Growth Equity Update

May 2025 – Edition 38

- 2025 venture capital funding growth led by AI: To the end of April the value of US venture raises is up 3x yoy to $77.7bn while Europe is up almost 20% to $13.6bn. Driven by the $40bn raise for OpenAI, 65% of all US funding ytd has been for AI.

- But not the whole story. US ‘non-AI’ raises up 67% ytd. Outside of AI the VC market is growing healthily. Excluding AI deals from both years, funds raised for ‘non-AI’ US companies are up $11bn or 67% yoy with software, biotech, fintech and cybersecurity strong.

- Europe ‘non-AI’ raises up 14% yoy: In Europe total VC funding to end April is up almost 20% to $13.6bn with AI at 10% of the value. Excluding AI from both years, the value of VC raises is up $1.7 bn yoy or 14%. Fintech and biotech have rebounded strongly. We look at the drivers.

- Public markets recover: The de-escalation of the US tariff regimes have seen public markets more than recover their post April 2 losses with the S&P 500 up marginally ytd. The FTSE Venture Capital Index is now up 10% ytd with an advance of 19% since April 2. We look at the implications of tariff uncertainty on venture backed businesses.

- New Mansion House Accord: In the UK 17 of the largest DC pension funds have pledged to invest at least 10% of their defined contribution default funds into private market assets by 2030, potentially unleashing an incremental initial c$50bn of funding for private assets, with at least half earmarked for the UK. Rothschild & Co is hosting a London conference on 10th June – Funding the UK Innovation Economy- Delivering on the Mansion House Accord.

- April saw $8.3bn of US VC deal raises, up 102% yoy. Europe was up 5% at $2.3bn.

- Chaos is merely disorder waiting to be deciphered - José Saramago

Click here to download a PDF version of Growth Equity Update

Venture Capital funding growth – is it all AI?

No. In the US ‘non-AI’ VC company funding is up $11bn or 67% yoy to the end of April. In Europe ‘non-AI’ funding is up 14% or $1.7bn yoy.

The VC funding market has certainly surged year to date with the US up 3x to $77bn in terms of funds raised to the end of April 2025 and Europe up 19% to $13.6bn in the same period.

To what extent is this just a phenomenon of raises for AI businesses? Since the emergence of OpenAI in 2023 we have seen substantial support initially for LLM businesses led by OpenAI, Anthropic and xAI in the US and Mistral in Europe. The second phase of AI investment has centred on the infrastructure of AI ranging from AI centric semiconductor development to the datacentres required for the compute needs of the industry. The third phase is investment in application specific AI businesses across a range of applications from voice assistants, legal document drafting, biotech discovery and software coding.

The next table shows the scale of US AI raises in the first four months of 2024. Across 15 deals a total of $3.18bn was raised with the largest single raise being $675m for Figure AI.

US AI related raises totalled $3.18bn in the first four months of 2024

Source: Rothschild & Co

Source: Rothschild & Co

The next exhibit gives the equivalent data for the year to end April 2025. In total across 35 rounds $50.3bn has been raised for AI related businesses.

- In the first four months of 2024 the $3.18bn raised for AI companies represented 16% of total US venture funds ($19.6bn) raised in that period.

- In the first four months of 2025 the $50.3bn raised for AI companies was 65% of total US venture funding ($77.7bn).

- If we adjust the 2025 figure for the $40bn OpenAI raise, treating it as an outlier, then the ‘other’ AI companies raised $10.3bn, still 3.2x the level of AI raises in the first four months of 2024. They represented 27% of the total funds raised in the US on this basis.

- Taking all AI raises out of the equation, US VC funding would have totalled $16.4bn in the first four months of 2024. Doing the same for 2025 sees the ‘non-AI’ VC market raises at $27.4bn.

- This implies that – ex AI – VC market raises are still up $11bn yoy, equivalent to growth of 67%.

US AI related raises were $50.3bn in the first four months of 2025

Source: Rothschild & Co

Source: Rothschild & Co

In the European growth equity market, the AI phenomenon has been more subdued.

- In the first four months of 2024, allowing a fairly wide definition, $802m was raised for European AI businesses. The largest raises were $110m for autonomous vehicle business Project 3 Mobility and $100m for AI robotics business, IX.

- AI represented 7% of total VC funding of $11.4bn in that period.

- In the first four months of 2025 there were nine rounds for AI related businesses raising $1.28bn, the largest being $600m for Isomorphic Labs and $180m for Synthesia.

- AI represented 9.4% of the total $13.6bn raised for VC backed companies.

- Taking all AI raises out, European VC funding would have totalled $10.6bn in the first four months of 2024 with the ‘non-AI’ VC market raises at $12.3bn in the first four months of 2025.

