Accumulating assets as a corporate executive

Background

Our client is a 56-year-old CEO of a FTSE 250 company, married with two adult children aged 18 and 19.

When our client was introduced to Rothschild & Co, he was looking for professional wealth management to streamline his financial affairs and free up personal time. With a successful corporate career to date, he had accumulated significant cash reserves, multiple pension pots and residential properties.

Key objectives

Our client did not plan to retire for some years and was ready to take a more structured approach to financial planning as he continued to accumulate wealth.

Establishing a comprehensive, strategic view of his balance sheet was a priority, and he wanted to ensure that his surplus cash was directed into investments designed for long-term growth. He also sought to review, simplify and consolidate his many pension pots.

Looking ahead to the next generation, the client was keen update his will and start building investment portfolios for his children through structured gifting. More broadly, he aimed to reduce the amount of time he spent managing his personal finances.

How we helped

Using our Wealth Framework, we helped our client categorise his assets into distinct 'pots', providing clarity across his balance sheet and identifying areas for action.

As a result, our client decided on a suitable strategic cash reserve that would allow him to sleep easy at night and ring fence funds required for an upcoming tax bill and the repayment of his outstanding mortgage. We also guided him on how much to allocate to long-term nest egg investments that would be held jointly with his wife.

Following a discussion around risk and return, the client chose one of our medium-risk strategies targeting a long-term return of inflation + 3%, with investment being made through one of our tax-efficient investment structures.

We set aside an amount that would be gifted to his children to start their investment portfolios with Rothschild & Co. Given our client’s high income levels, the most suitable approach was a monthly standing order to keep building his children’s investment portfolios out of excess income. Using our cashflow modelling, we were able to help the client start considering future larger gifts to his children to help them get onto the property ladder. In addition, annual ISA subscriptions were arranged for all four family members.

To simplify his retirement planning and establish a clear investment strategy, we consolidated his pensions into a Self-Invested Personal Pension. For these assets, he chose a higher-risk approach designed to deliver inflation +4% over time.

Through Rothschild & Co’s well-established professional advisor network, we were also able to introduce our client to private client lawyers who could help him update his will.

Outcome

The client and his family now benefit from a robust, long-term financial plan. With Rothschild & Co managing our client’s investments, he has reclaimed valuable personal time and feels confident in the face of market volatility. Regular semi-annual reviews ensure his strategy remains aligned with the evolving goals of his family.

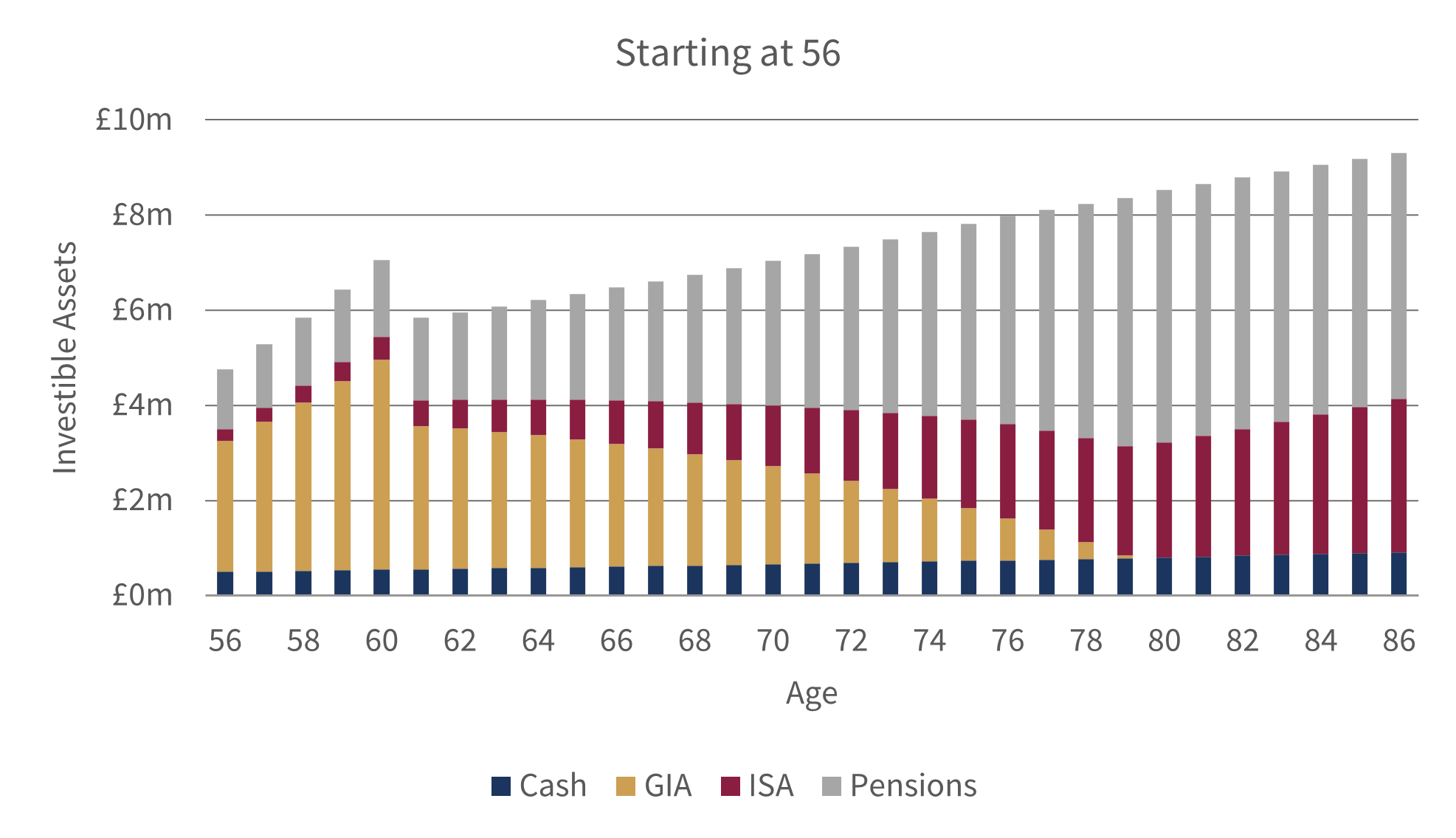

Cashflow modelling

| Assumptions | Cash | GIA | ISAs | Pensions |

| Starting Value (Age 56) | £500,000 | £2,750,000 | £250,000 | £1,250,000 |

| Performance | 2.00% | 5.00% | 5.00% | 6.00% |

| Inflation | 2.00% | 2.00% | 2.00% |

2.00% |

Source: Rothschild & Co, Bloomberg Data from 31 December 2002 to 30 June 2025.

The New Court Fund GBP inception date was 14 July 2015. Performance for periods prior to inception date is the Rothschild & Co Wealth Management UK Ltd GBP Balanced composite, adjusted to reflect the fund's 1% annual management charge and 0.06% operational costs. Performance data is net of fees. Data post 30 September 2007 is net of actual client fees incurred. Data prior is actual gross performance less current average client fees.

Past performance is not a reliable indicator of future performance and the value of investments and the income from them can fall as well as rise.

The above graphs are for illustrative purposes only. The information above is not intended and should not be construed as tax advice. Each investor should seek their own independent tax advice