Approaching retirement as a corporate executive

Background

Our client is the former CEO of a global company listed in the UK. He is married with adult children, who are starting families of their own.

When first introduced to Rothschild & Co Wealth Management, the client was approaching retirement, having built considerable wealth during more than 30 years as a high-earning corporate executive. Much of this wealth was concentrated in company shares, alongside sizeable cash reserves in low-yielding accounts and properties in the UK and abroad.

Asset rich but time poor, he acknowledged that financial planning had taken a back seat but was now keen to put a clear strategy in place.

Key objectives

Our client’s overriding goal was for him and his wife to remain financially comfortable and never have to worry about money. Beyond this, he wanted to diversify his wealth by reducing reliance on company shares and putting surplus cash to work in assets with stronger long-term potential.

Looking further ahead, the aim was to preserve and grow wealth ahead of inflation, creating a reliable nest egg to draw upon in later years if needed. He was also keen to pass on wealth efficiently to his children and grandchildren, while keeping the overall plan as simple as possible.

How we helped

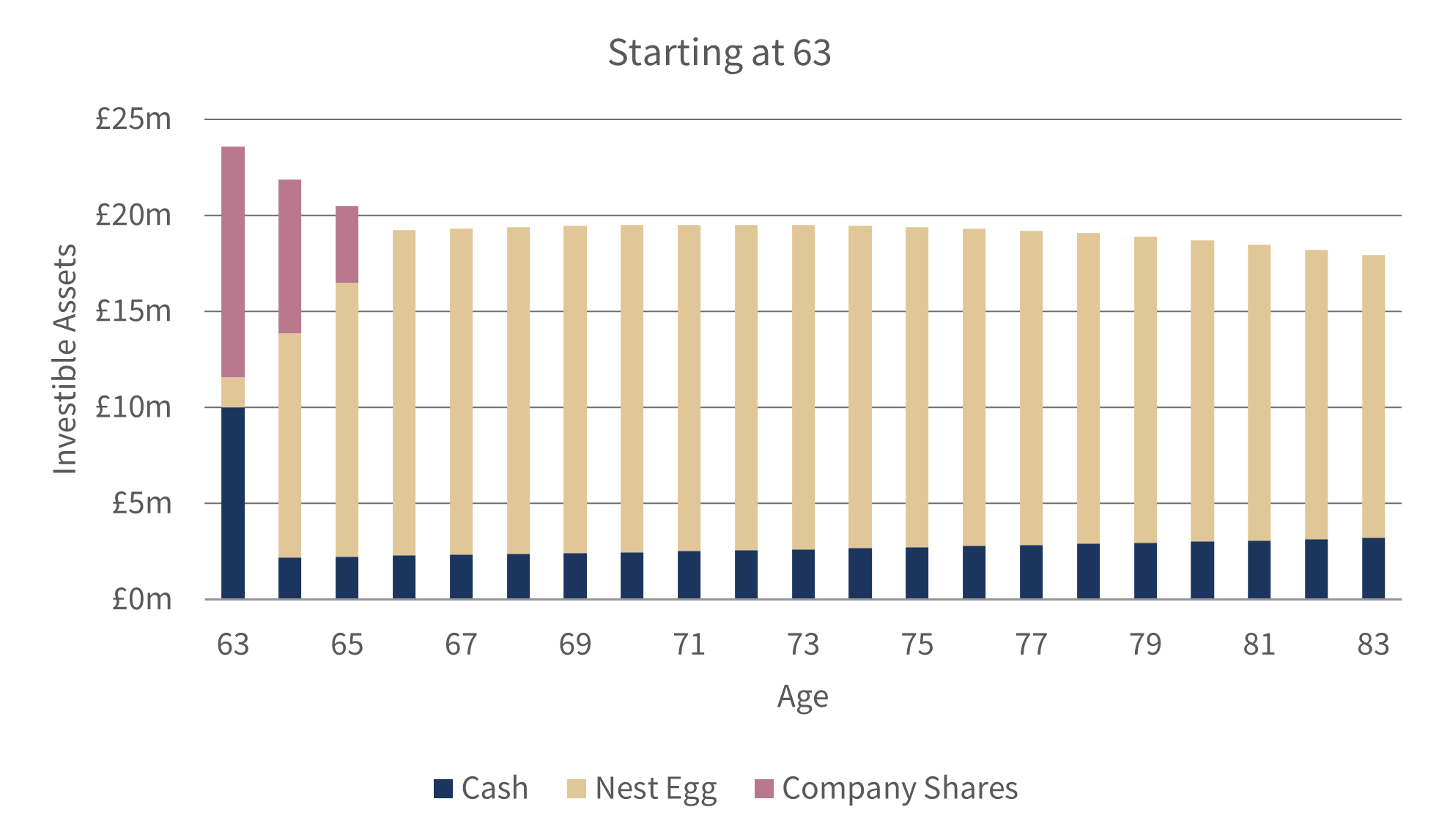

We worked with our client to draw up a structured plan for selling his company shares, setting clear parameters and providing custody throughout the process.

Using our wealth framework and cashflow modelling, we clarified how much should be set aside in cash reserves and how the remaining capital could be invested over longer horizons to target higher returns. By modelling different risk profiles and potential outcomes, he was able to identify the level of risk he felt comfortable taking with his nest egg.

Our Head of Wealth Solutions also explored succession planning with him, drawing on examples of how other families balance supporting children while encouraging independence. He was particularly interested in the role of trusts and family investment companies, as well as the inheritance tax planning opportunities available. We then introduced him to specialist tax advisers, who helped put in place an appropriate structure for his family.

Ahead of the October 2024 Budget, and in collaboration with those advisers, part of his nest egg portfolio was gifted to his children, who are now clients of Rothschild & Co in their own right.

Outcome

Our client now has a robust long-term financial plan, giving him the reassurance he sought for his family’s future. With Rothschild & Co managing his investments, he now feels confident even during market volatility.

Semi-annual reviews keep the strategy aligned with his objectives and, importantly, the plan remains flexible should our client’s circumstances or requirements change.

Cashflow modelling

Source: Rothschild & Co, Bloomberg Data from 31 December 2002 to 30 June 2025.

The New Court Fund GBP inception date was 14 July 2015. Performance for periods prior to inception date is the Rothschild & Co Wealth Management UK Ltd GBP Balanced composite, adjusted to reflect the fund's 1% annual management charge and 0.06% operational costs. Performance data is net of fees. Data post 30 September 2007 is net of actual client fees incurred. Data prior is actual gross performance less current average client fees.

Past performance is not a reliable indicator of future performance and the value of investments and the income from them can fall as well as rise.

The above graphs are for illustrative purposes only. The information above is not intended and should not be construed as tax advice. Each investor should seek their own independent tax advice.