- Total VC funding of European businesses is up $2.2bn or 19% yoy to the end of April 2025 ($13.6bn versus $11.4bn)

- Excluding AI related raises from both years the VC market is up $1.7 bn yoy ($12.3bn versus $10.6bn) or 14%

European AI raises totalled $802m in the first four months of 2024

Source: Rothschild & Co

Source: Rothschild & Co

European AI raises totalled $1.28bn in the first four months of 2025

Source: Rothschild & Co

Source: Rothschild & Co

What does this indicate?

- There is an underlying buoyancy in the venture capital/ growth equity market in 2025 that extends beyond the excitement engendered by AI and its applications.

- This is particularly marked in the US where total funds raised for ‘non-AI’ businesses are up $11bn or 67% yoy.

- It is also true though of Europe where ‘non-AI’ funding has grown 14% or $1.7bn yoy.

Some of the enthusiasm may reflect a general optimism around the potential of AI deployment within ‘non-AI’ companies to improve their prospects, either in more rapid product development, more efficient sales and customer targeting or through the ability to use AI to reduce labour costs and improve margins. It is clear that venture backed companies are aware of this potential. It is rare to see a pitch deck from a growth company (or a public company) that does not extol the benefits that the deployment of AI may bring to its operations. Investors may be picking up on that potential.

What other factors can be driving this underlying improvement?

- Macro conditions have improved for venture backed companies. After the period of sharp increases in interest rates, funding costs and investment hurdles post the outbreak of the Ukraine war, the interest rate cycle has turned down with sharply falling interest rates in Europe, a steady pace of cuts in the US and somewhat slower progress in the UK. Even the recent scare over tariffs has induced a response that the Fed will have to cut interest rates more quickly than it was doing hitherto.

- VC backed companies have improved. Many companies have adapted themselves to the more rigorous funding conditions post 2021 with a greater balance between the pursuit of revenue growth and the attainment of profitability and positive free cash flow. As a result, the better companies are typically in better shape.

- Valuation expectations have been tempered making it easier for funds to invest. Asked to pay 13-14x ARR in 2021 for SaaS based businesses investors are now looking at c6.5x, making acceptable returns more visible.

- Two strong years of public stock market performance (the S&P 500 was up 24% in 2023 and 23% in 2024) have engendered a positive background tone.

- While the IPO market is yet to relight, the positive public market performance has at least raised expectations that the IPO market should recover well before most of the companies now being funded will be ready to take advantage of it as an exit option.

Where is the incremental enthusiasm being felt?

- In the US there has been a marked resurgence of activity in biotech in the second half of 2024 and into the first half of 2025.

- Fintech has also seen a recovery and with a lot of activity in the secondary market as well as in primary. Blockchain and crypto, which fell away sharply after the collapse of FTX, has also been attracting more funding rounds in recent months.

- Software remains a consistently strong category. Perhaps reflecting the heightened risk of cyber-attacks on corporates, cybersecurity has seen a string of substantial raises at the start of 2025.

In Europe, the influence of AI has not been as marked on the fundraising scene. Our sense is that a lot of European managers have marked out AI as an area in which to invest, but have seen limited opportunities as yet to do so. Elsewhere we see similar trends as in the US.

- Fintech has rebounded strongly in Europe in the last twelve months and remains a favoured area of focus for many managers.

- Biotech has, like in the US, seen much greater prominence in fundraising.

- Software remains a favoured sector.

- The start of 2025 has seen a surge in fundraising for datacentres – obviously, AI connected. There has been a fall away in funding rounds for big climate tech projects.

- A couple of smaller sectors have seen unusual prominence early in 2025, notably a series of raises in Health tech.

So why do we hear from many companies operating outside AI that they find fundraising more difficult and that investors appear interested only in AI and related projects? We partly addressed this in our last Growth Equity Update in discussing how venture capitalists allocate their time. Factors include:

- VCs are clearly very interested in AI opportunities at the moment. Given the extraordinary perceived opportunity in AI and related businesses it is natural that, in a VC model in which a few numerical successes provide the bulk of the returns for funds, AI should receive disproportionate attention.

- We have seen too that there is strong competition between funds to get involved in AI deals. Founders in these AI businesses thus have greater sway in terms of valuation and terms in fund raises than their counterparts in other businesses.

- This gives rise to the sense of a two-tier market - that there is one set of conditions for AI businesses and one for everything else.

- The anecdotal experience is that, in non-AI rounds, the process of fund raising is relatively slow, there is substantial due diligence from investors, downside protections are often sought and there is, in many generalist funds, a reluctance to pursue long cycle, pre revenue projects.

- A feature of the market is that fundraising by VCs is dominated by the larger firms. This means that the financial firepower in the market is also more concentrated.

