Growth Equity Update

September 2025 – Edition 42

- A League of Their Own: ‘We believe the broader potential ecosystem of sports, media and entertainment investing is significant and underpenetrated.’ Ares Capital.

- We dive into the world of emerging sports leagues and the venture capital funding behind these innovative takes on traditional sports and the VCs that help fund their emerging business models.

- Vorsprung durch Technik: We look at how the German Federal government is looking to kick start progress through technology with measures to promote the venture capital industry in Germany and an entrepreneurial mindset.

- The Deutschlandfonds initiative is a €100bn fund of funds whose mission is to fill the gap in growth and innovation financing in Germany. The German government is providing €10bn in equity, with private backing to take the total to the €100bn.

- The AI investors: As Anthropic raises another $13bn at a $170bn valuation, six months after a $3.5bn raise at a valuation of $61.5bn, we review the major growth equity investors in the AI raises since the start of 2023.

- August – seasonal lows but y-o-y advances: US VC raises in August 2025 were up 6% yoy in value at $6.7bn and September is already ahead of 2024. Europe saw $1.9bn raised in August, the smallest month of the year to date but 2.3x the level of August 2024 bringing the ytd advance in European VC capital raised to 26%.

Click here to download a PDF version of Growth Equity Update

A League of Their Own

A dive into the world of venture capital funding in sports

Private equity’s involvement in sports has been well charted in recent years. Major private equity investors in the sports industries – the likes of Arctos Sports Partners, Ares, CVC, SilverLake, Redbird, MSP Sports Capital, Sixth Street Partners and others have allocated substantial funds to the sports industry in recent years. The process has been fuelled by changing regulations which, for instance, have meant that all the major US Sports leagues are now open to private equity investment starting with the decision by Major League Baseball to permit such investment in 2019. In August 2024 the NFL became the last of the big US sports leagues to open, allowing 10% of a team to be owned by private equity. Europe’s sports leagues and teams embraced this trend earlier seeing a wave of private equity investment from the early years of this century.

The attractions of the sports industry arise from the large loyal audiences attracted to teams and leagues, the opportunities for monetisation of physical attendance at live events, substantial media rights packages – typically growing fastest in the US, and more slowly growing from a high base in Europe- the ecosystem of related media content ( highlights, news, clips) plus fast developing revenue streams like sponsorship, gaming, merchandise and digital distribution.

The virtuous circle of media rights and the boosting of the underlying sports and teams has been emphasised using sports ‘documentary’ series by the big streaming platforms to drive audiences. A prominent example is the Netflix ‘Drive to Survive’ charting the Formula 1 racing season and now in its seventh series. European soccer watchers are familiar with fly on the wall series about major and minor soccer clubs from ‘First Team: Juventus’ through ‘Sunderland ‘Til I Die’ to Emmy Award winning ‘Welcome to Wrexham.’

For private equity one of the attractions of the sports industry is that it offers underlying investors an alternative asset class with low correlation to the underlying equity market and attractive low volatility characteristics derived from persistent (often life-long) fan demand and long duration broadcast and digital contracts.

Where does the VC and growth equity investor fit into all this? Private equity is playing in the big leagues, but the attractions of the sports model have led to a plethora of alternative and modified sports appearing, looking to capture similar demand characteristics at an earlier stage of a sports lifecycle.

Opportunities abound. Readers will be familiar with the startling growth and success of women’s sports, notably football. Interest in alternative racquet sports like padel and pickleball has surged in recent years. New motorsports, often picking up on the ‘green’ theme have emerged, with the development in car racing of Formula E and Extreme E, in motorbikes of the Moto E World Cup and rallycross RX2e and, on water, the E1 powerboat series and the conventional power F1H2O Series.

The relative scarcity of major leagues and teams makes this emerging field of substantial interest in the VC world. The Exhibit outlines a selection of recent ‘league deals’ carried out by VC investors demonstrating the emergence of alternative versions of mainstream sports.

Recent VC Investments in Sports Leagues

In May 2024 the King’s League raised $64m in a deal led by Left Lane. The Kings League has adapted traditional soccer. Games last 40 minutes on specialist pitches and start with a ball drop. It’s a 7 vs 7 game but the teams start with one player with the rest coming on sequentially at intervals in the first five minutes and, after that point, there are unlimited substitutions. There are ‘golden goals (count double) in the last two minutes of each half and no draws, with a penalty shoot-out deciding the tie if necessary.

The league started in March 2023 with twelve teams and was instantly successful with a sell out at the 90,000 Barcelona Camp Nou stadium, home during his football career, to founder Gerard Piqué. The teams are headed by footballers (Kun Aguero, Lamina Yamal, Iker Casillas), YouTubers and streamers (Junichi Kato, Jynxziu, Gerard Romero, DjMaRiiO) and celebrities (Jake Paul - boxer, GIMS - singer). All matches are streamed by the league across its own channels on Twitch, Kick and YouTube and games are shown live on TikTok and X and on traditional broadcast channels like Sky Sports and ESPN. The Kings League states that from January 2024 to January 2025, it received 14 billion brand impressions with sponsorship accounting for c75% of revenues. 85% of the league’s audience is under 35.

The dynamic between ownership of the league and of the teams and where the economics lie between the two is always a key feature of sports models. At one extreme team can be owned independently of the league and use their power to extract economic benefit from the broadcast and other revenues collected by the league. This is the model seen in Formula One where the economic relationship between the league, F1 Group, and the teams is dictated by the Concorde Agreement. The League takes a proportion of the revenues but, beyond a certain point, incremental revenues fall disproportionately to the teams who, however, must bear their own costs for developing and running their cars.

