Preparing for life after the firm

Background

Our client is a partner at a US consultancy firm in London. He is married with two school-aged children. He plans to continue working for 5-8 more years.

Key objectives

Our client wanted to know how and when he could afford to retire whilst continuing to co-invest in private equity opportunities through his firm. He also wanted to set aside funds to support his children to go to university in the US.

How we helped

We started by helping our client categorise and consider the risk and return profiles of his assets using our ‘Wealth Framework‘, which mapped out as follows (see table below). Our client had already built a strong financial foundation by paying off the mortgages on his properties and having a good mix of assets across different ‘pots’.

| Lifestyle | Cash | Nest egg | Growth | Firm |

| £2m primary residence (mortgage free) | £300k | c.£2m across pension, ISA and GIA | ~$1m in committed private assets ($300k already funded) | $500k partnership equity |

Solutions and options

As our client still had 5-8 years of earning potential of £2m annual compensation, we built a number of cashflow planning models to show the impact of different-sized regular contributions to his Nest Egg. We settled on £500,000 annual contributions up to his intended retirement.

We set aside sums for American university fees for his children, and for capital calls for private equity arrangements - allocating these to a range of deposit accounts and gilts, which we proactively manage for him to balance returns and liquidity. For additional peace of mind, we arranged a lending facility secured against his investments with us, for any unexpected capital calls.

As we look to growing and protecting our client’s wealth over the long-term, we continued to build up their Nest Egg whilst balancing his requirement for large expected future commitments for US university fees.

Our client appreciated our ‘bottom up’ investment approach as it aligned with his private equity investments. We therefore consolidated his non-private equity holdings into our balanced strategy. He invested within one of our tax-efficient investment structures that is domiciled offshore and provides flexibility should he choose to retire overseas in the future.

With a long-term plan in place to continue to build his family’s wealth, we were able to start a discussion on how to then consider passing those assets down to his children (e.g. factoring in an intended gift for house purchases, trusts or family investment companies) and the timing of these.

Outcome

As a result, our client now feels like he has a much better understanding of his plan to retire and aims to diversify the risk of his private assets by investing further in his family’s Nest Egg. He has a plan for future American university fee commitments and he values our proactive engagement as well as the structure of the plan that’s been put in place, which we meet regularly to review.

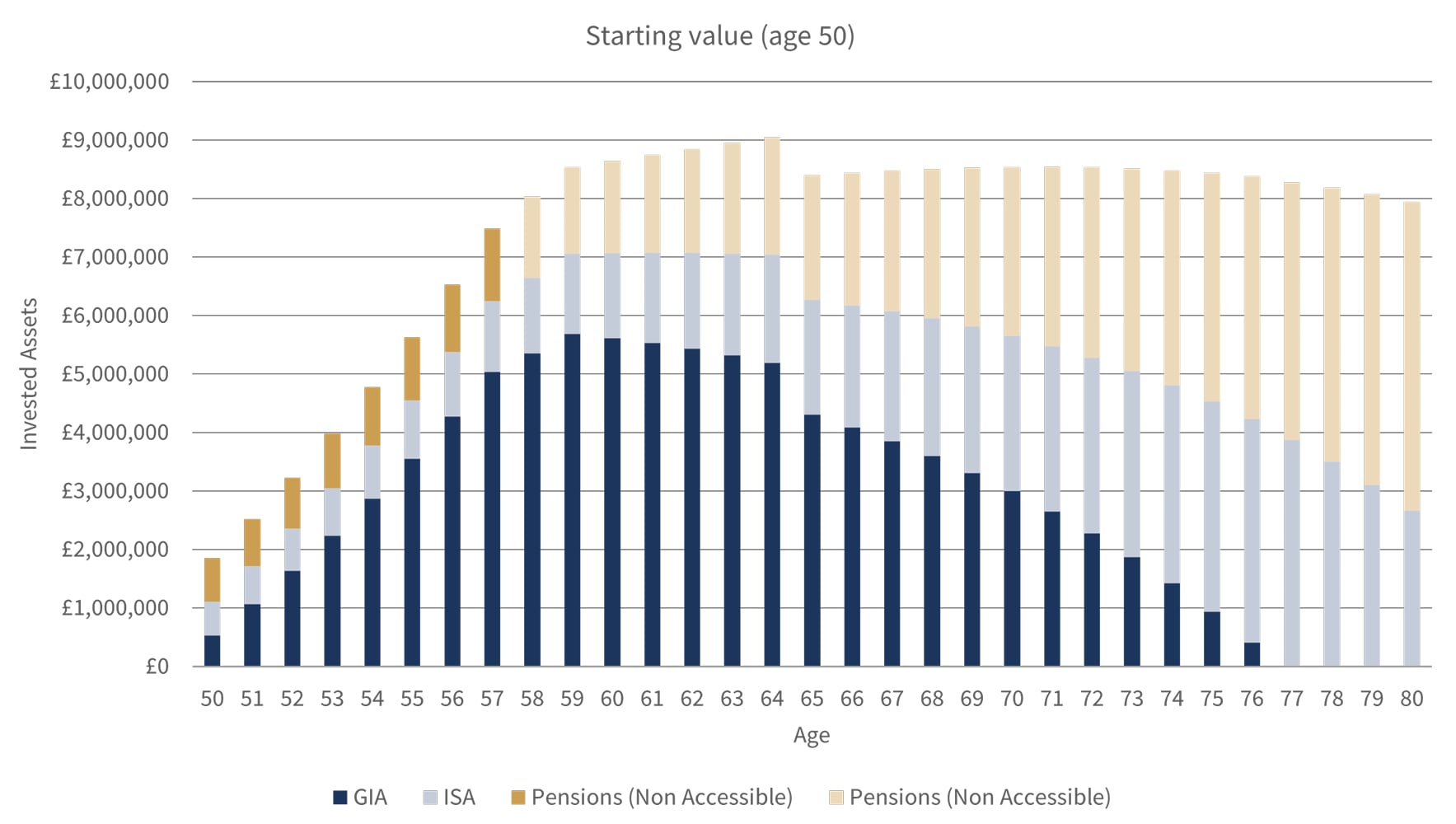

Cashflow modelling for a US Consultancy Partner

| Assumptions | GIA | ISAs | Pensions (Non accessible) | Pensions (Accessible) |

| Starting value (age 50) | £500,000 | £500,000 | £700,000 | £0 |

| Performance (balance for illustration) | 6.24% | 6.24% | 6.24% | 6.24% |

| Inflation | 2.00% | 2.00% | 2.00% | 2.00% |

Source: Rothschild & Co, Bloomberg Data from 31 December 2002 to 31 December 2024.

The New Court Fund GBP inception date was 14 July 2015. Performance for periods prior to inception date is the Rothschild & Co Wealth Management UK Ltd GBP Balanced composite, adjusted to reflect the fund's 1% annual management charge and 0.06% operational costs. Performance data is net of fees. Data post 30 September 2007 is net of actual client fees incurred. Data prior is actual gross performance less current average client fees.

Past performance is not a reliable indicator of future performance and the value of investments and the income from them can fall as well as rise.

The above graphs are for illustrative purposes only. The information above is not intended and should not be construed as tax advice. Each investor should seek their own independent tax advice