- For all VC firms there is a question of resource management. Most firms will concentrate their expertise in areas where they think they have a strong track record, better knowledge, and competitive advantage. Most of the larger firms therefore specialise in the larger sectors where the scale and range of investment opportunity is bigger – software, AI and related, fintech, climate tech, biotech. It means that businesses operating in relatively esoteric fields without a lot of counterparts may struggle to get their attention and conviction of firms’ intent on focusing their resource on what they perceive as the areas of leading opportunity.

The new Mansion House Accord

17 of the UK’s largest DC pension funds have now pledged to invest at least 10% of their defined contribution (DC) default funds into private market assets by 2030, potentially unleashing an incremental initial c$50bn of funding for private assets with at least half earmarked for the UK

Successive UK governments have seen a big opportunity in encouraging pension funds to divert more of their assets to potentially high growth, high return early-stage assets and in doing so promoting investment in UK growth and addressing the funding gap that appears to exist for UK growth equity companies.

The original Mansion House Compact was announced by the UK government in July 2023. The key initiative was to ensure the channelling of some part of defined contribution pensions into private companies.

At that stage eleven of the UK’s largest pension providers to commit 5% of their ‘default’ funds from defined contribution pensions to private companies and start-ups by 2030. They represented around two-thirds of the UK’s DC workplace market and at time of signature were investing just c0.5% of their assets in unlisted UK companies.

Simultaneously the UK government targeted a shift in the investment intentions of local government pension scheme allocations to encourage them to double investments in private assets to 10% from c5% presently, unlocking another potential c£25bn in additional investment into private companies and projects by 2030.

In early May 2025 the current government, which has emphasised the need for economic growth in the UK and has pledged to encourage investment, announced an update to the scheme. The new Mansion House Accord’s mission is to ‘unlock up to £50 billion investment for the economy, with first commitments to invest in the UK.’

The Mansion House Accord is designed to unlock investment into UK businesses and major infrastructure projects, including clean energy developments and it claims to have more ambitious targets than the 2023 Compact.

The Accord comes ahead of the Pensions Investment Review final report, which the government says, ‘will create megafunds to drive more investment, boost pension pots and grow the economy through the Plan for Change.’

The key elements of the new Mansion House Accord announced on May 13 are:

Seventeen of the UK’s largest workplace pension providers have signed the Mansion House Accord. These pension providers manage around 90% of active savers defined pension contributions.

The original eleven signatories of the Mansion House Compact were Aegon, Aon, Aviva, Cushon, Scottish Widows, Legal & General, Phoenix Group, Nest, Smart Pension, M&G and Mercer. They have now been joined by eight new signatories - LifeSight, NOW: Pensions, Royal London, Smart Pension, the People’s Pension, SEI, TPT Retirement Solutions and the Universities Superannuation Scheme (USS).

One of the original signatories has not signed the new accord. Scottish Widows, owned by Lloyds Bank, has welcomed the initiative saying that it is positive to see agreement on furthering investment in the UK. It has indicated that it is to set up a separate asset fund to be announced later this year and that the group already has £5.5bn worth of extensive long-running investments in UK equities.

The seventeen signatories to the Mansion House Accord will pledge to invest 10% of their workplace portfolios in assets that boost the UK economy such as infrastructure, property, and private equity by 2030. This is a step up from the 5% that was the commitment in the original Compact.

Answering an earlier perceived weakness of the scheme, these providers have pledged that at least half (5%) of these DC default funds will be allocated to the UK assuming there is a sufficient supply of suitable investible assets for providers. The government says that this should release ‘£25 billion directly into the UK economy by 2030.’

The signatories to the Accord have stated that £252bn of assets are subject to the pledge. Based on historical growth rates (17% pa) and reflecting further consolidation in the pensions market, this could rise to around £740bn by 2030.

The government’s figures of £50bn of extra investment to be unlocked and £25bn ringfenced for the UK are indicative and assume current private market investment levels are at 3.5%, of which 40% is UK-based. These are increased to 10% and 50% respectively by 2030 in line with the Accord.

At a practical level, given the scale of these funds it is likely that most of this funding would, in the growth equity market, go to later stage deals where a large institution would be able to lead rounds and deploy meaningful amounts of capital with tickets in the $50-100m range and above.

To give an indication of the sort of projects the UK government would like to see as a result of the Accord it comments:

‘This investment could support clean energy developments across the country, delivering greater energy security and helping to lower household bills, as well as delivering growth finance to Britain’s world-leading science and technology businesses - creating jobs, boosting businesses and putting more money into people’s pockets.’

The government’s announcement indicates that ‘progress against the commitment will be monitored.’ The signing of the Accord is a voluntary expression of intent by the signatories. There remains a debate about whether the commitment might become mandatory over time. The UK government also has a pensions bill later this year and it indicates that the Accord:

‘…will be reinforced by measures to be announced in the upcoming final report of the Pensions Investment Review. The final report will tackle fragmentation in the UK pension system, creating pension megafunds that take advantage of scale and consolidation like Australian and Canadian funds do, to invest in productive assets like private markets and big infrastructure projects.'