The other extreme of the model is where the League controls all the revenues but bears the costs not only of hosting the event but of funding the teams. It is a version of this model that is used by the King’s’ League. It covers the cost of the bulk of the players (special wild cards can be funded by the teams, albeit with a salary cap) and limits the number of teams per league to twelve. Teams are owned by personalities and generate revenue through sponsorship, specific media and merchandise.

Franchises (teams) in the King’s League generate between €0.5m-€2.5m pa in revenues. There is a market in the value of the team franchises. Spanish YouTuber Perxitaa, for instance, recently sold a 15% stake in his King’s League franchise, Troncos FC, for €0.6m, valuing the franchise at €4m. For perspective this is around 50% of the value being placed on some of the second-tier clubs in Spain’s La Liga.

A similar personality-heavy (Virat Kohli, LeBron James, Will Smith, Tom Brady, Rafa Nadal) business model is employed by the electric powerboat racing E1 Series. In this model the E1 Series absorbs the cost of the electric powerboats and charges the personality-led teams to participate. The teams are nevertheless able to generate their own revenue (streamers are able to integrate the team into their own brands and content streams and can generate team specific sponsorship) and, as with the King’s League, there is a market in the value of the team franchises.

Meanwhile the financing from Left Lane has allowed the King’s League to expand its reach. It has now established leagues in Spain, Brazil, France, Germany, and Italy with plans to launch in the United States by 2026.

Staying with soccer, in December 2024 the Baller League raised $25m in a round led by EQT Ventures. The league originally started in Germany in 2023. It has some common characteristics with the King’s League. There are twelve teams per league involving well known former professional footballers (Mats Hummels, Lukas Podolski, John Terry) and influencers. The games last 30 minutes, are 6x6, and feature a series of ‘gamechanger’ rules (goals counting double, goalkeepers not allowed to use their hands, no passes backwards etc). UK and US editions were announced in 2025. The league, like its Spanish counterpart, relies primarily on sponsorship revenue. The games are streamed free on Twitch and YouTube.

The US has seen a stream of VC investment in new and challenger leagues. At the smaller end 2025 has seen a $15m round for the Snow League, a snowboarding and free skiing competition and a $10m raise for the Pro Padel League.

The Snow League was founded in 2024 by the three-time Olympic halfpipe champion Shaun White and aims to attract sponsorship, attendance, broadcast and merchandise revenues into a sport that tends to be the poor relation in money terms to traditional Alpine skiing events. To attract high level winter sports athletes there is prize money of $1.6m across four events in the Snow League’s first season. The first event took place in Aspen, Colorado in March 2025.

The ProPadel League obtained $10m in a seed round supported by Left Lane and Kactus Capital in April 2025. The league is in its second season and operates with ten teams with a plan to expand that number to twelve in 2026. PPL has five planned events in 2025 moving between New York, Miami and Mexico. Prize money is c$1m and sponsorship is again the main revenue source. The league hopes to break even in 2026. The CEO of Left Lane Capital, Harley Miller, comments “Having seen the explosion of padel globally, we recognized a chance to partner early with PPL to own the market for one of the fastest-growing emerging sports.’ Left Lane is also an investor in the King’s League and The Snow League.

A clear area of opportunity is in the rapid development of women’s sport. The recent raises show both established women’s professional sport and their challenger equivalents receiving VC backing. In February 2022 the Women’s National Basketball Association (WNBA) in its 26th season raised $75m in its first ever capital raise bringing Nike and other investors onto its cap table. The WNBA press release described it as ‘the largest ever raise for a women’s sports property.’ Press reports suggest the valuation of the WNBA and its teams is close to $1bn.

In December 2024 the challenger women’s professional basketball league, Unrivaled raised $28m in a Series A. It followed this up with a further raise at a valuation of $340m in September 2025. The new league offers a different format and business model to its more established counterpart. The game is played 3 vs 3 (instead of 5 vs 5) on a smaller court, with three 7-minute quarters plus a target score finish fourth quarter (versus 40-minute WNBA games). Unrivaled’s business approach is a player-centric model which it hopes will secure long term commitment. Players in Unrivaled earn higher wages than in the WNBA (up to $220k for three months, versus c$120k in the WNBA for six months). The WNBA runs May to October. Unrivaled takes advantage of the off season, running January to March meaning players do not have to go overseas to supplement their wages. The first 30 players who signed up to Unrivaled have a direct stake in the league amounting to a 15% equity stake. The league operates from a dedicated complex that includes game and practice courts, workout and recovery areas and childcare. Revenues derive from a media deal with TNT Sports and sponsorship deals. Press reports suggest Unrivaled made $27m of revenue in its first year and was just short of break- even. The league has signed up 90% of its roster for the 2026 season and is reportedly increasing wages.

A notable participant in growth equity deals in sport has been the Kingdom of Saudi Arabia. Saudi Arabia’s PIF has emerged as a major player in key high-level sports initiatives like LIV golf, boxing, and as a partner in tennis to both the ATP and WTA and in football as an official partner of the FIFA Club World Cup. Notably in February 2025 Surj Sports Investment, the sports arm of Saudi’s PIF, made a $1bn investment for a c10% stake in the global sports streaming platform DAZN.

Saudi investment has also reached down into emerging venture backed leagues. Surj, alongside Verance Capital and Cordillera Investment Partners, was an investor in the July 2025 $40m Series C round for the Professional Triathletes Organisation (PTO). The PTO specialises in endurance sports and mass participation and organises the T100 Triathlon World Tour as its marquee event. The world’s top 40 male and female triathletes compete alongside amateur athletes in cities including Singapore, San Francisco, London, Ibiza, Lake Las Vegas, and Dubai.

