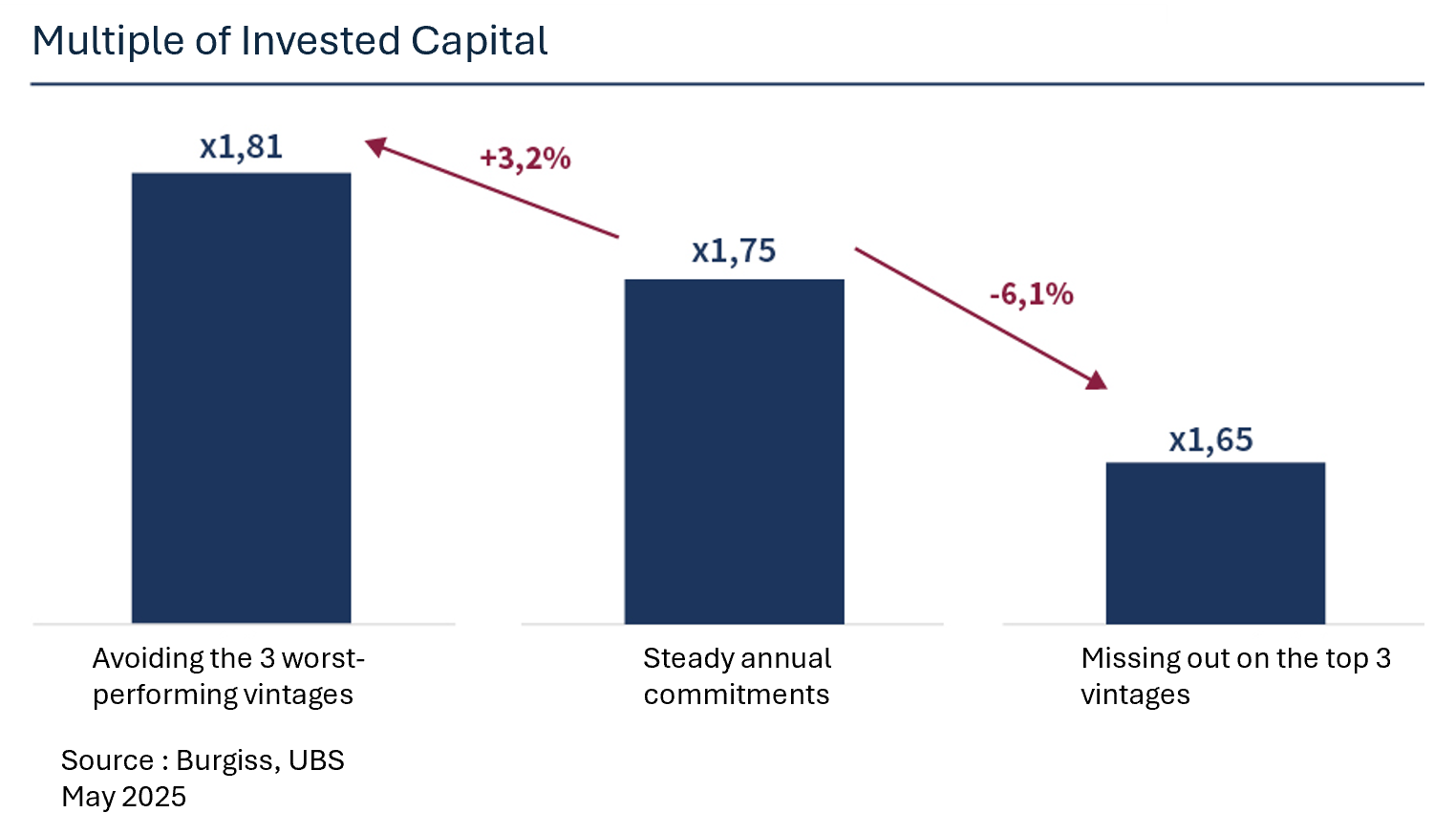

Time is also a major factor when it comes to private markets. Each fund aims for a long-term investment cycle, over the course of which economic and financial conditions will change. Consequently, vintage diversification is a useful tool for managing risk and maintaining a consistent investment trajectory. By spreading investment out over time, investors smooth out their entry points, reduce their dependence on any given environment, and capture performance across all cycles, without seeking to trade in market phases.

Finally, unlisted assets are a natural complement to – rather than a replacement for – listed assets. Listed assets offer liquidity, flexibility and tactical adjustment capability, while unlisted assets offer access to a much broader range of investable companies and ease volatility over the long term. This complementary relationship also makes for more fluid allocation management by gradually financing investments, absorbing capital calls, reinvesting pay-outs and building consistent portfolios aligned with long-term wealth management goals.