The new pension schemes bill is expected to have a clause giving the UK government ministers a reserve ‘mandating power to set binding asset allocations.' Asked post the announcement of the Accord whether the government would at any stage mandate pension funds to the 10% commitment, Chancellor Rachel Reeves said, ‘never say never’.

This approach is resisted in the pensions industry whose first responsibility is to the pensioners in the schemes. Amongst signatories to the Accord, David Lane, CEO of TPT, commented that mandation ‘would open up a load of investment challenges in terms of fiduciary duty and outcomes for members’ while Benoit Hudon, chief executive of Mercer UK, observed that ‘One of the points we insisted on is that there be no mandation….because if you force everyone to move to the UK, creating all that demand, it may be that just by virtue of market forces, you end up paying too much for something'

On the other hand, the government claims that some of the pension funds have indicated privately that they will go beyond the targets agreed through the Mansion House Accord.

The commitment is dependent on implementation by the Government and regulators of critical enablers. Barriers to invest in private assets have reduced in recent years but the role of government and regulators in supporting the industry in securing a pipeline of UK investment opportunities and facilitating the Value for Money framework for investors will be critical.

Rothschild & Co is hosting an event - Funding the UK Innovation Economy: Delivering on the Mansion House Accord on Tuesday 10 June 2025 in London.

Rothschild & Co is hosting this event to bring together senior level policy makers, pension fund allocators, regulators, UK venture and growth investors and UK based innovation businesses. We will discuss progress towards achieving the 10% target, the barriers which still exist, and the UK sectors with sustainable competitive advantage best placed to benefit from this new capital.

If you would like an invitation to the Funding the UK Innovation Economy event on June 10 please contact Tim Brenton or Patrick Wellington.

Markets rebound as tariff fears are subdued

Chaos is merely disorder waiting to be deciphered. José Saramago

The gradual partial dismantling of the ‘Liberation Day’ tariff regimes first announced on April 2 has come as a great relief to markets. The universal 10% tariff on imports to the US remains. The incremental tariffs on 60 counties have been suspended for 90 days until July 9th. The US has announced that it is in trade talks with multiple countries and the first such deal – with the UK – has already been signed. Critically the US and China have agreed to suspend tariffs on each other’s goods for 90 days with ‘reciprocal’ tariffs between the countries being cut from 125% to 10% although the US has retained its 20% duty on Chinese imports relating to fentanyl, meaning total tariffs on China are at 30%.

The China deal in particular encouraged markets that the US administration has responded positively to the threat to global GDP growth its tariffs represented, a point that has been made by many US and Europe CEOs in their Q1 results comments.

As a result, equity markets have retraced and more the post April 2 losses meaning that the S&P 500 is now up marginally ytd. As the Exhibit shows the ‘natural’ hierarchy of recent times, with the tech favoured indices outperforming, has been resumed with the April 2 to May 14th performance being headed by the Magnificent 7, followed by NASDAQ, then the S&P 500, then the European STOXX600 with th1e FTSE 100 bringing up the rear and actually underperforming marginally in that period.

Impact of tariff announcements - Performance of major indices

Source: Rothschild & Co

Source: Rothschild & Co

The markets remain very sensitive to the daily flow of news from the White House with occasional checks to the recovery, such as on the day that the administration announced tariffs on non-US movies. There is likely to be increased nervousness if the 90-day tariff suspension deadline on July 9th is approached without further indications of whether the suspension will be extended.

The FTSE Venture Capital Index which measures the performance of the US venture capital industry, with a strong sector weighting towards technology, was in mid-April down 12.5% from the start of the year. With an advance of 19% since April 2 It is now up 10% ytd.

Deal announcements still robust: Most growth rounds are the result of several months work and so the short-term trend in these announcements is not a particularly good reflection of any impact there may have been from the tariff uncertainty. May has continued to see a healthy flow of substantial deals including a $900m raise for AI business Anysphere at a $9bn valuation; a$600m raise for food delivery business Wonder and a $450m raise for HR management software business Rippling at a $16.8bn valuation. In Europe in May defence aerial intelligence business Quantum Systems has raised €160m and agentic AI business Parloa $120m at a $1bn valuation. Our monitor of impending deals –those reported to be underway but not yet announced – is at a higher total in mid-May than in mid -April with almost $30bn of deal value in the offing.

