Growth Equity Update

July 2025 – Edition 40

- US growth equity storms ahead in H1: The value of fundraises of $100m+ for US VC companies increased 2.6x yoy to $121bn in H1 2025 vs $46bn in H1 2024 and is already ahead of the 2024 full year total of $111bn

- AI leads the way: Boosted by the $40bn raise for OpenAI and the $14.3bn for Scale AI 62% of H1 funds raised in the US were for AI businesses

- Europe’s steady progress: The R&Co Deal Monitor indicates that European VC raises of $20m+ saw a solid 23% yoy advance in value. There were 56 deals of $100m + in H1 (vs 45 in H1 2024) and four deals of $500m + (vs 3 in 2024)

- Exit activity picking up: Pitchbook sees total US H1 VC exit value up 51% yoy at $120bn versus $151bn for the whole of 2024, with exit value via M&A at $55.9bn (+39%), via buy outs at $19.7bn (+101%) and public listings at $44.4bn (+53%)

- VC funds raised still subdued: Pitchbook figures indicate $26.6bn raised by US funds in H1 versus annual totals of $98bn/ $81bn in 2023/4. In Europe H1 funds raised were €5.2bn versus annual figures of €23.1bn/€22.3bn in 2023/4

- Public markets shrug off fears: Despite the geopolitical (Ukraine, Israel, Iran) and economic (Liberation Day) turmoil, both the S&P 500 and the Euro STOXX 600 finished H1 up 6% in local currency terms. The 9th of July deadline of the US’s 90-day tariff suspension has passed without further major upset

- British Business Bank - Bigger and leader: As part of its growth initiatives the UK government is making key changes at the British Business Bank. Its total financial capacity is increased to £25.6bn; it will invest greater amounts in companies through direct investments; it will be able to lead investment rounds and make strategic investments of up to £60m in UK growth companies. We review the changes

- Growth is the only evidence of life – John Henry Newman

Click here to download a PDF version of Growth Equity Update

Growth Equity raises- strong H1 2025

The US 2025 H1 value total of $121bn is already ahead of the $111bn raised in the whole of 2024. Europe is up 23% yoy by value in H1.

In the January edition of the Growth Equity Update we made a series of predictions for the growth equity market in 2025. Two of the key ones were:

Venture capital activity to grow again in 2025: After two years of decline global VC activity grew in 2024 over 2023. Global funding for VC firms increased by 5% from $349bn in 2023 to $368bn in 2024. We think that VC deal value will rise again in 2025 …We do not expect a growth bonanza- the AI raises of 2024 have set a tough comp- but we do expect another year of solid growth in 2025.

Artificial Intelligence to dominate and widen: A two-tier market has emerged in venture capital. It is AI, and then everything else. AI captured around a third of all new VC funding in 2024…These deals, and the rapid valuation uplifts between rounds, have only stoked the appetite of investors for exposure to the potential industry transformations that the application of AI offers. We expect that the net will widen in 2025 and that a broader range of investors will seek to gain exposure to AI amongst application specific businesses.

We can debate how radical these predictions were but the evidence of H1 2025 suggests that they are on track.

US VC – H1 2.6x value increase: The two factors are best expressed by the US market. Our R&Co Deal monitor, which tracks Growth Equity/VC deals of $100m + in the US, indicates that fundraising for US based VC companies has increased by 2.6x ytd. By the end of June $121bn had been raised for companies, outstripping the $46bn to the end of June 2024.

US H1 2025 total of $121bn exceeds the $111bn full year 2025 total: Indeed the 2025 half year total at $121bn is already ahead of the $111bn raised in the whole of 2024.

Top 20 US deals in H1 2025 raise $83.5bn

Almost 70% of the value of the H1 US deals were in the top 20 raises. Indeed, a third of the value was in just one raise, the $40bn funding round for OpenAI in March which valued the company at $300bn. Ten of the top 20 raises were for AI businesses.

AI leads the way

There were 33 raises of $100m or more for US AI businesses in H1 2025 raising $75bn, making it the largest single sector for fundraising, absorbing 62% of total funds raised in H1 up from around a third in the whole of 2024. The LLM providers were well represented with OpenAI ($40bn), xAI ($5bn), Anthropic (two raises totalling $4.5bn) and Sandbox AQ ($450m) all represented.

Notably there were two big AI ‘talent unicorn’ raises in H1 2025. These are substantial raises backing founders and their teams. These are pre-revenue and pre-product companies that have assembled high reputation teams, but which have only given an outline of the AI related fields in which they intend to operate.

In April Safe Superintelligence raised $2bn at a valuation of $32bn. It was founded in 2024 by the former chief scientist at OpenAI, Ilya Sutskever, and its concept is that it creates superintelligent AI that is safe for humanity. The company is pre-product, being yet solely focused on foundational research, although it is believed to be considering applications in healthcare and education.