The King’s League is planning to launch in the MENA region supported by Surj Sports. In January 2024 the Saudi PIF created the Electric 360 partnership with Formula E, Extreme E and the E1 powerboat Series to support the growth of electric motor sports globally. The PIF also holds equity stakes in all three businesses.

The growth of sports VC investment is being fuelled by fundraising and specialist funds devoted to the sports industry. A number of names have been prominent in recent sports league VC investments. Left Lane has investments in the King’s League, League One Volleyball, the ProPadel league, Magnus Carlsen’s Freestyle Chess and the Real American Freestyle wrestling tournament founded by Hulk Hogan.

In July 2025 Ares launched a new media and entertainment fund targeting individual investors. The fund will make debt and equity investments in sports leagues, teams and sports-related businesses, as well as media and entertainment companies. Ares established its first dedicated $3.7bn sports strategy fund in 2022 and earlier this year raised $1bn for the first close of its second sports fund. Ares comments ‘While sports teams, clubs and leagues often draw much of the attention, we believe the broader potential ecosystem of sports, media and entertainment investing is significant and underpenetrated.’

Will Ventures has a range of sports investments including TMRW Sports a holding company for tech enabled sports leagues, starting with TGL, an indoor, team-based golf league headed up by Tiger Woods, Rory McIlroy and Mike McCarley. It is also invested in the Snow League and in an associated array of leisure and sports technology, data, brands, media and merchandise businesses.

The Monarch Collective, which focuses on women’s sports launched in 2023. This year it raised the size of its investment fund from $150m to $250m on the back of demand reflecting the perceived opportunity in women’s sports. The fund was formed to invest exclusively in women’s sports, particularly in leagues, teams and media rights.

For further reading around thus subject see Will Ventures - The rise of venture-backed sports leagues

Germany and the VC market

The German coalition government has stepped up efforts to promote investment into early-stage German companies.

In recent editions of the Growth Equity Update we have charted how the UK and French governments support early-stage business through public bodies and the encouragement of external investment into VC backed companies.

In this edition we look at Germany and the efforts of the state authorities to promote VC entrepreneurship. In an issue familiar with those following the UK government’s Mansion House Reform initiatives, the level of German pension find investment in private companies is very low. A study by Redstone Capital in June 2023 found that German pension funds provide less than 1% of the LP base for German VCs whereas US pension funds provide 27% of the LP base of US VCs. US pension funds indirectly own about 10% of German VC backed companies, 10x the level of German pension funds. (see Redstone Capital - German Pension Funds & VC .pdf)

Redstone illustrates the contrast by comparing the allocation of Germany’s largest pension fund, the c€34bn Civil Servants' Insurance Association (BVV Versicherungsverein) with that of the Washington State Public Retirement plan, one of the largest public pension funds in the US with over $100bn in net assets. The US fund’s exposure to private equity and venture capital is 27%. The German fund’s exposure is less than 1%. We may congratulate the German fund on its superior liquidity profile but the implications for the domestic funding of VC and early-stage companies in Germany is clear and that is what successive German governments have tried to address.

US and German pension fund allocation comparED

Overall, according to Crunchbase, German start-ups raised €7.6bn in 2024, making Germany the third-largest VC market in Europe, accounting for about 15% of the continent’s total funding. France was in the second place at €7.9bn with the UK leading at €17bn.

German VC deal activity by quarter 2020-2025

The new 2025 coalition government in Germany led by Friedrich Merz has proposed further initiatives to boost VC investment in Germany in its coalition agreement. There are a number of proposed measures to ease the burdens of regulation and to make company formation easier.

On the funding side there are four key initiatives:

Deutschlandfonds: A €100bn fund of funds whose mission is to fill the perceived gap in growth and innovation financing in Germany. The German government is providing €10bn in equity, and it is hoped that private backing will take the total up to the €100bn.

WIN (Growth and Innovation Capital for Germany) The Win initiative was originally launched in September 2024 with an initial target to provide €12bn of funding for German start-ups and innovative companies. The new government wants to increase the funding to €25bn using public guarantees. Companies including Deutsche Bank, Allianz and Deutsche Telekom are supporting the initiative.

Extending the Zukunftsfonds: The government announced that the Zukunftsfonds programme (discussed below) is to be extended beyond 2030.

A new €10bn fund for debt and equity investments to support the digital and green transformation of larger SMEs is being established.

These latest measures reinforce a number of federal initiatives stretching back to 2004 to promote the VC industry when ERP-Financing Instruments were introduced by the Federal Ministry for Economic Affairs and Energy in a programme supported by the European Investment Fund (EIF).

HTGF (High-Tech Gründerfonds) – early-stage funding. The next key development was the establishment of HTGF (High-Tech Gründerfonds). This was set up in 2005 to address a perceived funding gap in Germany in early-stage businesses and to encourage growth in high tech start-ups.

It operates as a public-private partnership between the Federal Ministry for Economic Affairs and Energy, KfW which is the German state-owned investment and development bank based in Frankfurt, and private companies including BASF, Robert Bosch, Knauf, RWE, SAP, WACKER and many others. HTGF has become a core part of the VC scene in Germany analogous to Bpifrance or the British Business Bank. It invests directly in start-ups with investment decisions being overseen by three sector-based committees covering Industrial Technology, Life Sciences and Chemistry, and Digital Technology.