Liquidity issues: One of the key concerns post Liberation Day was the immediate impact it had on the exit market. With the sharp rise in the VIX volatility index, from 21 immediately before the tariff announcements on April 2, to 52 on the day before their suspension on April 9, the IPO market seized up with several high profile planned IPOs being postponed. Typically, the IPO market operates best when the VIX is below 25. The VIX hit 25 at the end of April and currently (15 May) stands below 20. As a result, a trickle of IPOs has resumed in the US.

General partners though remain under pressure to provide liquidity to limited partners. The IPO markets have already been functioning at a low level for the last three years amid a weak overall environment for exits. Indeed, Crunchbase recently calculated that, at the current rate of exits, it would take 30 years for every US. company on its register of US unicorns to go public or be acquired. Without the liquidity produced by active levels of exits, the ability to raise and reinvest in new growth equity funded companies is reduced.

Pressure on fundraising valuations: The heightened uncertainty that remains even as the immediate impact of the new tariff regime has softened persists. Venture and growth investors will assume that the ramifications of the tariff uncertainties will hit venture backed companies as they would public companies and that the effect on these smaller, typically less well-developed businesses -often a narrower range of customers and less financial flexibility- may be greater.

Investors will likely therefore be cautious about the impacts on revenue growth, profitability, and path to cash flow break even. Already slow fund-raising processes (outside AI) may become yet slower and there may be further impacts on the valuation and protection that investors seek in new rounds.

In the meantime:

Fed interest rate cuts -mixed signals: Prior to Liberation Day the market had been anticipating two more interest rate cuts in 2025 in line with the official Fed dot plot. Post Liberation Day the market factored in at least three interest rate cuts in the expectation that this would be needed to stave off a faltering economy. Since then, the administration has softened the message on tariffs and a series of other factors have come into play:

- Despite some apparent dissatisfaction with the performance of the Fed, President Trump has confirmed that he will not seek the early departure of Fed Chairman Jay Powell from his post. Jay Powell’s term as chair of the Fed runs until May 2026 and his term as a Board of Governors member until January 2028. Mr Powell has said that he has no intention of leaving as chair before the end of his term. The market views him as dispassionate and consistent in an otherwise volatile environment.

- US GDP fell unexpectedly by 0.3% in Q1 (the consensus forecast was +0.4%), although this was widely seen as an aberrant number caused by a surge in imports as companies anticipated the tariff announcements on April 2. A slowdown in consumer spending and the impact of DOGE reforms on federal spending were also partly attributed for the decline. It was the first quarter of negative growth since Q1 of 2022.

- The April inflation number, announced in mid-May, was better than expected with US inflation falling to 2.3% against expectations of 2.4%. It was the third consecutive month both that inflation declined and was below expectations. Encouragingly some of the sub-indices of ‘sticky’ services inflation showed positive signs. The core inflation rate, excluding food and energy products, remained flat at 2.8%. The ‘supercore’ index of services (which excludes shelter costs) and is a measure favoured by the Fed fell to 2.7%, its lowest level since 2021. Shelter inflation is also falling.

In its meeting on May 6th the Fed kept interest rates unchanged at 4.25%-4.5% - it has kept rates unchanged since January. Jay Powell commented that the Fed will watch to see what impact the tariff policy changes would have on the data although it observed that the 'risks of higher unemployment and higher inflation have risen.’

Nevertheless, the April employment numbers were decent (+ 177,000 jobs with the unemployment rate steady at 4.2%) and were followed by the subsequent better than expected April inflation number. All of this is sending mixed, but perhaps marginally improved messages about the economy, to the Fed reducing the immediate likelihood of a resumption of interest rate cuts at its next meeting on June 6th.

Jay Powell’s comments in response to a question on consumer sentiment (which has deteriorated) might stand for his overall response to the current flow of data, 'the timing, the scope, the scale and the persistence of those effects are very, very uncertain, so it’s not at all clear what the appropriate response for monetary policy is at this time….It’s still a healthy economy.'

Few expect an interest rate cut at the next Fed meeting on June 6th. Thereafter there are four more meetings to the end of the year (July 30, September 17, October 29 and December 10). The market appears to put a July rate cut at about a 50% chance although it thinks at least one rate cut by the September meeting is very probable with then at least one more cut at either the October or December meeting to leave rates at 3.75%-4% by year end.

The Rothschild & Co strategists Kevin Gardiner and Anthony Abrahamian illustrate the potential economic impacts of a range of the Trump administration’s initiatives in the following graphic.

The potential impacts of President Trump’s policy agenda

Source: Rothschild & Co

Source: Rothschild & Co

Meanwhile in Europe the ECB cut interest rates in mid-April by a further 25bps to 2.25%. This was the third rate cut of 2025 so far and the seventh since June 2024. The April inflation number, published in early May was flat month on month at 2.2% and was worse than expectations of 2.1%. Underlying inflation trends looked unfavourable with core inflation, excluding energy and food, up 2.7% from 2.4% in March and worse than market forecasts of 2.5%. Services inflation, typically sticky, rose to 3.9% versus 3.5% in March.