In June Thinking Machines Lab, a six-month-old company founded by the former CTO of OpenAI, Mira Murati raised $2bn at a valuation of $10bn. It too is pre-revenue and pre-product and is working on making “AI systems more widely understood, customisable and generally capable.’

Elsewhere application specific AI raises, typically smaller in value, are becoming more common. Runway which is developing a range of generative AI models for media production, including video-generating models, raised $308m at a $3bn valuation. Harvey which offers automation for legal work raised $300m at a $5bn valuation just four months after a $300m Series D valuing it at $3bn. In healthcare, Abridge AI has a transformational virtual medical note taking technology for physicians – it raised $300m at a $5.3bn valuation. Also in healthcare, Hippocratic AI is building a large language model specifically for healthcare use cases. It raised $141m from Kleiner Perkins and others.

AI infrastructure remains a prominent field for VC funds with Together AI – which helps run and fine tune AI models with easy- to -use APIs raising $305m at a $3.3bn valuation; Turing, which trains frontier models to allow enterprises to turn them into production-ready systems raising $111m and Nexthop AI raising $110m for its service in building efficient Al infrastructure for large cloud operators.

US AI businesses raise $75bn in H1 2025

The sector hierarchy for US growth equity fundraising in H1 2025 is indicated in the next Exhibit. After AI the other big US sectors for fundraising in H1 were Software at $6.7bn, Biotech at $5.7bn, Fintech at $4.7bn, ClimateTech and Defense Tech both at $3.7bn, followed by Cybersecurity ($3.3bn) and Metaverse, a single raise of $3bn.

The top US VC raises by industry sector – H1 2025

In software notable raises include the $500m Series C by Nerdio in March led by General Atlantic. Nerdio is a platform designed to simplify how companies deploy and manage Microsoft cloud technologies. The raise pushed the company’s valuation north of $1bn. The company reported in June that ARR had exceeded $100m for the first time. Fleetio, a fleet automation software business, raised $450m in March to enable the acquisition of Auto Integrate, a fleet maintenance platform, giving the combined business a valuation of $1.5bn in a deal led by Elephant and Goldman Sachs Alternatives. Rippling, the HR tech platform offers a range of products including payroll and benefits, SSO and identity management, bill pay, and corporate cards. It raised a $450 million Series G round at a $16.8bn valuation in May. Its ARR – according to a mid-May post on X, is $570m, up from $350m at end 2023, implying a near 29x ARR multiple.

In Biotech Retro Biosciences raised a $1bn Series A in January for its work on anti-ageing, age related diseases and conditions. A notable investor in the round was OpenAI’s Sam Altman. Pathos AI describes itself as an AI powered biotech and raised a $365m Series D in May to fund trials of solid tumour drugs. Eikon Therapeutics’ $350m February Series D to fund cancer therapies brought its total raised since 2021 to $1.1bn.

Fintech continues its recent revival with the most notable raise in H1 being the $2.1bn by Acrisure led by Bain Capital. It valued the business, whose services include insurance, reinsurance, cybersecurity, real estate, payroll, benefits, and wealth management solutions, at $32bn. Plaid’s APIs connect consumer bank accounts to popular finance apps. Its $575m secondary round in April valued the company at $6bn, down from a peak of $13.4bn in 2021 at the height of the market. The company grew sales c25% to the ‘high three hundred millions’ in 2024 and it projects c$430m for 2025, implying a sales multiple of c14x.

The biggest US deal in Climate Tech in H1 was AI related. In May Commonwealth Fusion Systems raised a $1bn Series B2. The unnamed lead investor was identified as a hyperscaler developer. It is known that Microsoft and Google both contributed to previous rounds. The company has targeted having two 400MW fusion reactors in operation by the first part of the 2030s. The ability to build a workable fusion power commercial energy source remains a major technical challenge. In June, the nuclear technology company TerraPower raised $650m. The company was founded by Bill Gates, who serves as its chairman, and the capital raised will be used for the construction of its first Natrium plant, which would be the first commercial advanced nuclear power facility in the US. Backers in this round included the venture capital arm of NVIDIA.

We have previously touched on the resurgence of Defense as a focus for VC investors. Anduril offers a range of autonomous defence systems, and the AI based software that controls them. In June, the company raised $2.5bn in a Series G which valued it at $30.5bn, twice the valuation of its previous round. Revenues in 2024 doubled to $1bn. H1 also saw a $250m raise for Epirus which provides technology to counter drone swarms. Its Leonidas system uses high-powered electromagnetic pulses to target drones as it moves across the battlefield.