HTGF offers seed funding of up to €2m with a maximum investment of € 8m in each start up. It will lead early-stage rounds. It also acts as an entrepôt of advice and guidance for start-ups giving them access to advice, expert networks and introductions to follow on investors. The focus is very much on start-up businesses. To be eligible for support the business must have a significant presence in Germany, be active in one of the three core sectors and it must not be more than three years old.

Thus far HTGF has four generations of funds (2005-11-17-21) which in total have been invested in over 750 companies. There have been approximately 180 exits. In 2024 the assets under management had reached €2bn. HTGF’s influence has been substantial with, in 2015, the institution being calculated as responsible for 50% of total seed investment stage in Germany and for 20% of early-stage financing by VC investors.

The efforts of the HTGF are supported by the separate European Angels Fund Germany programme launched in 2012 which promotes seed, early, and growth-stage enterprises through co-investment of €0.25m-€5m per company.

Coparion – later stage funding: HTGF and the EAF are focused mainly on early-stage business. To support later stage businesses the Federal Ministry for Economic Affairs and KfW introduced Coparion in 2016. This fund was set up with an initial €225m of funding, supported by the European Investment Bank. Coparion will invest up to €15m in total in each company across multiple financing rounds. It looks to co-invest with private investors with the Coparion funding being no more than half of the value of each round. The typical ticket size is €0.5m-€8m with Coparion doing about ten deals a year. To be eligible companies must have their HQ in Germany and be less than ten years old. Coparion now has a fund size of €275m and investments in 50 companies including Grover, Plan A and Holidu.

Zukunftsfonds ‘Future Fund’. In 2021 The Federal Government introduced the Zukunftsfonds (“Future Fund”). The Zukunftsfonds was set up with €10bn of available VC funding and aims to support start-ups in the growth phase with high capital requirements. As in France and the UK, the intent is to use government funds and backing to stimulate greater amounts of inward funding from private capital sources, in this case an incremental €30bn of private co-investment. KFW was tasked with execution of the funding plan.

At its launch in March 2021 the Federal Minister for Economic Affairs, Peter Altmaier commented: “The Federal Government alone will invest €10bn in the “Zukunftsfonds”. Together with further private and public partners, we will mobilise at least €30bn in venture capital for start-ups in Germany. Combined with our existing financial instruments, we will be able to provide over €50bn in venture capital for start-ups in the next few years together with private investors."

There are different elements in the funding package

- KFW, backed by the ERP Special Fund and the Zukunftsfonds increased its commitment volume for venture capital funds, growth funds and venture debt funds by €2.5bn for the next ten years. The Zukunftsfonds took over the financing of KfW’s Venture Tech Growth Financing programme which had been set up in 2018 with the objective of supporting the financing needs of high-growth tech companies through bridge and post-IPO debt loans.

- EIF Growth Facility: €3.5bn was made available as the GFF EIF Growth Facility. This invests in growth funds and growth financing rounds for start-ups. The investment is generally made under the same conditions as an investment made by private-sector co-investors. For late-stage funds under the ERP / Future Fund Growth Facility, investments are limited to €50m or €75m when combined with other programmes

- €1bn Deep-Tech & Climate Fund invests directly into deep tech companies. ‘Deep tech companies develop innovative scientific breakthroughs with significant macroeconomic impact potential. Development through to market readiness is very time- and capital-intensive. The intent of the new Deep Tech Future Fund is to help these types of technologies in Germany reach market maturity.’

- The Fund is intended to operate for a minimum of 25 years, with management entrusted to the High-Tech Gründerfonds. Supported sectors include AI, big data, quantum, blockchain, cybersecurity, IoT, robotics, sensor technology and additive manufacturing as well as new energy/smart grid, e-mobility/storage, smart city/smart home, and agritech. There is a €30m cap on investments in a single company.

In addition, over time further elements like the €1.3bn Venture Tech Growth Financing (VTGF) programme, the KfW Capital fund-of-funds and the €1bn European Tech Champions Initiative have been added. To be eligible for the Zukunftsfonds, VC funds must be based in Europe, raise at least €50m primarily from private investors, and focus on innovative, German technology companies. By mid-December 2024, ten elements of the Federal Government’s Future Fund were in operation with €13.6bn available to the VC ecosystem up until the year 2030, with around €6.2 billion already committed.

Green Transition Facility: The German government’s €100m Green Transition Facility was launched in June 2023. Also managed by KfW Capital it invests in VC funds focused on climate tech The maximum investment per fund is €25m.The Green Transition Facility was fully invested by end 2024 with KfW Capital having invested c€100m.

KfW, a German state-owned promotional and development bank, plays a key role in these initiatives. As it says ‘KfW has been committed to improving economic, social and environmental living conditions across the globe on behalf of the Federal Republic of Germany and the federal states since 1948. To do this, it provided funds totalling €112.8 billion in 2024 alone.’

KfW Capital was formed in October 2018 to strengthen the supply of venture and growth capital for innovative technology companies in Germany. KfW Capital invests in German and European venture capital funds with the support of the ERP Special Fund and the Federal Government's Future Fund.

As of 30 November 2024, KFW was invested in more than 124 VC funds with a volume of c€2.4bn. In turn the VC funds in which KfW Capital participates invest around four times the capital brought in by KfW Capital. As a result, more than 2,200 start-ups and tech firms have received funding in this way. In addition, the Growth Fund Germany, the KfW Capital fund-of-funds with a total volume of around €1 billion, had by end November 2024 invested €567m in 29 venture capital funds.

