Preparing for life after the firm

Background

Our client works for a US-based private equity firm in London. He is a founding partner of the London office, married in his mid-50s with three adult children.

Key objectives

He wanted to simplify his finances by putting a plan in place for the carried interest he was due to receive over the next five years, balancing his exposure to PE whilst planning for retirement. Supporting his children with property purchases was a priority, and he wanted to leave a meaningful legacy for his family and charity.

Understanding our client

Our client held discretionary investments and a number of private equity vintages in different stages of commitment. We started by helping them categorise and consider the risk, return and liquidity profiles of his assets using our ‘Wealth Framework‘. We used our cashflow planning tool to review our client's short-term requirements, longer-term retirement objectives and carried interest plans – making sure to account for capital calls being due in USD. Our cashflow planning presented a range of different financial scenarios, which were projected against his age and retirement location, with various inflation and return assumptions.

Solutions and options

Once we had a clear vision of our client's circumstances, we were able to offer tailored solutions to help. As he still had five-to-seven years of income and carry, we built a number of cashflow planning models to show the impact of different investment contributions, timing of gifts to their children, and charitable donations.

In reviewing the risk and return levels across their asset base, we compared our investments to his current arrangements. He appreciated our ‘bottom up’ approach which he felt aligned to his firms PE approach. Following this, we consolidated their investments into our balanced strategy, to provide them with a balanced, liquid nest egg to de-risk their more illiquid PE investments.

To assist with their shorter-term expenditure, liquidity and capital call requirements, we set up a proactively managed cash management strategy across gilt portfolios (tax efficient for UK taxpayers), liquidity funds and deposit accounts.

For additional peace of mind, we arranged a lending facility secured against his portfolio, which can be used for additional liquidity. The facility is free to arrange and can be drawn in different currencies (e.g. GBP, USD, CHF).

Day to day, support our client beyond their investments by:

- Coordinating with his accountant for amounts required to cover tax bills and allocated the amount to gilts

- Recording private equity commitments, with cash held in GBP & USD to cover 12 months

- Managing currency and foreign exchange for capital calls at pre-agreed rates

- Sending capital calls from his accounts to help save time and administration

Tax efficiency was important to them. The client was pleased to be able to invest in one of our structures, which are efficient when accumulating wealth and drawing income. Whilst invested, client portfolios don't incur

annual capital gains tax and they are efficient in reducing clients’ taxable dividend yield. They are also domiciled offshore which can provide flexibility if retiring overseas and are scalable to take account of contributions.

We also introduced him to David Kilshaw, Head of Private Client Wealth Solutions, to discuss different options available to his family in the future such as trusts and charitable foundations.

Outcome

Our client is happy that he has a plan in place for his family's current and future financial needs and comforted by the cashflow models, which have helped better frame the timing and impact of future commitments.