Nevertheless, in its April meeting the ECB cited ‘rising trade tensions’ as potentially exacerbating already slow growth in Europe (GDP growth was 0.4% in Q1). Despite some commentary from ECB Board members that higher fiscal spending in Germany and the impact of tariffs mean the risks to inflation are ‘likely tilted to the upside’ the market confidently expects another 25bps rate cut at the next ECB meeting in June and a further two cuts by the end of the year.

In the UK, the Bank of England cut interest rates in early May by 25bps to 4.25%. The Monetary Policy Committee though was split om the decision and the accompanying commentary stated that the BoE would take ‘a gradual and careful approach’ when considering further rate reductions. The BoE forecasts show inflation peaking at 3.5% in Q3 and then reverting to its 2% target in 2027. The BoE Governor Andrew Bailey commented that ‘The past few weeks have shown how unpredictable the global economy can be. That’s why we need to stick to a gradual and careful approach to further rate cuts.'

The market had been factoring in three rate cuts by the end of the year prior to the rate cut announcement, tempering that to an expectation of two cuts after the BoE’s comments.

The Boe’s latest forecasts published after the May meeting expect UK GDP to grow by 1% in 2025 and 1.25% in 2026 with the forecasts assuming that the suspension to the Liberation Day tariffs will continue after the current 90-day hiatus. The BoE’s forecasts are based on interest rates falling from the current 4.25% to 3.5% in 2026. Figures published in mid-May showed the UK economy grew by a better than expected 0.7% in Q1, up from 0.1% in Q4 2024. Within this the March growth number was also better than expected at 0.2% growth versus market expectations of zero.

Market expectations for interest rates

Source: Rothschild & Co/ Bloomberg

Source: Rothschild & Co/ Bloomberg

Rothschild & Co strategist Kevin Gardiner summarises the current key drivers of the market in this graphic:

Source: Rothschild & Co

Source: Rothschild & Co

April – Growth equity raises still advancing

Another healthy month for growth equity raises and no apparent sign as yet of tariff related slowdown.

US $8.3bn of VC deal raises in April, up 102% yoy: April saw 38 US venture capital raises of $100m or above, with the $8.3bn raised double the $4.1bn of April 2024.

This brings the ytd total to $77.7bn, almost 3x the end April 2024 level. Even stripping out the largest single deal of 2025, March’s $40bn for OpenAI, the yoy total is still 93% ahead of the 2024 level.

AI still dominating: Almost 40% of April’s raises were for AI related businesses.

The largest deal of the month was the $2bn raise for Safe Superintelligence (SSI) at a valuation of $32bn led by Greenoaks. The business was founded in 2024 by the former chief scientist at OpenAI, Ilya Sutskever with its first funding round being a $1bn round at a $5bn valuation in September 2024. The concept behind SSI is that it creates superintelligent AI that is safe for humanity. The company is pre-product being as yet solely focused on foundational research, although it is believed to be considering applications in healthcare and education.

Sandbox AQ raised $450m from a group of investors that included Google and Nvidia. Its concept is the development of quantitative AI platforms across biopharma, chemistry, materials science, cybersecurity, and financial services. The third AI deal in the top five US raises in April was the $308m raise for Runway led by General Atlantic, FMR and Baillie Gifford. Runway has developed a group of AI media tools, including video generating models for use in film and video production.

In fintech Plaid raised $575m in a deal led by Franklin Templeton, Fidelity and Blackrock valuing the business at $6bn, down from the $13.4bn at which it raised in 2021. The round was staged to allow employees to monetise restricted stock units. Plaid’s APIs connects bank accounts to financial applications.

Cybersecurity business Chainguard raised $365m from Kleiner Perkins and IVP in as Series D round that valued the company at $3.5bn. The business builds and sells ‘hardened-by-default’ open-source components and has ARR of c$100m in 2025.

The US – $8.3bn of US venture backed raises of $100m+ in April

Source: Rothschild & Co

Source: Rothschild & Co

YTD our Deal Monitor has recorded 141 raises of $100m or more in the US raising just under $78bn. This is well ahead of the c$33bn raised in the US IPO markets in the same period. The 22 US AI deals have raised just over $50bn, 65% of the total.

AI has provided four of the seven raises of $1bn and above (Open AI $40bn, Anthropic $3.5bn, SafeSuperIntelligence $2bn, Anthropic again $1bn). Metaverse business Infinite Reality raised $3bn. The other two substantial raises were heavily AI related. There was a raise of $1bn for social media platform X, which was subsequently absorbed by xAI. Anti-ageing biotech Retro Biosciences also raised $1bn. It is heavily backed by OpenAI’s Sam Altman who funded the entirety of the company’s previous $185m round.

