Donald Trump Day

After weeks of uncertainty, the exact terms of “Liberation Day”, as dubbed by the President of the United States, were unveiled late Wednesday (French time), when Donald Trump officially announced the broad strokes of his trade policy in terms of tariffs.

The new President announced the launch of 10% minimum tariffs on all imports to the US starting April 5th, coupled with “reciprocal tariffs” imposed on a case-by-case basis on the majority of US trade partners beginning April 9th. According to the Trump Administration, the calculation of these tariffs was based on Non-Tariff Barriers to Trade (NTBs), currency devaluations and other taxes levied on US exports. The “reciprocal tariff” rate applied by the US at this point will be 50%. In actuality, the “reciprocal tariffs” as defined appear to target the re-balancing of the trade deficit between the US and its various trade partners.

While on the whole, the announcements themselves exceeded market expectations, the impact varies considerably depending on the partner. A few examples:

Tariffs of 34% were set for China, in addition to the 20% already announced early in the year. Asian countries have been hit the hardest, with a rate of 46% imposed on Vietnam.

- 24% for Japan

- 20% for the European Union

- 10% for the United Kingdom and most South American partners (excluding Mexico)

Canada and Mexico will continue to see their exports exempt from new trade tariffs, in accordance with the USMCA1.

These new measures do not apply to products already subject to sector tariffs, such as steel, aluminium and the automotive industry – all sectors subject to confirmed 25% tariffs with immediate effect. It should be noted that the semiconductor and pharma sectors are not subject to specific measures (as of yet).

The April 2nd decree represents one of the largest tariff hikes in US history. The effective tariff rate is up from just under 2.5% in 2024 to 22% after the implementation of the announced tariffs2, i.e. its highest level since 1930.

What can we expect to see in terms of retaliatory measures by US trade partners?

Faced with the near-immediate application of these new trade tariffs, the first thing we can expect to see its trade partners do is try to exploit possible margins of negotiation with the US administration. The separation of tariffs into two categories suggests that the 10% base tariff will probably be difficult to negotiate, while the “reciprocal tariff” category may be open to more adjustments. US Treasury Secretary Scott Bessent himself intimated that tariffs could be negotiated depending on the attitude adopted by the various partners.

Should such negotiations fail, however, the risk of escalation has significantly increased, with counter-tariffs likely to be announced, in particular by the European Union and China, also with the aim of targeting services provided by large US tech corporations. For its part, the Trump Administration has indicated that the “reciprocal tariff” rate, currently set at 50%, may be increased if other countries decide to take retaliatory measures. As a result, the uncertainty surrounding tariff policies is expected to remain high in the coming days.

What impact will these policies have on the financial markets?

The equity markets have delivered contrasting performances thus far in 2025, defying forecasts issued in late 2024, when investors welcomed the prospects associated with the election of Donald Trump. At the time, tariff barriers were relegated to the rank of negotiation tactics, with a magnanimous view of future tax cuts and other promised deregulation moves, back when the Euro was steadily making its way towards parity.

On the downside, the US markets seem to have hit a snag in the wake of two exceptional years in 2023 and 2024, when the S&P 500 gained +26.3%3 and +25.5%3, respectively, while the EuroStoxx 50 climbed +23.2%4 and +11.3%4. 2025 is shaping up to be a reshuffle, however. After peaking at +4.9%3 on February 19th, the flagship S&P 500 index is now suffering the impacts of economic and geopolitical uncertainty, combined with budget cuts enacted by the Trump Administration, all of which investors responded to by triggering a 7.5%3 correction, shaving another -3.3%3 off the index year-to-date (at April 2nd). This drop is mainly led by what are referred to as “growth” sectors, with the Nasdaq down 6.6%3 YTD, and by smaller caps exposed to the economic cycle, with the Russell 2000 losing 8.0%3 (at April 2nd).

That said, despite the volatility putting US equities in the red during the first quarter, the recent correction is not enough to erase the gains earned in 2024. Since 31 December 2023, the S&P 500 still shows a cumulative gain of +20.9%4.

