Data centres: the powerhouse fueling the digital age

KEY TAKEAWAYS

- The global artificial intelligence (AI) market size is expected to reach USD 407 billion by 2027, up from USD 86.9 billion five years ago, with an anticipated annual growth rate of approximately 35% across industries until 2030.[1]

- To support this growth, significant investment is needed in data centres which are key elements of AI infrastructure.

- As AI requires considerable amounts of computing power, the challenge for data centres lies in the sustainable use of energy and resources.

How AI is shaping tomorrow

Over the past decade, we have observed major technological shifts that have paved the way for the advent of AI. Since 2015, the number of internet users has surged by 60%, now encompassing 67% of the global population.[2] This rapid expansion of the digital landscape has significantly enhanced global connectivity and increased our reliance on cloud services and servers.

Today, our lives are deeply intertwined with these digital infrastructures, from mobile phones and smartwatches to streaming platforms and social media. Much of our digital experience now resides in the cloud. Recently, generative AI has emerged as a key focus in the tech sector. With tools like ChatGPT becoming widely accessible, AI is reaching a broader audience than ever before. The potential for improved products, services, and productivity gains is substantial, with the ability to significantly drive economic growth.

AI search and generative AI applications are expected to become a major industry worth over USD 100 billion, and the economic potential of generative AI could add between USD 2.6 trillion to USD 4.4 trillion in value to the global economy if fully implemented across various use cases.[3] Additionally, the volume of AI servers is projected to grow exponentially, with a compound annual growth rate (CAGR) of 42% expected by 2027.[4]

Early excitement surrounding further AI applications and the expectation of substantial revenue generation has sparked global investor interest and led to considerable capital inflows into the tech sector, particularly into companies operating large amounts of data across global networks, known as hyperscalers. [5] Investors eager for immediate returns in the stock market were, however, caught off-guard, when concerns rose about the pace of adoption of AI, the heavy spending required to build the initial AI infrastructure, and the time needed to achieve clear AI monetisation. Indeed, as of today, the main challenge for AI is the time required to bridge the investment gap, in particular the data centre capacity, which is a key element of the AI infrastructure.

The unsung heroes of the digital Era

It’s easy to overlook that cloud services and servers rely on physical data centres, which are the backbone of our digital infrastructure. As AI becomes more prevalent in both work and leisure, it will require significant power, necessitating the simultaneous operation of thousands of servers. Consequently, the efficiency of data transfer and communication will increasingly depend on the performance of these data centres.

|

The cost of AI progress

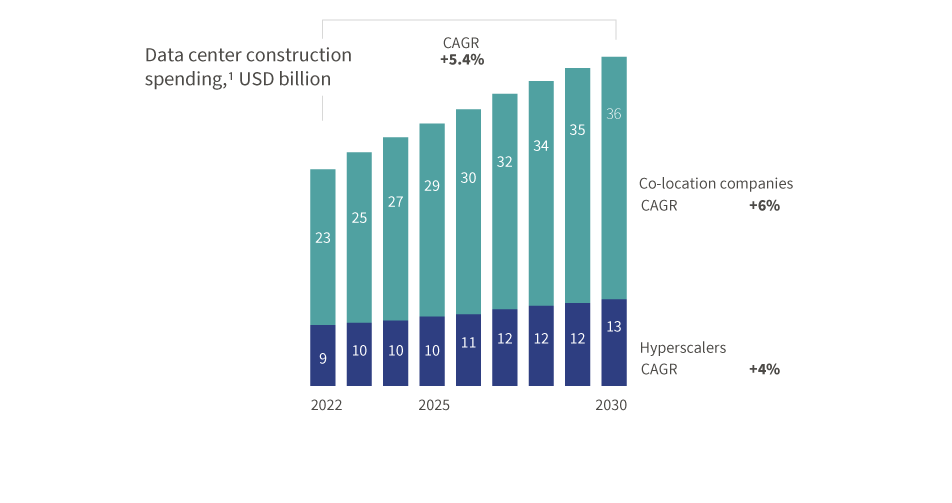

With the advancement of AI applications, such as autonomous driving, the demand for greater data centre capacity will grow accordingly. To fully reach AI's potential, new data centres must be constructed. Building and operating data centres is capital-intensive: Constructing large-scale facilities—with capacities exceeding 250 racks (around 3,500 servers)—can cost tens of millions of dollars, and annual operating maintenance expenses often exceed USD 10 million.[6] Spending on these facilities is projected to reach USD 49 billion (Chart 1), with demand expected to grow by 10% annually through 2030.[7]

Chart 1: Data centre infrastructure market analysis

Global spending on the construction of the data centres is forecast to reach USD 49 billion by 2030.

1 - Includes construction spendings by providers. Excludes enterprise spending and any other capital expenditure outside of construction (such as equipment).