Overall, according to Crunchbase, German start-ups raised €7.6bn in 2024, making Germany the third-largest VC market in Europe, accounting for about 15% of the continent’s total funding. France was in the second place at €7.9bn with the UK leading at €17bn. Stefan Wintels, the CEO of KfW, commented recently that the German venture ecosystem remains ‘underdeveloped’ with insufficient private capital flowing into the industry saying:

'We need education. We need a cultural change, and quite frankly, we need better data to demonstrate that the risk-return profile of venture capital is very competitive.’ The government focus on supporting the VC industry has increased because ‘people have understood that a competitive VC ecosystem is important for economic growth, for innovation, and hence long-term competitiveness and well-paid jobs…. I think I see the beginning of this mindset change among private investors in Germany. But we should be honest that this is a long-term journey. This does not happen overnight.’

Tracking AI investors

In our last Growth Equity update we charted the immense investor appetite for AI LLM and foundation models businesses with $131bn having been raised for such companies since the start of 2023. In this edition we chart the major investors in AI rounds.

Since the start of 2023 Open AI has raised $56.6bn. A flurry of funding in the last 15 months has raised $19bn for xAI. Anthropic has received c$11bn of investment from a combination of Amazon and Google plus c$18bn from other investors. Scale AI is a data annotation company which enables models to build AI applications. It has raised $15.3bn across two rounds since May 2024, most of the funding coming from Meta. There have been two ‘talent ‘AI raises for companies founded by former Open AI executives, the $3bn raised for Safe Superintelligence and the $2bn for Thinking Machines Labs. The leading European LLM business in fundraising terms is France’s Mistral which has raised $3.2bn across four rounds since June 2023.

In this edition we chart the major investors in AI rounds. Crunchbase has reviewed the major investors in AI rounds ytd in 2025.

Investors in AI rounds 2025 ytd (lead or co-lead)

A lot of these names are very familiar. SoftBank leads the table for 2025 AI raises ytd mainly by dint of its leadership of the $40bn OpenAI raise in March. It has also been a backer of Perplexity.

Corporates are prominent. Meta is the most substantial investor in Scale AI with leadership of its $14.3bn round in June 2025. Microsoft is the most significant investor in Open AI having invested $10bn in 2023 and having participated in all the subsequent rounds. Space X led a $2bn deal for xAI in July, one in a flurry of deals in the last year that have seen $19bn in total raised for the company.

Google made a $1bn investment in Anthropic in June this year, following its $2bn investment in October 2023 and its investment in the initial $450m round in May 2023. It has also led rounds in Sandbox AQ and A121 Labs. Amazon has led three rounds for Anthropic – in September 2023 and March and November 2024. Nvidia is a regular participant in AI funding rounds having co-led on OpenAI, Mistral, ThinkingMachinesLab, Sandbox AQ, Perplexity and Runway.

Thrive Capital, run by Jared Kushner and with c$25bn in AUM, has been a prominent early investor in AI businesses. It led the October 2024 Open AI $6.6bn round, a $900m round in June 2025 for Anysphere which produces the Cursor AI coding assistant and the $600m round for AI drug discovery business Isomorphic Labs in March this year. Thrive is also invested in Anthropic, Lila Sciences, Hugging Face and ElevenLabs.

Lightspeed Venture Partners led a $3.5bn funding round for Anthropic in March this year. Its view is ‘At Lightspeed, our core belief is that the biggest value from AI’s development will be unlocked at the frontier. Intelligence *is* the product and we are at the beginning stages of the journey. As a result, the most valuable applications are still being built — and the foundation models that underpin them are the essential and valuable substrate for that next wave.’ Lightspeed is also invested in Mistral, leading two of its 2023 raises and in SkildAI where it led the $300m Series A in July 2024. It was a major player in the September 2025 $13bn raise for Anthropic alongside Iconiq, FMR and the QIA.

Not surprisingly Andreessen Horowitz appears regularly as an AI investor. It led the $2bn round for ThinkingMachinesLab in July 2025 and participated in the September 2024 for SafeSuperIntelligence. It has also been prominent in raises for xAI, Mistral and Hippocratic AI.

Peter Thiel’s Founders Fund is an investor in OpenAI, was the lead investor in the $2.5bn round for defence AI company, Anduril in June this year and was an early investor in ScaleAI.

Greenoaks ‘we believe a small handful of companies define each generation’ led the $2bn April 2025 raise in SafeSuperIntelligence. The firm was also an early investor in Scale AI. Kleiner Perkins led the January 2025 $141m raise for Hippocratic AI in January. It is also invested in Windsurf, Glean, and Ambience.

Accel led a $220m round for H in 2024 and made its initial investment into Perplexity in 2025 in the $100m investment round in July 2025. New Enterprise Associates and IVP were also involved in that fundraising and have led a series of rounds for Perplexity.

AI LLM BUSINESSES - $131BN RAISED SINCE THE START OF 2023

The appetite for LLM investment remains strong. As well as the reopening of the OpenAI round there are several more raises in the works. Not content with its four raises since May 2024, xAI is said to be seeking a further $10bn at a $200bn valuation with the Saudi PIF said to be the potential core investor. There are about $17bn of impending AI raises underway. Capital G and Nvidia are to lead a $5bn round for Vast Data with raises also in the works for Luma AI, Lambda, Runway and Sesame AI

Impending AI raises

Markets – Europe to the fore

Lower US interest rate hopes come to the fore.

YTD to end September 16, in local currency terms, NASDAQ is up 15%, the S&P 500 and the FTSE100 are up 12% and is up 10%, The FTSE100 is up 12% and the STOXX600 is up 8%. Funds flows indicate that the brief swing towards European markets and away from the US that occurred in the aftermath of Liberation Day have now reversed – the flow of funds is once again predominantly towards the US.