Finally, H1 2025 is notable for a modest revival in blockchain and crypto deals. There were six deals raising a total of $775m in H1. These were led by a $153m Series C in April for Auradine which specializes in equipment for AI data centres and bitcoin mining.

Europe – 23% yoy value growth in H1 2025

Europe’s funding for VC companies was up solidly year on year in H1 with a 23% value advance to $21.8bn (H1 2024 $17.7bn). There were 56 deals of $100m + in H1 (vs 45 in H1 2024) and four deals of $500m + (vs 3 in 2024).

AI is a less dominant theme in Europe. The top five categories in H1 2025 in Europe were Software, AI, Fintech, Biotech and Climate Tech in that order.

In software there were 63 deals of more than $20m in H1 raising $3.18bn, led by $260m for the medical education and clinical decision-making business AMBOSS, $200m for the travel software platform TravelPerk and $175m for the decision intelligence business, Quantexa.

There were 21 raises in AI totalling just short of $3bn. The largest raise was the $690m for the AI driven defense business Helsing. In March Isomorphic Labs raised $600m in its first external funding round led by Thrive Capital, with participation from GV and Alphabet. The company has developed a number of AI models that form its unified AI drug design engine that works across multiple therapeutic areas. In May Israeli business AI21 Labs raised a $300m Series D from Google and Nvidia. AI21 develops LLMs and natural language processing tools and is best known for its language models, notably the Jamba series, which enhances long-context understanding and enterprise-grade applications

Fintech has sustained the revival seen towards the back end of 2024 with 32 rounds raising $2.7bn in H1 2025.The biggest was the $500m raise by the Israeli international payments’ platform, Rapyd. This coincided with the finalisation of its $610m purchase of PayU from Prosus, originally announced in August 2023. The deal valued Rapyd at c$4.5bn, down from the $10bn mark the company hit at its peak in 2021. Dojo is a payment provider focused on SMEs in the UK. The familiar Dojo card machines’ secret weapon is that settlement to the SME takes place next day -a key attraction for small businesses. The company raised a $190m funding round with Vitruvian Partners. Scalable Capital, a German business providing a digital platform for retail investors, raised $175m in a round led by Sofina and Noteus Partners.

Biotech deals remain prominent with 35 deals raising a total of $2.7bn. Verdiva Bio announced ‘an oversubscribed Series A’ of $411m, co-led by Forbion and General Atlantic in one of Europe’s largest ever Series A rounds. Verdiva acquired the development rights of a pipeline of assets from Chinese biotech Sciwind Biosciences in 2024 including an oral-based – rather than the more common injection based - GLP-1 anti-obesity drug.

Climate Tech deals are at $2.1bn across 35 deals at the end of H1 with the biggest raise being $420m for green flexibility, a German developer of large-scale battery storage systems led by Partners Group. May saw a $330m raise for sustainable aviation fuel business, Skynrg. In June Proxima Fusion raised $145m from Cherry Partners and Balderton Capital. The business is a spin out from the Max Planck Institute to build fusion power plants using QI-HTS stellarators

A couple of interesting sectors moving up the funding charts. The increased focus on European defence sovereignty in recent months has Quantum Systems CEO Florian Siebel stating that ‘The need for sovereign, aerial intelligence has never been more pressing.’ May saw a $176m round for the German business led by Balderton Capital, Hensoldt and Airbus. Quantum Systems is an ‘aerial data intelligence company that provides multi-sensor data collection products to government agencies and commercial customers.' It is a dual use business with commercial as well as defence applications with government contracts in the US, the Ukraine, Germany, Spain, Australia, and Colombia. The business had revenue of c€115m in 2024 and cites 100% yoy revenue growth.

The same trend has been reflected in recent raises for the likes of drone manufacturer Tekever and battlefield operating software business, KELA Technologies. Overall defense companies raised $343m across four deals in H1 2025 – a figure that would rise to $1.03bn if we included the Helsing raise in this category.

Blockchain and crypto raises are also becoming more common. There were six such deals for a total of $291m in H1 in Europe.

European VC raises up 21% yoy in H1 2025 – Software and AI lead the way

How does Pitchbook see it?

We check our R&Co Deal Monitor findings against the data from Pitchbook.

Pitchbook reflects the sharp upturn in US deal activity in the last three quarters with the value of deals close to the peak levels of 2021. In H1 2025 it identifies $163bn of total US VC deal value, up 1.75x over the $92.7bn of H1 2024

US VC deal activity by quarter

Pitchbook’s numbers show the surge in AI deals in H1 2025, led by the $40bn raise by OpenAI. It identifies $104bn of deal value in AI to the end of June, equivalent to the figure for the whole of 2024. AI absorbed 64% of US deal value in H1 2024, up from annual figures of 49% in 2024 and 38% in 2023

US AI & ML VC deal activity

The value of European deal activity is displayed in the next chart. Pitchbook has this at €29.2bn in H1 2025, down 6% from €31.2bn in H1 2024.

