Asset Management Europe: Monthly Letter – February 2020

Marc-Antoine Collard, Chief Economist, Head of Economic Research, Asset Management, Europe

Economic environment

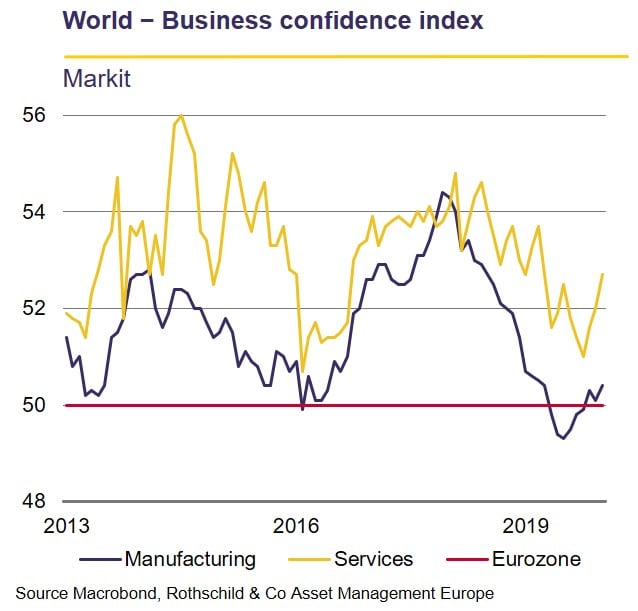

The US and China trade agreement signed in mid-January, the diminished fears of a no-deal Brexit and accommodative monetary policies have all fuelled the enthusiasm of equity investors. Galvanised by tentative signs of stabilisation in economic activity, equity investors seem convinced that world growth will rebound markedly in 2020. The resilience of the service sector has continued, supported by low unemployment rates and a rise - albeit modest - in wages. The Markit manufacturing business confidence index stayed slightly above the 50 threshold for a third month.

Click the image to enlarge

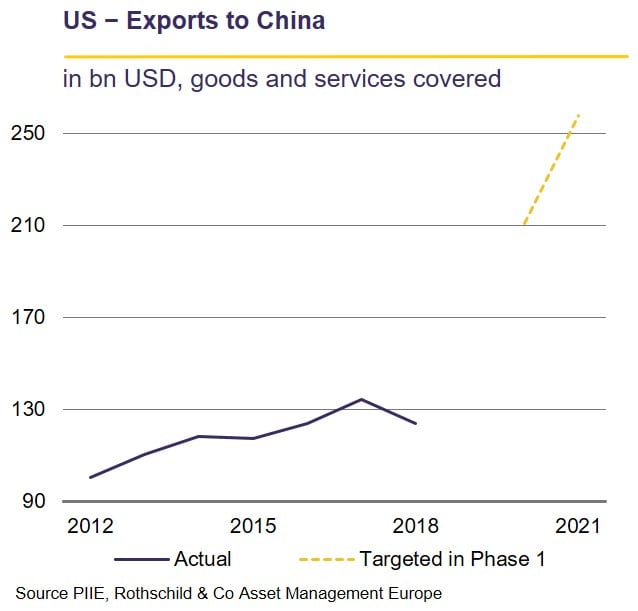

Yet, far from sharing the overwhelming optimism of investors, manufacturing businesses seem perplexed by and question the viability of Phase 1. The centrepiece of this Sino-American agreement is a commitment by China to import an additional USD200bn worth of US imports over the next two years which, if fulfilled, would result in a near doubling of exports to China. The targets look rather unrealistic, however, not only because of the magnitude of the increase, but also because China's domestic demand is losing steam, which will weigh on its imports. The agreement also contains an unprecedented dispute resolution mechanism, one without third-party arbitrators, as is usually stipulated by such agreements. Thus, if the Trump Administration believes China has not respected an obligation, a retaliation kicks in that is proportionate but unilaterally determined by the US.

Furthermore, this 'managed trade' approach will likely create problems and divert, rather than expand, global trade. For instance, in an effort to reach its targets, China could be forced to purchase more American cars (≈ 25% market share) by cutting back on imports from the EU (≈ 50% market share) or Japan (≈ 20% market share). Correspondingly, the EU or Japan could take a case to the WTO, and such a dispute would most likely confront China for failing to adhere to the most-favoured nation principle of nondiscriminatory treatment of imports.

Click the image to enlarge

As with Phase 1, investors also appear to believe that negotiations between the UK and the EU can only lead to a favourable outcome. The two parties have until the end of 2020 to put in place the terms of their future commercial relationship, unless the UK requests an extension by 1 July. EU chief negotiator, Michel Barnier, reiterated that an ambitious trade deal is on offer, although it requires the UK to align itself closely with European regulations. PM Johnson, for his part, pledged that the UK is not leaving the EU to undermine European standards, adding the UK will prosper no matter the nature of the final trade deal secured. In fact, if Mr. Johnson continues to aim for an ambitious trade agreement, many within his party have voiced their preference for exiting without agreement - something the former Government under Theresa May had always wanted to avoid - in the event the EU refuses to abandon part of its demands.