The FTSE Venture Capital Index which measures the performance of the US venture capital industry, with a strong sector weighting towards technology is up 18% ytd. After a strong summer and a decent results season a typical ‘return to school’ market caution emerged at the start of September with weakness in the bond markets pushing up the cost of borrowing in most major economies around the world, fueling pessimism about growth prospects.

This was then partially offset by poor jobs data (JOLTs) out of the US with July job openings at 7.18mn, down from 7.44m in June and worse than market expectations. This was followed by a weak August jobs report – just 22,000 jobs added plus a downwards revision of 911,000 jobs in the data to the year ended March 2025. This fuelled fears of a slowing labour market and economy in the US, a factor perversely that fuels the equity market which is focused on the potential for interest rate cuts.

Political pressure on the Fed to cut rates has been substantial in recent months with (amongst other things) a visit by the President to inspect the ‘cost overruns’ at the Fed HQ building, the appointment of Stephen Miran, the chair of the White House’s Council of Economic Advisers, to a vacant seat on the Fed; the attempt to remove Federal Reserve Governor Lisa Cook from the Fed for ‘cause’, a move that offers a route to potential de facto control of the Fed by the administration; a series of statements from administration officials including the Treasury Secretary Scott Bessent and the President himself (‘I think we should be paying one percent right now’) that interest rates should be significantly lower and the beginning of the race to appoint a presidential nominee to the Fed Chair when Jay Powell’s term runs out in March 2026.

At the July 30th Fed meeting it kept interest rates steady at 4.25%-4.5% for the fifth meeting in a row, although two of the twelve FOMC committee members voted against the decision, both backing a 25bps rate cut. At the annual Jackson Hole symposium in mid-August Fed Chair Jay Powell appeared to open the way to an interest rate cut at the next Fed meeting in September while still warning of a risk to the economy.

He observed that “With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance’. At the same time though he continued to highlight that the administration’s new tariff regime might increase inflation while the restrictions on immigration may hit the US labour market. Indeed, the Jackson Hole speech was followed by the weak August jobs report but also the news that inflation rose to 2.9% in August up from 2.7% in July. This puts the Fed in a bind with rising inflation a deterrent to cutting rates but a slowing job market suggesting that rates might need to fall to stimulate growth. As Jay Powell observed,: "There is significant uncertainty about where all these policies will eventually settle and what their lasting effects on the economy will be".

The market was already decided, projecting a 97% certainty that the Fed would cut rates at its September 17 meeting taking the rate down to 4.25%. The rate cut duly came. It is less convinced than it was that there will be a further rate cut of 25bps at the meeting on October 29 (the probability was as high as 71% in mid-August but that has faded to 54%) but that still gives a majority view that there will be a second rate cut to 3.75%-4%at that point. There is a substantial minority (45%) looking for a third rate cut to 3.5%-3.75% at the final Fed meeting of the year on December 10.

Meanwhile the market has been shrugging off the impact of the imposition of tariffs on countries who had not reached a reciprocal trade deal by the start of August and the increase of secondary tariffs on India for supporting Russian oil exports. The next key date on tariffs is the end of the 90-day extension of the pause on incremental tariffs on China imports on November 10.

In the UK June inflation rose to 3.6% in June and has hit 3.8% in each of July and August. The Bank of England has warned that inflation is likely to peak at 4% in September, twice its target rate. Despite this, weak economic signals meant that the Bank of England cut interest rates by 25bps to 4% at its meeting on August 7th on a split vote (5-4 second round vote – the first was tied four for ‘no cut’, four for a 25bps cut and one for a 50bps cut).

Since then, UK GDP rallied to 0.3% growth in Q2. In early September as yields rose on long dated bonds as investors focused on government debt levels the Bank of England governor Andrew Bailey observed at the Treasury Select Committee meeting on further interest rate cuts:

“Although we’ve taken a further step, and although I think that the path will continue to be downwards, gradually over time, because policy is still restrictive…. There is now considerably more doubt about exactly when and how quickly we can make those further steps…. That’s, that’s the message I wanted to get across. Now I think, judging by what’s happening to market pricing, I think that message has landed.”

Markets – which had been looking for another interest rate cut by the year end, no longer expects one. The next cut is only fully priced in by next April.

In Europe the ECB held interest rates at 2% at its July 24th meeting, pausing a string of rate cuts. It was a unanimous decision and appeared to express some caution ahead of the imposition of US tariffs on August 1. Inflation was at 2% in July and August. Rates were again held at 2% at the September 11 meeting of the ECB and the market now looks for interest rates to remain unchanged to the end of the year and into 2026. At present the market has just a 50/50 prospect of a 25bps cut by the ECB’s March 2026 meeting.

Market-implied policy rates for the US, UK,

Eurozone and Switzerland

Rothschild & Co strategist Kevin Gardiner summarises the current key drivers of the market in this graphic:

August – Summer’s Lease

Seasonally quieter month still advances on 2024

US VC raises in August 2025 up 6% yoy: August saw 28 US/Canadian venture capital raises of $100m or above, raising $6.7bn. This was 6% ahead of the $6.3bn raised in August 2024.

For the first month since February there were no $1bn plus raises in the month. There were three deals of $500m plus. The largest was an $863m raise for fusion power startup Commonwealth Fusion Systems. Fusion power offers the promise of cheap, abundant, clean energy. It is also extremely difficult to achieve requiring temperatures of 100m-150m degrees Centigrade (hotter than the sun’s core) to achieve fusion. At those temperatures matter becomes plasma whose movement must then be controlled (it mustn’t touch the reactor walls) by powerful magnetic fields called Tokamaks. Fusion raises thus tend to rely on technology advance milestones in their quest to reach commercial scale.