1 - Includes construction spendings by providers. Excludes enterprise spending and any other capital expenditure outside of construction (such as equipment).

Source: Synergy Research Group, McKinsey & Company: Investing in the rising data economy, (Link), 17.01.23.

AI vs. sustainability: the green challenge

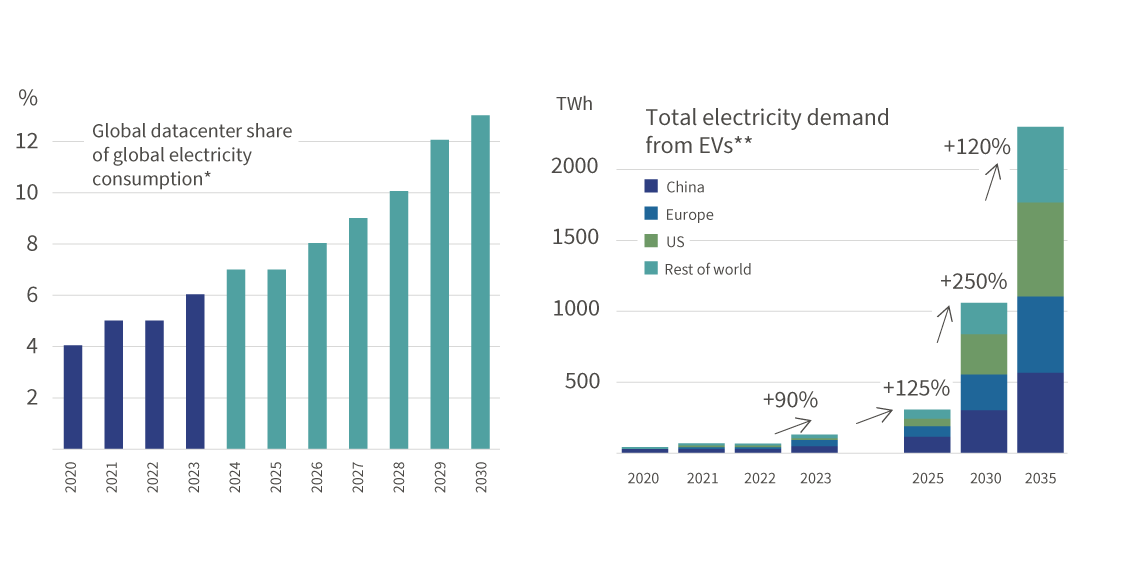

The rapid adoption of AI will significantly increase power consumption by data centres, often relying on electricity from local utility companies typically designed to serve residential areas. With power resources still constrained, billions of USD in capital investments are being directed to transform the data centre market, as expanding capacity requires substantial financial outlay. Additionally, the servers in these facilities need extensive cooling solutions, which often rely on water-intensive systems. Globally, data centres already account for a significant portion of overall electricity consumption, underscoring their considerable energy footprint (Chart 2).

Chart 2: Watt's up?

* Source: Huawei Technologies, on global electricity usage of communication technology: Trends to 2023

**Includes passengers cars, buses, light commercial vehicles, and heavy-duty trucks. Source: global EV data explorer, IEA