European VC deal activity by quarter

Fundraising by VCs remains subdued on both sides of the Atlantic. The Pitchbook figures indicate $26.6bn of funds raised in the US in H1 which compares with annual totals of $98bn in 2023 and $81bn in 2024. In Europe funds raised are identified by Pitchbook at €5.2bn versus annual figures of €23.1bn/€22.3 in 2023/4.

US VC fundraising activity

The pace of exit activity is subdued by historic standards but has picked up as a trickle of IPOs has supplemented increasing M&A activity. Pitchbook sees total US H1 VC exit value at $120bn versus $151bn for the whole of 2024.

It sees exit value via M&A activity at $55.9bn versus $40.2bn in H1 2024 (+39%), exits via buy outs at $19.7bn vs $9.8bn (+101%) and exist via public listings at $44.4bn versus $29bn (+53%) with the overall H1 total up 51%.

In Europe H1 exits are seen by Pitchbook down 9% yoy at €26.8bn versus $29.4bn in H1 2024. IPO exits were the culprit, at €3.6bn versus €11.1bn, with buy outs (€6.9bn vs €5bn) and M&A (€16.3 vs €13.3bn) both up yoy.

Quarterly US exit value ($bn) by type

Beefing up the mandate of the British Business Bank

As part of the UK government’s growth initiatives, some key changes at the British Business Bank. Its total financial capacity will be increased to £25.6bn; it will be able to invest greater amounts in companies through direct investments; it will be able to lead future investment rounds and make strategic large investments of up to £60m in UK growth and innovation companies.

In recent editions of the Growth Equity Update we have focused on the UK government’s Mansion House Accord and its attempts to stimulate growth in the UK by encouraging UK pension providers to invest more of their funds in private UK assets. Announced on May 13 the Mansion House Accord has seventeen of the UK’s largest workplace pension providers pledging to invest 10% of their DC default funds in private assets. The simultaneous Pensions Investment Review supports the process by addressing issues such as value for money.

In the June update we looked at the French government’s Tibi scheme to promote private asset investment and at the role of Bpifrance, France’s public investment bank whose role is to support French businesses and especially SMEs. In 2024 Bpifrance invested c€570m directly into 147 French start-ups with 58 first time investments in companies. It also acts as an LP for French VC firms committing €1.7bn to French venture funds in 2024.

In this update we look at the UK equivalent of Bpifrance, the British Business Bank.

The British Business Bank was set up by the UK government’s Department of Business, Industry and Skills in 2014 with initial funding of £1bn. Its mission was to act as a development bank for small and medium sized enterprises in the UK, gathering a previously diffuse series of schemes (Enterprise Capital Funds, Enterprise Finance Guarantee, Small loans Guarantee fund etc) run under the auspices of the UK government. Post Brexit the British Business Bank took up the functions previously run by the European Investment Bank, receiving the UK portion of the funds from the European Investment Fund.

The mission statement of the BBB is to drive sustainable growth and prosperity across the UK, and to enable the transition to a net zero economy, by improving access to finance for smaller businesses.

The BBB designs, delivers and manages access to finance programmes for smaller businesses across the UK aiming to increase the supply and diversity of finance and raise awareness of the finance options available to smaller businesses. The BBB typically has not invested directly into companies but instead invests in or alongside private VC funds which invest in companies. It has more than 200 delivery partners. The Bank deployed £3.5bn of public funding into UK smaller businesses in 2023.

According to Pitchbook data the British Business Bank is the largest investor in UK venture and venture growth capital funds. Its equity programmes have supported 22 of the UK’s unicorns, representing 56% of the UK’s current unicorn total.

The BBB administers the Enterprise Capital Funds programme established to increase the level of early-stage equity finance going to young businesses with high growth potential. The programme involves the commitment of public funds to address fund-raising constraints faced by venture capital funds. The BBB typically acts as a limited partner in these funds.

British Patient Capital was launched by the BBB in 2018 with £2.5bn of capital. Its focus is on later stage venture and growth capital, and it invests in established funds as an LP. As of March 2024, BPC managed assets of £3.25bn with £2.3bn in fund and co investments. The branding of British Patient Capital has from 2025 been retired and its activities subsumed into the core British Business Bank.

Recent investments have included £15m in Quantexa’s $175m Series F in March this year and a £10m investment in the £58m Series A of Maxion Therapeutics.

In February 2025, the BBB made a £20m investment in Cambridge Innovation Capital’s £100m Opportunities Fund’ focused on scale up opportunities from university spinouts. CIC was launched in 2013 and invests in deep tech and life sciences businesses that have a connection with the Cambridge ecosystem. The BBB has also invested in other funds, including Northen Gritstone and the UCL Technology Fund.