Commonwealth Fusion Systems is collaborating with MIT’s Plasma Science and Fusion Centre to build SPARC, the world’s first fusion device to produces plasmas which generate more energy than they consume. SPARC is a compact high-field tokamak being built with HTS magnets.

Fusion power is seen as critical in powering the new generation of data centres required for AI. CFS intends to build the world’s first large-scale fusion power plant in Virginia, home to the greatest concentration of data centres in the world. The company signed a deal to supply 200MW of electricity to Google in June 2025.

The next two largest raises were both for AI infrastructure businesses. Canadian group Cohere raised $500m from Inovia Capital and Radical Ventures at a $6.3bn pre money valuation. Cohere is a large language model AI business that focuses entirely on the B2B market. Its LLM is trained on the internal data of the companies it serves. It is frequently used by companies where regulation or privacy concerns are paramount and as a non-US owned business can offer additional data sovereignty safeguards. Its customers include financial institutions, government departments, IT companies and telcos. It is on track for $200m ARR by end 2025. Cognition raised $500m in a round led by Founder’s Fund which valued the business at $9.8bn. Cognition’s key product is an AI coding agent called Devin whose function is to speed up software development.

Also, in AI there was a $314m raise for AI robotics business, FieldAI; $250m each for AI coding and automation tools businesses Replit and Elise; $200m for Periodic Labs’ AI applications for scientific materials study and $100m for AI infrastructure business, Decart. This meant that AI related businesses attracted 44% of total US VC funding in August. Although not on the list for August, September started with a $13bn raise for Anthropic valuing the company at $170bn. The round was led by Iconiq Capital, Lightspeed, FMR and the QIA. The previous round of $3.5bn in March 2025 valued the company at $61.5bn.

The US – $6.7bn of US venture backed raises of $100m+ in August

Europe - $1.9bn raised in August: The Rothschild & Co Deal Monitor registered 27 raises of $20m or more in Europe in August with a total value of $1.9bn. August is typically the smallest month of the year for VC raises in Europe and indeed this was the smallest of 2025 to date. The amount raised though was 2.3x the level of August 2024 and brought the year-to-date advance in European VC capital raised to 26%.

There were five deals of $100m in the month. These were led by the $235m raise for Sirius AI led by Temasek. The Swiss based company provides a no code, end to end AI platform addressed at financial services businesses.

Ortivity is a German health tech specialising in outpatient orthopaedic care. Its €200m raise was led by private equity business Apheon and supported by other investors including Unigestion. Ortivity has 100 locations in three regional clusters delivering delivers integrated orthopaedic services covering diagnostics, anaesthesia, surgery, and aftercare.

Swedish Climate Tech business Aira raised a $172m round with Altor, Kinnevik, Lingotto, Temasek and others investing. Aira, which operates in Sweden, Germany, The UK and Italy, designs and manufactures intelligent heat pump systems typically to replace gas boilers. The systems are offered to residential customers with installation and long-term service agreements.

Belgium’s Aerospace Lab is a satellite design, manufacturing, and operations company planning to build an advanced satellite production mega factory near Charleroi capable of producing 500 satellites a year to support programmed like the LEO Iris2 project. Its $110m raise was backed by the European Investment bank.

In the Netherlands, Framer, a no code website design platform raised a $100m Series D at a $2bn valuation. Backers included Meritech and Atomico. Framer supports dynamic websites that can be rapidly updated without developer support.

Europe – $1.9bn of VC raises in August

Fundraising outlook: $25bn of potential raises

After a lively start to September for completed deals (Anthropic $13bn, Mistral $2bn, PsiQuantum $1bn, Databricks $1bn, Figure AI $1bn) there are c$20bn of impending deals, mainly in the US and in AI. At the top of the list is another potential raise for xAI, this one said to be for $10bn at a valuation of $200bn led by the Saudi PIF. AI video generation business Luma has a planned $1.1bn raise at a valuation of $3.2bn. Data centres business Crusoe Energy, a prolific raiser of funds, is said to be raising $1bn at a $10bn putative valuation.

In Europe rumoured raises include $1bn for Revolut, $900m for UK AI infrastructure business NScale, $400m for N26, $345m for Danish food marketplace “Too Good to Go”, $200m for French drones’ business Harmattan, $150m for Dutch semiconductor business Axelera and $100m for UK drones business Cambridge Aerospace.

German AI business N8n is said to be in a hotly contested round of c$100m at a valuation that might be as high as $2.75bn. After its $200m raise in July at a valuation of $1.8bn ‘vibe coding’ software development platform Lovable is reported as having received inbound enquiries for investment at a $4bn valuation.

Growth Equity – c$25bn in reported upcoming raises:

Our views on the state of the venture capital markets

The combination of global inflation, rising interest rates, and increased geopolitical risk substantially impacted the venture capital market in 2022 and 2023. 2024 saw some adaptation to the ‘new normal’. The refocusing of venture backed companies to achieve a better balance of growth, profitability and cash flow and the delivery of interest rate cuts has led to increased optimism and enthusiasm for growth equity in 2025. Our summary of the outlook is:

- The deterioration in the interest rate, inflation and macro-economic environment led to a sharp impact on valuations in private markets. The scale of the fall in the FTSE Venture Capital Index in 2022 was much more substantial than the 33% fall on NASDAQ. This was reflected in some big valuation reductions in some high-profile VC rounds in 2023 and slow recovery in 2024.