If we extract the $40bn OpenAI deal out of the first four months statistics, then the fund-raising total was $37.7bn, still 93% ahead of the same period in 2024 with AI, on this basis, at 27% of the total.

$78bn of US VC /Growth raises ytd to end April, 3x the level of 2024

Source: Rothschild & Co

Source: Rothschild & Co

Europe - $2.3bn of VC deal value in April: Seasonally April tends to be one of the slower months of the year for VC raises. In Europe, our Deal Monitor recorded $2.3bn of venture capital raises in the month, $1.5bn lower than the March total but still up 5% yoy.

There were five European deals of $100m or more in April led by $132m for medical device business CMR Surgical led by SoftBank and Lightrock to accelerate the US expansion of its core surgical robotics product, the Versius System. There was an associated $68m debt raise led by Trinity Capital.

German solar energy business Enpal raised $121m in a deal led by TPG and Softbank. In March 2024, the business raised €1.1bn in debt commitments to facilitate solar and heat pump adoption amongst German households. The latest raise is to fund expansion into new markets and to roll out a new energy trading platform.

Croatia’s Verne (formerly Project 3 Mobility) raised $110m - investors were not disclosed.

Spain’s Job&Talent is a 'workforce as a service' marketplace that connects people with companies looking for hourly workers. It raised a $103m Series F at a valuation of $1.5bn with a series of blue-chip investors including Atomico, Blackrock, and Kinnevik. Its previous raise was at the peak of the market in December 2021 with a Series E of $500m at a valuation of $2.35bn. The funds in this round will be used for international expansion and to accelerate product development in AI-powered features and automation. Job&Talent is developing a suite of AI agents, each designed to simplify a specific aspect of workforce management using operational data from over one million worker placements and millions of logged shifts across the platform. The first is a recruitment agent, Clara which in its first few months of operation has conducted over 180,000 interviews, equivalent to the output of thousands of recruiters, directly contributing to more than 7,000 hires.

Swiss biotech Granite Bio raised $100m in a deal led by Versant Ventures, Novartis Venture Fund, Forbion and Sanofi Ventures. Granite is focused on targeting multiple autoimmune diseases.

After four months of the year the development of the market has been encouraging with the total amount of money raised for growth stage business at $13.6bn, 19% ahead of 2024 and 67% ahead of 2023 at the same stage. The sector diversity of the raises is greater than in the US, notably marked by much less emphasis on pure AI businesses.

The next chart shows that the top five sectors in Europe have accounted for 63% of the funds raised ytd with AI in fifth position.

Ytd software remains the biggest sector both by volume and value with 39 raises for a total of $2.3bn led by $200m for the travel software platform TravelPerk and $175m for the decision intelligence business, Quantexa.

Fintech has sustained the revival seen towards the back end of 2024 and is in second place by both volume and value with 32 rounds raising $2.1bn, the biggest being the $500m raised for Israeli international payments platform, Rapyd.

Biotech deals remain prominent with 21 deals raising a total of $1.6bn. Verdiva Bio announced what it dubbed ‘an oversubscribed Series A’ of $411m, co-led by Forbion and General Atlantic in one of Europe’s largest ever Series A rounds...

Climate Tech deals remain relatively subdued with the value of raises after four months being $1.35bn. It was the leading sector in 2023 and 2024 but investor appetite for larger deals in long duration, high set up cost businesses has faded post the difficulties at Northvolt and so the type of big raise seen at the likes of Northvolt, H2GreenSteel , Verkor and Zenobe in 2022 and 2023 have been largely absent since mid-2024. The biggest raise in ClimateTech ytd has been the $420m for green flexibility, a German developer of large-scale battery storage systems led by Partners Group. A complementary debt financing package meant that the total funds raised were in excess of €1bn.

Europe - $13.6bn raised in YTD to end April – 19% ahead of 2024, 67% ahead of 2023

Source: Rothschild & Co

Source: Rothschild & Co

Europe - $2.4bn of raises in April 2025

Source: Rothschild & Co

Source: Rothschild & Co

Still a robust pipeline: The long timescale of venture and growth equity raises means that the flow of announced deals is likely not a particularly good indicator of the state of confidence in the market post the tariff turmoil caused by the Liberation Day announcements on April 2nd. Any impact is likely to take a few months to be reflected in the numbers.

The next Exhibit shows that impending raises in growth equity – drawn from press reports – appear to total c$30bn, mainly in the US. This is strongly up on the c$16.5bn in impending raises we reported on last month. There are a number of interesting additions to this list.

The first to consider though is not an addition. The prospective size and valuation of the raise for Elon Musk’s xAI appears to have gone up in the last month. The company had been reported as seeking a further $10bn from investors at a valuation of $75bn. More recent reports put the putative fund raiser at $20bn and the valuation at $120bn, potentially a marker of the continued appetite for AI LLM deals.