Tech shake-up: impact on AI infrastructure investment

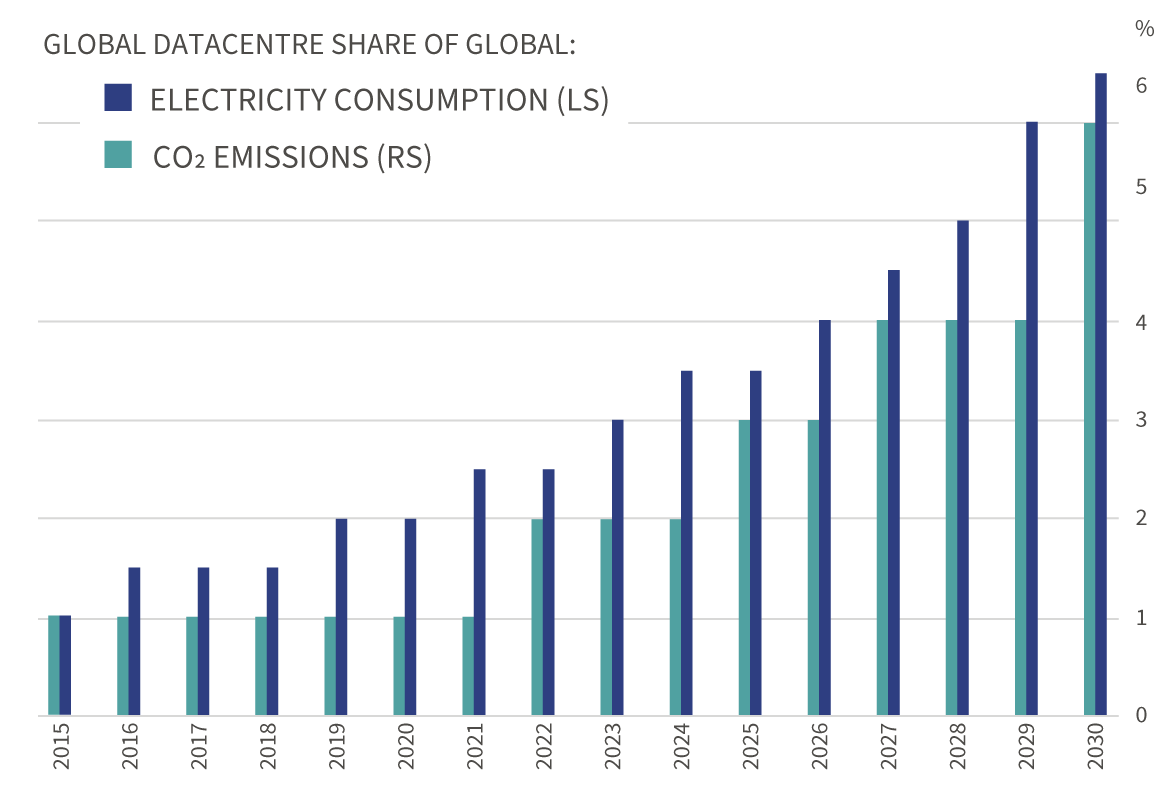

As AI's energy demands continue to rise, so do the hyperscalers' total carbon emissions. Google reported a nearly 50% increase in emissions over five years due to the surge in AI usage.[8] Microsoft on the other hand announced investments to improve the efficiency of its data centres while focusing on greener energy supply.

Indeed, data centres now sit at the crossroads of digital, energy, and environmental technologies, making efficient energy management essential to minimising their societal impact. The pressing challenge is to generate sustainable energy to meet the growing demands of data centres and AI technology (Chart 3).

Chart 3: Data Centre and Co2 emissions (BCA Research):

Data centres are power hungry, and polluters too

Source: Huawei Technologies, on global electricity usage of communication technology: Trends to 2023

It is important for investors to consider the companies involved in developing this foundational AI infrastructure. Looking ahead, data centres face the challenge of efficiently managing and optimising power resources while striving to minimise energy consumption. The future of data centres will demand responsible energy use and significant progress is still required to meet the ambitious goal of reaching "net zero" emissions by 2030 [9], a target now under threat from the rising power demands of artificial intelligence systems.

However, as global energy production is not unlimited, a trade-off between technology advancement and protection of the environment is not possible. Therefore, as AI requires increasing amounts of energy, further developments must be carefully planned and managed to ensure that the expansion of AI and data centre infrastructure does not compromise our planet's health.

Our insights, your investment journey

[1] Statista: Artificial intelligence (AI) market size worldwide from 2020-2030, 30.07.2024.

[2] Statista: Number of internet and social media users worldwide as of April 2024, 30.07.2024.

[3] McKinsey: The economic potential of generative AI: The next productivity frontier, June 2023.

[4] Gartner: Forecast Analysis: AI-Optimized Servers, Worldwide, Nov. 2023.

[5] Hyperscalers provide cloud computing and data management services to organizations that require vast infrastructure for large-scale data processing and storage.

[6] Intel Granulate: Understanding Data Center Costs and How they Compare to the Cloud, 31.07.24 and Avery Fairbank: Understanding data centre costs and dynamics, (Link), Nov. 23.

[7] McKinsey & Company: Investing in the rising data economy, 17.01.23.

[8] FT: Google emissions jump nearly 50% over five years as AI use surges, 2.07.2024.

[9] The science shows clearly that in order to avert the worst impacts of climate change and preserve a livable planet, global temperature increase needs to be limited to 1.5°C above pre-industrial levels. Currently, the Earth is already about 1.1°C warmer than it was in the late 1800s, and emissions continue to rise. To keep global warming to no more than 1.5°C – as called for in the Paris Agreement – emissions need to be reduced by 45% by 2030 and reach net zero by 2050.

Read more articles

-

Rothschild & Co impulsa su crecimiento en España con la incorporación de Álvaro Santos en el área de Wealth Management

Press releases

El nuevo nombramiento refuerza las capacidades locales y supone un paso más en la expansión del negocio de banca privada en España.

-

Geopolitics Blog: Christmas Season: Reasons to be cheerful

Insights

In our latest geopolitical blog, Mark Sedwill, Chair of Geopolitical Advisory at Rothschild & Co offers his reflections on six strategic reasons for Christmas confidence.

-

Five key questions for a carefree retirement

Corporate

Planning for retirement early helps secure your finances and gives you the freedom to enjoy travel, hobbies or family time. These key questions can guide you