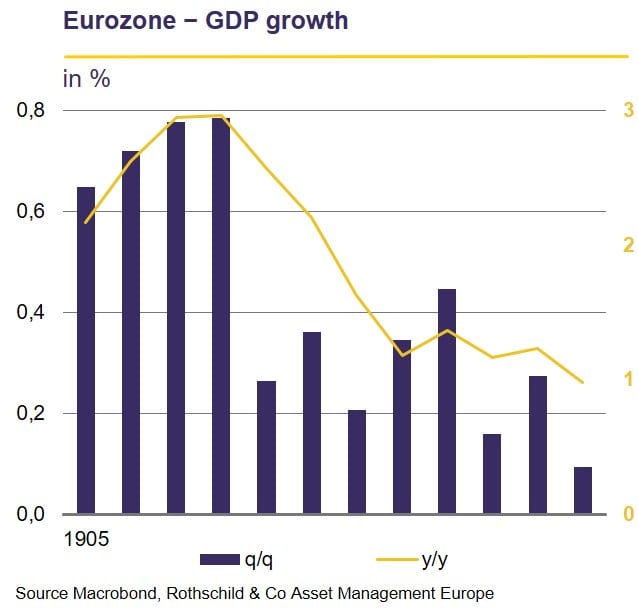

Meanwhile, if business surveys and other soft data can, in part, explain investors' elevated expectations, global macroeconomic statistics do not show, for now, a clear inflection in real activity, the most convincing example being in the eurozone. According to a flash estimate published in mid-January, economic growth has continued to falter in Q4 2019, with GDP recording its weakest pace (0.1% q/q) since 2013. Dynamics in France (-0.1%) and in Italy (0.3%) were particularly poor, while Spain (0.5%) was once again the main driver. What's more, recent data suggest that the flash estimate will be revised downward, notably due to disappointing statistics in Germany.

Click the image to enlarge

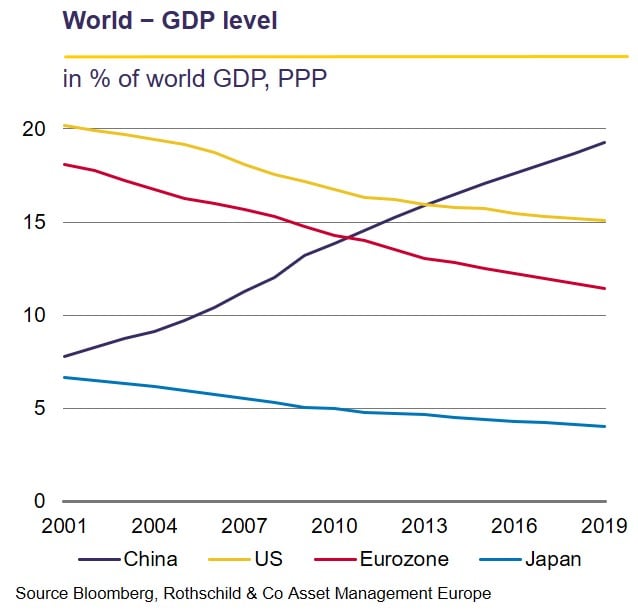

Overall, even before the coronavirus outbreak, the balance of risks to the global outlook remained on the downside and, unlike what was hoped for by most market participants, growth in 2020 was likely to remain close to 2019's pace, the lowest in a decade. The virus epidemic now affecting - mainly - China exhibits a lower fatality rate than SARS in 2003, although it is spreading significantly faster. According to various studies, SARS caused a net loss of economic activity in China estimated between 0.5 and 1.5 point of GDP. Since then, however, the weight of China's service sector has increased significantly, making the economy more vulnerable to the current turmoil. What's more, a prolonged decline in household consumption would also penalise investment since capital spending by Chinese firms has become extremely sensitive to domestic demand.

Click the image to enlarge

Understanding the impact of today's outbreak on the global economy is all about identifying the transmission channels: reduced goods imports by China, fall in tourism visits from Chinese nationals, supply-chain disruptions due to shortages of Chinese-produced intermediate goods, and financial market and business confidence effects. As China's weight in the world economy has tripled in the past two decades, the coronavirus acts jointly as a demand and supply shock. In addition to weaker Chinese import demand, a sharp drop in the country's industrial activity may cause substantial supply-side disruptions elsewhere. China's dominant manufacturing position suggests that, in the near term, finding substitutes for disrupted suppliers will be difficult. Therefore, a significant drop in economic growth in Q1 2020 is expected, although the magnitude will depend on the development of the epidemic. The longer current travel restrictions are maintained, the stronger the impact on activity, and the effects will probably not be linear nor homogeneous across sectors.

Admittedly, stimulus measures could facilitate the recovery and most investors have concluded that this is only a temporary cloud, expecting a V-shaped pattern for growth during H1 2020. However, uncertainty remains in a context where the world economy was already advancing at a slow pace, not too far from the stall speed... which has not escaped sovereign bond yields renewing their downtrend, once again diverging from the equity markets.

Download the PDF version Monthly Letter (627 KB)