The situation is much different in Europe, notably driven by rearmament plans aimed at shoring up the Defence sector. The EuroStoxx 50 is up +8.8%4, with Germany leading the way (+11.82%4 for the DAX), aided by a new Government committed to supporting its economic development. In France, despite the challenges faced by luxury sector names, the CAC 40 has picked up +6.4%4 YTD. The EuroStoxx 50 has climbed +21.8%4 since 31 December 2023, while the CAC 40 has struggled with a meagre +7.7%4.

Looking at “emerging” markets, the MSCI Emerging Markets index has risen 4.3%3 in 2025, a performance largely carried by the MSCI China index, which has shot up +18.3%3 YTD, rocket-fuelled by government stimulus measures and innovation in principle ushered in by DeepSeek. Since early 2024, China has racked up a remarkable gain of +38.6%3.

On the interest rate front, the yield on the US 10-year treasury note hit a peak of 4.8% on January 14th before sliding down to 4.0% on April 2nd, due to fears surrounding the economic outlook brought on by US tariffs. Conversely, the French 10-year OAT continued on the gradual climb started in early 2024, increasing from 2.6% on 1 January 2024 to 3.2% on 1 January 2025, then 3.4% on April 2nd. Similarly, the German Bund started the year at 2.4% and ended at 2.7% on April 2nd. Rising long rates in Europe have nevertheless been offset by the tightening of Investment Grade credit spreads, protecting the asset class and allowing it to maintain a very slightly positive performance in the first quarter of 2025 (iBoxx Euro Corporate in EUR at +0.2%4).

A definite macroeconomic impact, coupled with persistent uncertainties

If we try to perform an initial macroeconomic analysis of the measures announced by Donald Trump, we can see they will definitely have an adverse impact on global GDP, with the hiking of trade tariffs set to unavoidably hinder global economic activity

Risk of stagflation in the United States

Broken down by major geographic area, the US economy should – in light of the announcements made, and bearing in mind that they are still in place – see a resurgence in inflation in the short term, liable to increase from +1% to +1.5%5, primarily due to goods with no local alternatives. As a result of this resurgence, US consumers are likely to take a direct hit to their purchasing power. Though difficult to estimate, a negative impact of roughly -1%/-1.5% on US GDP compared to previous expectations of around 2% growth is credible, which would bring the US economy dangerously close to recession, with much greater risk of stagflation.

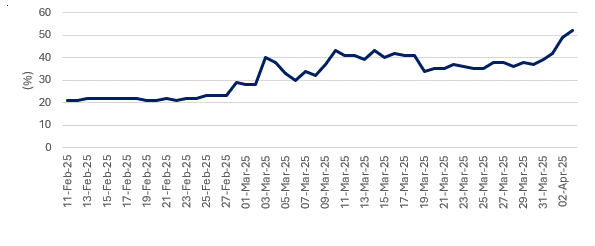

Recession is thus beginning to look like the main scenario favoured by forecasting platforms, with the risk of a US economic recession in 2025 estimated at 52% by Polymarket the morning after “Liberation Day”, versus 22% at end-February.

Probability of a US economic recession in 2025

According to public event prediction platform Polymarket at 10:00 a.m. on 3 April 2025

In addition to the direct impact on US consumption, the “uncertainty” impact could take just as large a toll on the US economy: the indirect effect of more prevalent “wait and see-ism” by consumers before making purchases, or by US businesses when it comes to investing, is very real and hard to estimate in the short term, but cannot be overlooked.

US exports should also be subject to tensions in relations with major trade partners, not to mention potential retaliatory measures liable to arise in the coming days or weeks...

Up to now, these negative revisions to US economic growth forecasts on the heels of the tariff announcements have predominated over considerations of inflation making a comeback in the future and its impact on US government bonds. Inflation expectations will determine how quickly the Federal Reserve responds. This response may be slow, especially in the event of a disconnect with these same inflation expectations.

An inflation hike of 1% or 1.5% would put the Fed in an eminently complicated position for rate cuts in 2025, in that any sudden weakness in demand or sudden spike in unemployment triggering a “rapid” recession would require the central bank to intervene by cutting its policy rates. Such cuts would likely come later rather than sooner, given the now-upward risks on US inflation, capable of generating volatility on the bond markets.

In theory, the trade tariffs could bring in an additional $600 million in federal income, representing the largest increase in taxes since the Revenue Act of 1968 and reducing the deficit/GDP ratio by around 2 points. This in turn could serve to fund potential tax cut measures.