- There is substantial interest in venture capital to fund artificial intelligence, both the foundation LLM models and the applications of AI and industries (data centres, semiconductors) supporting the development of AI.

- Outside the AI space the VC market is regaining confidence with a revival of interest in fintech, biotech and software being notable. Certain investors remain very active in the space with substantial funds to deploy. There remains substantial dry powder in the VC industry

- The speed of the investment process has slowed since 2021-22. The level of diligence on new deals has stepped up.

- 2023 and 2024 saw more down rounds, albeit the substantial fund raising of 2021 and the ability of companies to eke out existing resources has limited the number of these.

- It seems likely that the more difficult conditions for fundraising, and the lack of a clear path in some cases to early cash positive status, will mean a flurry of venture capital backed businesses looking to sell or merge their businesses.

- Valuation priorities have shifted with investors having moved away from a pure emphasis on revenue growth and revenue multiples. There is a sharp focus instead on profitability (or a rapid path to it), on positive free cash flow and on DCF and comparative based multiples.

Read the previous editions: May 2022, June 2022, June 2022 (2), July 2022, August 2022, Sep 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024, April 2024, May 2024, June 2024, July 2024, August 2024, September 2024, October 2024, November 2024, December 2024, January 2025, February 2025, March 2025, April 2025, May 2025, June 2025, July 2025, August 2025

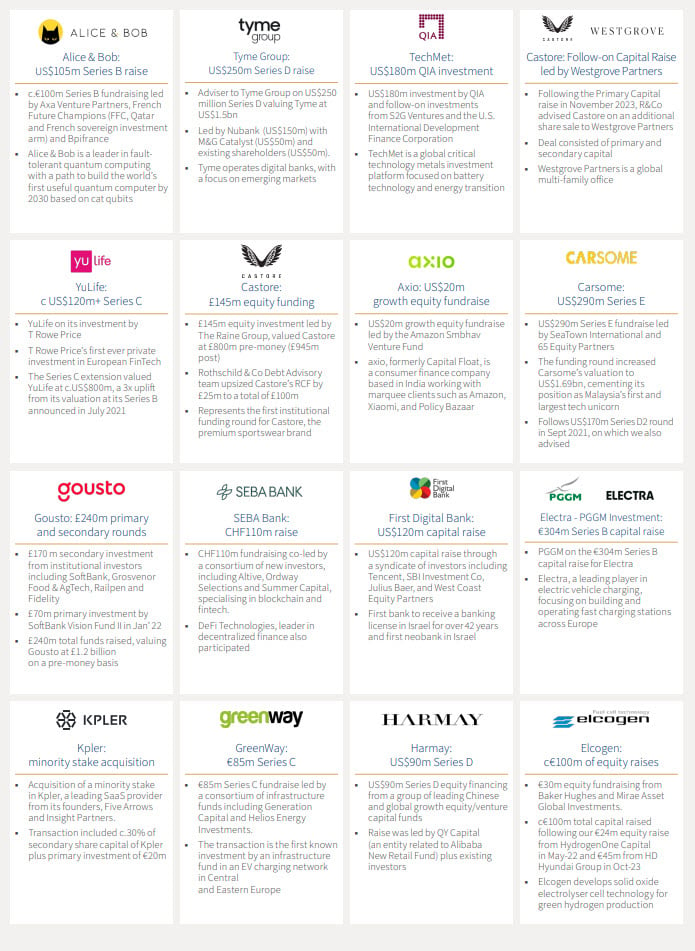

Rothschild & Co: Selected recent deals in Growth Equity and Private Capital

A selection of recent deals on which we have advised:

For more information, or advice, contact our Growth Equity team:

Director of Private Distribution

+44 20 7280 1351

+44 7788 395 556

Head of Private Capital, North America

+1 212 403 5559

+1 917 594 7208

Head of ECM for North America

+1 212 403 5500

+1 917 297 5131

Co -Head of ECM for Europe

+44 20 7280 5377

+44 7907 712 978

Global Head of Strategic and Private Investors.

+44 20 7280 5826

+44 7753 426 961

Head of Private Distribution

+44 7926 905 488

Co -Head of ECM for Europe

+44 20 7280 1668

+44 7912 395 294

Vice Chairman of Equity Advisory

+44 20 7280 5088

+44 7542 477 291

This document is being provided to the addressed recipients for information only and on a strictly confidential basis. Save as specifically agreed in writing by Rothschild & Co Equity Markets Solutions Limited (“Rothschild & Co”) this document must not be disclosed, copied, reproduced, distributed or passed, in whole or in part, to any other party.

This document does not constitute an offer, inducement or invitation for the sale or purchase of securities, investments or any of the business or assets described in it.

This document has been prepared from publicly available information. This information, which does not purport to be comprehensive, has not been independently verified by us or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such. The information provided should not be relied on for any purpose and should not in any way serve as a substitute for other enquiries and procedures that would (or should) otherwise be undertaken.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, no responsibility or liability is or will be accepted by us, as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates or forecasts and nothing in this document should be relied on as a promise or representation as to the future.

Law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this document should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer inducement, or invitation to sell or purchase securities or other investments in any jurisdiction. Accordingly, this document does not constitute a Financial Promotion under the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or equivalent legislation in other jurisdictions. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or is a person to whom this document may otherwise lawfully be distributed. In other jurisdictions, this document is being distributed on the basis that each person to whom it is issued is reasonably believed to be a Professional Investor as defined under the local regulatory framework. Persons who do not fall within such descriptions may not act upon the information contained in this document.