Historically the BBB supports venture capital firms who lead rounds. It has not taken a role in leading or pricing rounds but has supported as a follower.

This appears about to change in a series of significant announcements related to the BBB’s mandate made by the UK government at the end of June.

As the government has focused on promoting growth in the UK economy the mandate and resources of the BB have been beefed up.

In June 2025 the UK Government made an announcement that it describes as ‘transforming the resources and capabilities of the British Business Bank to deliver the UK’s modern Industrial Strategy and boost growth, marking a major step change in financing to support smaller businesses to start and scale in the UK.’

The key elements are

- The British Business Bank's total financial capacity will be increased to £25.6bn, enabling a two-thirds increase in investments to around £2.5bn pa.

- In turn this investment is expected to crowd in tens of billions of pounds of private capital to support innovative UK businesses

Also in June, on the back of the UK government spending review, the Secretary of State for the Department for Business and Trade announced that £6.6bn of new capital is being committed by the British Business Bank to boost growth

Within this the British Business Bank launched a new £4bn initiative, the BBB Industrial Strategy Growth Capital. Its aims are:

- To tackle the scale-up financing gap for priority sectors by investing greater amounts in companies through direct investments, leading future investment rounds and making strategic large investments of up to £60m in UK growth and innovation companies.

- The Bank’s targeted eight growth sectors are advanced manufacturing, clean energy industries, creative industries, defence, digital and technologies, financial services, life sciences, and professional and business services.

- Building a long-term funding ecosystem by corner stoning specialist venture capital funds investing in modern Industrial Strategy sectors and doubling support for emerging fund managers.

- Working with industry to develop new products and solutions to support priority sectors - for example by making early-stage direct investments into UK AI companies with a view to keeping them in the UK longer term, or creating new specialist debt funds to leverage private investment into supply chains of priority sectors.

- The aim is to crowd in another c.£12bn of private capital to deliver a total of c£16bn of capital in smaller businesses and innovation in the eight growth sectors over the next four years.

It is hoped that these measures may deliver around £30bn of additional Gross Value Add (GVA) to the UK economy through incremental company growth over the life of the investments.

There is also a commitment to regional diversity with a £2.6bn capital commitment to drive the growth of smaller businesses across the UK’s Nations and regions. Key measures will include:

- Launching two new Nations and Regions Investment Funds, totalling £350m, in the East and South East of England. These funds will address regional finance gaps outside traditional hotspots by bringing targeted equity and debt finance to support innovation clusters.

- Strengthening regional innovation through additional targeted £100m investment into the existing Nations and Regions Investment Funds within ten clusters working with Innovate UK: Greater Manchester, West Yorkshire, the West Midlands, Liverpool City Region, South Yorkshire, North East, West of England, Glasgow City Region, Cardiff Capital Region, and Belfast City Region.

- Expanding the British Business Bank’s Regional Angels Programme: helping reduce regional imbalances in access to early-stage equity support for smaller UK businesses.

- Expanding diverse angel networks through new Angel Syndicate Support and Embracing Diversity programmes: these will deliver operational support to angel syndicates.

- Creating an inclusive investment ecosystem with a new Investor Pathway Capital programme This new £400m initiative has been launched to back diverse and emerging fund managers

Louis Taylor, CEO of the BBB, commented, ‘This is a strong endorsement of the Bank’s 10-year track record, market access and capabilities, including our position as the largest investor in UK venture and venture growth capital funds and the most active late-stage investor in UK life sciences and deeptech.

Markets – Europe to the fore

Both the S&P500 and Europe’s STOXX600 were up 6% ytd to end June in local currency.

Despite the geopolitical (Ukraine, Israel, Iran) and economic (Liberation Day) turmoil, both the S&P 500 and the EuroSTOXX 600 finished H1 up 6% in local currency terms.

The weakness of the dollar meant that, measured in € terms, EU markets led the way in H1, up 10% with the UK up 4%, global stocks down 3%, the US down 7% and the Magnificent Seven down 10%.

The FTSE Venture Capital Index which measures the performance of the US venture capital industry, with a strong sector weighting towards technology, was up 19% in H1.

Since the half year end the original deadline of the US’s 90-day tariff suspension on July 9th has passed without further major upset. A July 7 executive order from the US President pushed the deadline on country specific tariffs back to August 1. The issue remains with the US administration threatening a 50% tariff rate on Brazil and a 50% tariff on copper imports into the USA. Around 15 countries have been issued notices warning of the imposition of higher tariffs on August 1 unless new agreements come into place.

European stocks have outperformed in 2025 ytd

Year to date local currency equity returns are well ahead of inflation. Business surveys still suggest a benign growth outlook and corporate earnings downgrades have moderated after the initial shock effect of tariff changes. Much of the commentary suggests an initial pause to activity that has subsequently recovered.