Anther Elon Musk company, Neuralink, is planning to raise $500m at a pre-money valuation of $8.5bn. The company was valued at $3.5bn in its Series D in August 2023 led by Peter Thiel’s Founders Fund. Neuralink is developing custom chips for use as brain implants for the treatment of paralysis and associated conditions.

Sesame AI’s AI assistants use the company’s new Conversational Speech Model (CSM). Its male and female voice assistants, ‘Miles’ and ‘Maya,’ are reported to have more natural and emotionally resonant conversations than current AI chatbots. The company is reported to be looking to raise $200m led by Sequoia and Thrive Capital.

Also in the US Agility Robotics, which produces the Digit bipedal humanoid warehouse robot, is reportedly raising $400m in new funding at a pre-money valuation of $1.75bn with WP Global and SoftBank said to be leading.

A big impending raise in the UK is that for AI hyperscaler Nscale which emerged from stealth in May 2024 and in December raised $155m in a Series A led by Sanditon Capital to accelerate its AI infrastructure expansion across Europe and North America. Nscale develops sustainable AI-ready data centres, deploying massive-scale GPU infrastructure to deliver a range (bare metal, Kubernetes etc) of high-performance AI cloud services. Nscale is launching a public cloud service in early 2025 allowing developers access to purpose-built inference and training solutions.

Bloomberg now reports that Nscale is looking for an additional US$1.8bn of financing in a private credit deal led by Goldman Sachs as well as another $900m in preferred equity and convertible shares.

Growth Equity – c$30bn in reported upcoming raises

Source: Rothschild & Co; press reports

Source: Rothschild & Co; press reports

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts has led to increased optimism and enthusiasm for growth equity in 2025. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment led to a sharp impact on valuations in private markets. The scale of the fall in the FTSE Venture Capital Index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Outside the AI space the VC market is regaining confidence with a revival of interest in fintech, biotech and software being notable. Certain investors remain very active in the space with substantial funds to deploy. There remains substantial dry powder in the VC industry.

- The speed of the investment process has slowed since 2021-22. The level of diligence on new deals has stepped up.

- 2023 and 2024 saw more down rounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- Recent initiatives by the US to impose tariffs on its trading partners is likely to impact US and global economic growth and to negatively affect the fund-raising environment for venture backed companies.

- It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and on DCF and comparative based multiples.

Read the previous editions:

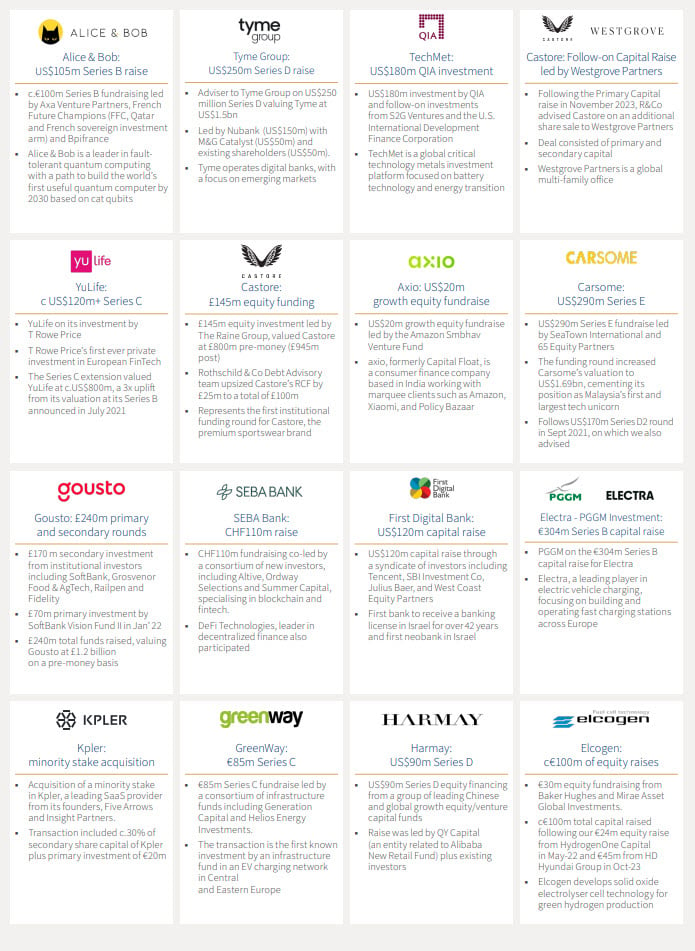

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Thomas Chung

Head of Private Capital, North America

thomas.chung@rothschildandco.com

+1 212 403 5559

+1 917 594 7208

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.