The US Senate is currently considering the permanent renewal of tax cuts for certain households and on companies enacted by Trump in 2017 (from 35% to 21%), which could offer a form of support in particular to domestic firms and middle classes, but for now such a move is in the preparatory phase.

Euro Zone and Asia: retaliation or negotiation?

In the Euro Zone, these measures could reduce economic growth by at least 0.4% to 0.6% in the coming quarters6; in such case, a mild technical recession cannot be ruled out, especially for Germany, set to subsequently benefit from early-2025 tax announcements.

The Euro Zone's economic outlook is very different, with 0.9% growth in 2024 and 0.9% previously expected for 2025. However, the impact of the Euro’s appreciation could be doubly negative, making imports more expensive and incurring tariffs on exports.

The inflationary impact foreseen in Europe appears potentially more limited, with US imports accounting for just 7% of final European demand. Consequently, the initial impact should have more to do with the economic slowdown of US GDP. The European Central Bank may take a more accommodative stance in response to these economic downturn risks, given the heightened risk of falling below its medium-term inflation target.

Meanwhile, the economic impact in Asia should be heavy at roughly 0.6% on the economic growth of Asian countries (on average), with wide-ranging disparities. In China, these announcements could shave 2% off GDP7, further encouraging the government to stimulate domestic consumption in order to offset the consequences on exports and move closer to its target of around 5% growth in 2025.

At this stage, Trump’s initial raft of announcements is liable to put predominantly downward pressure on economic growth and inflation in Asia.

Given how (highly) evolving the situation is, and the high probability of counterattacks by trade blocs (in the coming days and weeks), we are fairly modest in our expectations when it comes to the main macroeconomic impacts on the horizon. Estimated effects on growth and inflation, Central Bank policies and corporate profits will all evolve in concert with these future announcements...

1 - United States-Mexico-Canada Agreement, adopted on 1 July 2020

2 - Source: BNP Paribas Exane

3 - Source: Bloomberg, in USD, performance with dividends reinvested

4 - Source: Bloomberg, in EUR, performance with dividends reinvested

5 - Source: BofA, JPM

6 - Source: Christine Lagarde, in case of 20% tariffs; Bank of America

7 - UBS estimate

Contact us

The Rothschild Martin Maurel teams are at your disposal to provide you with the best possible advice on these subjects.

-

Rothschild & Co impulsa su crecimiento en España con la incorporación de Álvaro Santos en el área de Wealth Management

Press releases

El nuevo nombramiento refuerza las capacidades locales y supone un paso más en la expansión del negocio de banca privada en España.

-

Geopolitics Blog: Christmas Season: Reasons to be cheerful

Insights

In our latest geopolitical blog, Mark Sedwill, Chair of Geopolitical Advisory at Rothschild & Co offers his reflections on six strategic reasons for Christmas confidence.

-

Five key questions for a carefree retirement

Corporate

Planning for retirement early helps secure your finances and gives you the freedom to enjoy travel, hobbies or family time. These key questions can guide you

-

Growth Equity Update

Insights

This is the latest Growth Equity Update from Patrick Wellington, Vice-Chairman of Equity Advisory. 52% of the $63.4bn raised by the US growth equity market in Q4, up 31% yoy, was for AI companies. Datacentres, defence and crypto made strong showings. In this edition we look at the rise of the prediction marketplaces, Polymarket and Kalshi. Polymarket’s $2bn November raise at an $8bn valuation was up from $1.2bn in January. Kalshi’s valuation was $2bn in June and $11bn in November. We predict what’s ahead for them in 2026.

-

Global Advisory: Rothschild & Co Redburn Review - December 2025

Insights

Rothschild & Co Redburn have shared their final review of 2025, where they discuss all these questions, and more.

-

-

Asset Management: Monthly Macro Insights - December 2025

Market Commentary

Despite geopolitical tensions and trade frictions, GDP growth in 2025 proved surprisingly resilient, slowing only slightly compared to 2024. However, vulnerabilities remain, as several factors that have supported the global economy thus far may prove to be temporary.

-

CIO Lens: Bubbles, brooding and balance

CIO Lens

AI-driven optimism keeps markets buoyant, but stretched valuations and lingering global uncertainty remind investors to stay vigilant.

-