Cross Asset Class Returns

Fed interest rate cuts: As expected the Fed held rates steady for the fourth meeting in a row at 4.25%-4.5% on June 6th with most of the Fed’s rate setters saying that tariffs would have ‘persistent effects’ on inflation. The notes from the FOMC meeting show that ten of its members look for two or more quarter-point cuts by the end of the year, two anticipate one cut and seven no cuts. President Trump’s view is that rates are ‘at least three points too high.’

There are four more meetings to the end of the year (July 30, September 17, October 29, and December 10). The market, and indeed Fed Chair Jay Powell, has not ruled out a July rate cut. With the number of FOMC members opposing rate cuts having risen though, the consensus market indicator is for two 25bps rate cuts, one each in the October and December meetings, to leave rates at 3.75%-4% by year end.

In Europe, the ECB cut interest rates again in early June to 2%, the eighth rate cut since June 2024 following the drop in the May inflation figure to 1.9%, below the ECB’s target 2% for the first time since September 2024. The ECB is forecasting an interest rate of 1.6% for 2026. It looks for economic growth of 0.9% in 2025 and trimmed its 2026 forecast by 10bps to 1.1%. With ECB president Christine Lagarde confirming that the interest rate cut was an ‘almost unanimous decision’ the market confidently expects a further two cuts by the end of the year.

In the UK, the Bank of England cut interest rates in early May by 25bps to 4.25%. It then held interest rates steady at its June meeting with the monetary policy committee splitting 6-3 split on the rates on hold/ reduction decision. Subsequent figures showed the UK economy shrinking unexpectedly by 0.1% in May after a 0.3% decline in April. UK inflation is still above target at 3.4% in May, after 3.5% in April. The UK also has tariff uncertainty with BoE Governor Andrew Bailey commenting on interest rates ‘The path remains downwards, but how far and how quickly is now shrouded in a lot more uncertainty, frankly.”

The market expectation is for two further interest rate cuts of 25bps by end 2025 starting, post the disappointing May GDP growth number, with a 25bps cut at the August meeting.

Rothschild & Co strategist Kevin Gardiner summarises the current key drivers of the market in this graphic:

June– Another strong month for growth equity raises

US up 2x in June yoy; Europe up 50%

US VC raises in June 2025 up 100% on June 2024: June saw 38 US venture capital raises of $100m or above, raising $31.2bn. This is more than twice the level of June 2024 when the total was $15bn.

Unsurprisingly the month’s raises were led by AI deals. There were four $1bn plus raises, three of which were for AI businesses.

Scale AI raised $14.3bn at a $29bn valuation in deal with Meta. Scale provides data labelling and model evaluation services delivering high quality training data for AI applications such as self-driving cars, mapping, AR/VR, and robotics. Meta is keen to access the specialised datasets for LLM training to improve the performance of its Llama 4 models. Meta is taking a 49% stake in Scale AI while the founder of Scale, Alexander Wang, will head Meta’s new superintelligence research lab.

At the end of the month xAI completed its long-awaited raise. The equity raise was $5bn and the company secured another $5bn in debt. The proceeds ‘will support xAI’s continued development of cutting-edge AI solutions, including one of the world’s largest data centres and its flagship Grok platform.’

The largest seed round in Silicon Valley history was the third of June’s big AI raises. Thinking Machines Lab, founded by the former CTO of OpenAI, Mira Murati raised $2bn at a valuation of $10bn in a deal led by a16z. The six-month-old company is pre revenue and indeed pre- product. Earlier this year it indicated that it is working on making “AI systems more widely understood, customisable and generally capable.’ It has though a number of other former OpenAI employees working for it including co-founder John Schulman, former head of special projects Jonathan Lachman, and former vice-presidents Barret Zoph and Lilian Weng. It is an example of the AI minted concept of a ‘talent unicorn.’

Defence technology has come into vogue post the Ukraine War and given the heightened geopolitical tensions around the world. Anduril offers a range of autonomous defense systems, and the AI based software that controls them. Anduril’s systems are powered by Lattice, an AI-based operating system that connects autonomous sensemaking and command & control capabilities with modular and scalable hardware components. Products include the Barracuda family of military drones, the Roadrunner reusable vertical take-off and landing (VTOL) Autonomous Air Vehicle (AAV) and the Dive-LD autonomous underwater vehicle. The company raised $2.5bn in a Series G which valued it at $30.5bn, twice the valuation of its previous round. Revenues in 2024 doubled to $1bn. In February Anduril was granted the U.S. Army’s contract – with a headline value of $22bn - for developing new AR/VR headsets. The round was led by Founders Fund which subscribed $1bn.