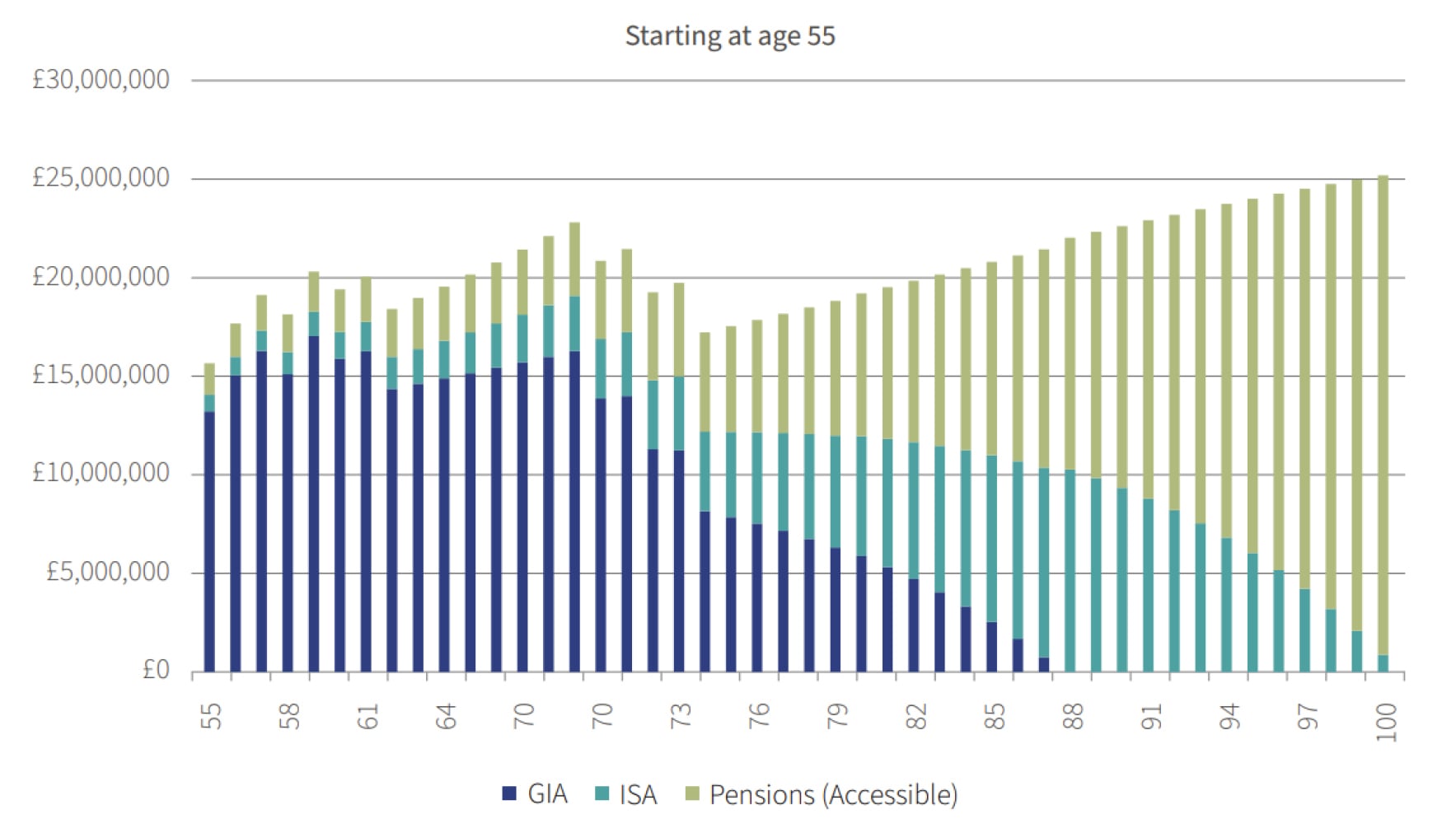

Cashflow modelling for a Private Equity Partner

| Assumptions | GIA | ISAs | Pensions (Accessible) |

| Starting value (age 55) | £12,000,000 | £750,000 | £1,500,000 |

| Performance (balance for illustration) | 6.24% | 6.24% | 6.24% |

| Inflation | 2.00% | 2.00% | 2.00% |

Source: Rothschild & Co, Bloomberg Data from 31 December 2002 to 31 December 2024.

The New Court Fund GBP inception date was 14 July 2015. Performance for periods prior to inception date is the Rothschild & Co Wealth Management UK Ltd GBP Balanced composite, adjusted to reflect the fund's 1% annual management charge and 0.06% operational costs. Performance data is net of fees. Data post 30 September 2007 is net of actual client fees incurred. Data prior is actual gross performance less current average client fees.

Past performance is not a reliable indicator of future performance and the value of investments and the income from them can fall as well as rise.

The above graphs are for illustrative purposes only. The information above is not intended and should not be construed as tax advice. Each investor should seek their own independent tax advice