The US – $31bn of US venture backed raises of $100m+ in June

Europe - $4.5bn of VC deal value in June: It was also a noticeably strong month for venture capital raises in June in Europe. The R&Co Deal Monitor registered 62 raises of $20m or more. The total of $4.5bn raised was the second strongest month of the year to date (January was $4.9bn), the fifth biggest month since the start of 2022 and was up over 50% by value against June 2024. For the second month in a row there were 13 deals raising $100m or more.

The largest deal in the month was the $690m raise for the AI driven German defense business, Helsing. The round was led by Prima Materia ( the investment vehicle of Spotify founder Daniel Ek, who is also Helsing’s chairman), Lightspeed and Accel and valued the business at $13.2bn. Helsing’s previous Series C raise in 2024 was for €450m. Helsing uses AI to develop applications for defence, focusing on all-domain defence innovation ( air, land, sea, space, and cyber).

There were two more AI focused businesses in the top 13 deals by value. Spain’s Multiverse Computing raised $215m in a deal led by Bullhound Capital. Multiverse’s flagship product is CompactifAI, an AI model compression tool that reduces AI model size while maintaining performance, leading to lower energy consumption and costs. The UK business, PhysicsX raised a $135m Series B led by Atomico, with participation from Temasek, Siemens, Applied Materials, and July Fund. PhysicsX is building a new engineering software stack to bring AI enablement to the engineering lifecycle, equipping manufacturing organizations in aerospace & defense, automotive, semiconductors, materials, and energy with tools to solve challenges at an accelerated pace.

Each of fintech, biotech and cybersecurity saw two big raises.

German fintech Scalable Capital, a digital investment platform for retail investors, raised $177m from Sofina, Noteus and Balderton Capital. Dutch financial management platform for SMEs and freelancers, Finom, raised $132m in a deal led by AVP.

In Biotech a rare Welsh raise came from Draig Therapeutics with the Cardiff based company raising a $140m Series A for treatments for neuropsychiatric disorders. The company has a phase 2 trial candidate for a major depressive disorder. SV Health Investors led the deal. Spain’s Splice Bio raised $135m from EQT Life Sciences and Sanofi Ventures. Its research in protein engineering has produced a proprietary protein splicing technology platform to create next-generation gene therapies.

In cybersecurity Cato Networks of Israel raised $359m at a $4.8bn valuation from Vitruvian Partners and ION Crossover. Cato provides enterprises with a united software-defined wide area network (SD-WAN) and network security platform, delivered as a global cloud service. Also, in Israel Coralogix raised $115m at a $1bn valuation for its observability platform that gives teams real-time insights across systems, security, and AI workloads. The raise was led by NewView Capital.

Elsewhere German satellite space launcher business, Isar Aerospace raised $172m in a deal led by Eldridge Industries. Nuclear fusion energy company, Proxima Fusion raised $145m led by Cherry Ventures. Israeli medical device business ForSight Robotics has developed a hybrid surgical robotic platform for widespread eye diseases, called ORYOM. It raised $125m in a Series D led by Eclipse and the Adani Group. Luxembourg based quick commerce supermarket delivery business JOKR raised $100m from Activant Capital and G Squared.

Europe – $4.5bn of VC raises in June

Fundraising outlook: Public markets have recovered from the turmoil of Liberation Day, are looking through threats to revive some of the tariff proposals on a piecemeal basis (copper, Brazil) and have absorbed the implications of the ‘big, beautiful bill’ and are at close to their all time highs. This is being reflected in the private markets as well. Q2- which captures the period of the Liberation Day tariffs (Liberation Day was April 2) saw US VC raises rise 69% yoy in value to $51.7bn (2024 $30.6bn) versus Q2 2024. In Europe Q2 fundraising was up 24% yoy to $10.6bn.

Despite a number of large deals having come though in these months the forward pipeline of raises appears robust. Our monitor of impending raises is at around the $10bn mark. Recent additions and amendments are:

The humanoid robotics business Figure AI is said to be looking to raise $1.5bn at a $39.5bn valuation. It last raised $675m in 2024 at a $2.6bn post money valuation.

Cohere, the Canadian LLM business focused on enterprises, is looking to raise $500m at a valuation of $6.5bn. Its ARR is at c$100m.

Europe’s LLM business Mistral is reported to be seeking up to $1bn in equity from investors, including Abu Dhabi’s MGX fund.

Various reports have UK fintech Revolut conducting a mixed primary secondary round of c$1bn at a valuation of as much as $65bn. Greenoaks is said to be leading the new money round. Mubadala is reported to be considering an additional $100m investment.

Growth Equity – c$10bn in reported upcoming raises

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts has led to increased optimism and enthusiasm for growth equity in 2025. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment led to a sharp impact on valuations in private markets. The scale of the fall in the FTSE Venture Capital Index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Outside the AI space the VC market is regaining confidence with a revival of interest in fintech, biotech and software being notable. Certain investors remain very active in the space with substantial funds to deploy. There remains substantial dry powder in the VC industry.

- The speed of the investment process has slowed since 2021-22. The level of diligence on new deals has stepped up.

- 2023 and 2024 saw more down rounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- Recent initiatives by the US to impose tariffs on its trading partners is likely to impact US and global economic growth and to negatively affect the fund-raising environment for venture backed companies.

- It seems that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and on DCF and comparative based multiples.

Read the previous editions:

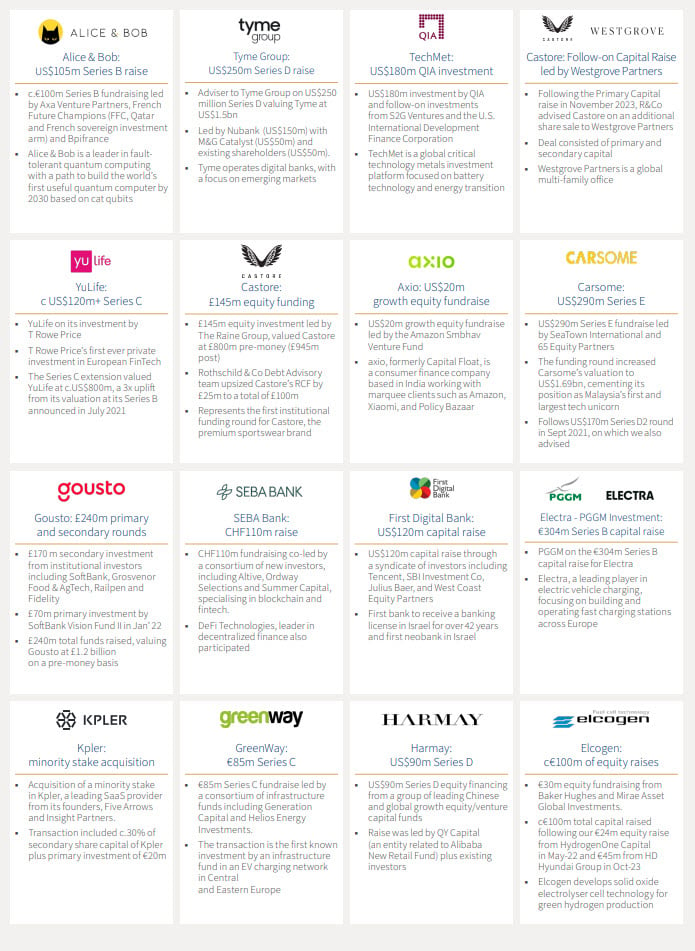

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Chris Hawley

Global Head of Private Capital

chris.hawley@rothschildandco.com

+44 20 7280 5826

+44 7753 426 961

Patrick Wellington

Vice Chairman of Equity Advisory

patrick.wellington@rothschildandco.com

+44 20 7280 5088

+44 7542 477 291

Thomas Chung

Head of Private Capital, North America

thomas.chung@rothschildandco.com

+1 212 403 5559

+1 917 594 7208

Mark Connelly

Head of North American Equity Markets Solutions

mark.connelly@rothschildandco.com

+1 212 403 5500

+1 917 297 5131

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.

Read more articles

-

Rothschild & Co impulsa su crecimiento en España con la incorporación de Álvaro Santos en el área de Wealth Management

Press releases

El nuevo nombramiento refuerza las capacidades locales y supone un paso más en la expansión del negocio de banca privada en España.

-

Geopolitics Blog: Christmas Season: Reasons to be cheerful

Insights

In our latest geopolitical blog, Mark Sedwill, Chair of Geopolitical Advisory at Rothschild & Co offers his reflections on six strategic reasons for Christmas confidence.

-

Five key questions for a carefree retirement

Corporate

Planning for retirement early helps secure your finances and gives you the freedom to enjoy travel, hobbies or family time. These key questions can guide you

-

Growth Equity Update

Insights

This is the latest Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory. 52% of the $63.4bn raised by the US growth equity market in Q4, up 31% yoy, was for AI companies. Datacentres, defence and crypto made strong showings. In this edition we look at the rise of the prediction marketplaces, Polymarket and Kalshi. Polymarket’s $2bn November raise at an $8bn valuation was up from $1.2bn in January. Kalshi’s valuation was $2bn in June and $11bn in November. We predict what’s ahead for them in 2026.

-

Global Advisory: Rothschild & Co Redburn Review - December 2025

Insights

Rothschild & Co Redburn have shared their final review of 2025, where they discuss all these questions, and more.

-

Building international leaders in the mid-market

Private Assets