Asset Management Europe: Monthly Letter – October 2019

Marc-Antoine Collard, Chief Economist, Head of Economic Research, Asset Management, Europe

Economic environment

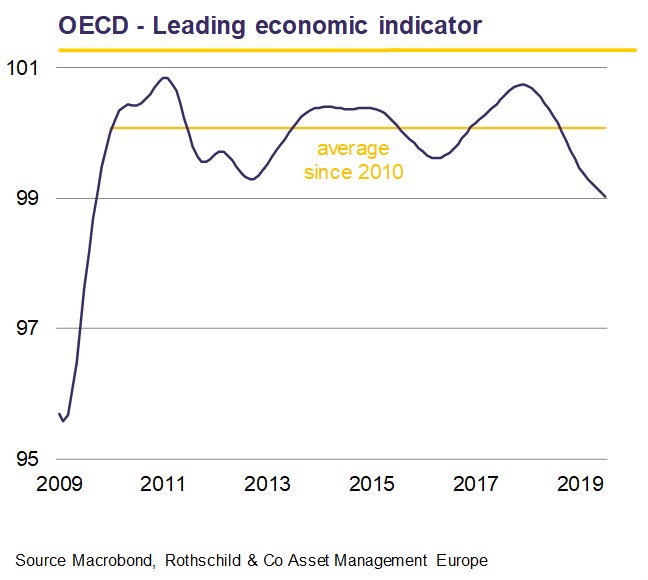

The expansion of the global economy is caught in a tug-of-war between geopolitical drags and supportive macroeconomic policy. Recent economic data suggest nonetheless that the widespread moderation in GDP is likely to persist for longer than most economists anticipated. Indeed, survey measures of business activity have continued to weaken, particularly in manufacturing. So far, the service sector had held up, with improved labour market conditions and modest expansionary fiscal policy underpinning consumer spending.

Click the image to enlarge

However, the dichotomy between manufacturing and services is somewhat unravelling, as neither sectors works in isolation. In fact, over a third of manufacturing exports derive from services, and services contribute to more than half of exports. The risk of the manufacturing slowdown having a long-lasting impact on economywide growth prospects might materialise. For instance, as operating conditions worsened, manufacturing businesses in most Asian economies signalled a fall in new orders; correspondingly, employment expectations contracted at the sharpest rate for nearly four years. Recent reports also show a downturn in global hiring intentions and reduced working hours in several countries, suggesting these drags are no longer solely concentrated in the goods-producing industries. This could, in turn, place downward pressure on household incomes, spending and demand for services.

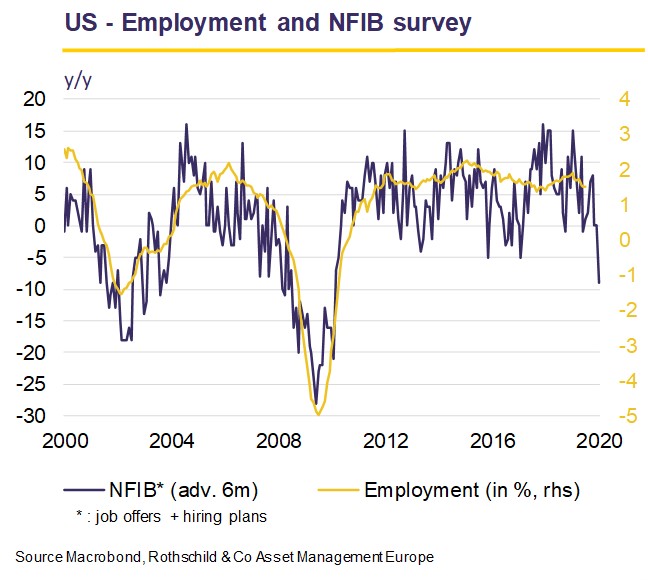

The confluence of deteriorating growth prospects and decisively dovish monetary policies are driving sovereign bond yields to a new nadir, as the amount of fixed income securities with negative yields hit a record, with over USD 17 trillion according to certain estimates, equivalent to roughly 20% of world GDP. Obviously, lower interest rates should help to cushion the extent of the economic slowdown. However, the impact of recent changes in policy interest rates might be modest, at best, especially in advanced countries. In that regard, the Fed has the most room for further accommodation and the clearest path to follow with additional pre-emptive easing. The US economy is not immune to trade tensions and certain pockets showed signs of weakness, namely slowing employment and investment growth. Since the cost of borrowing is already low and hardly a hindrance for most businesses, lower interest rates look unlikely to move the needle on growth and investment spending.

Click the image to enlarge

In addition, it cannot be ruled out that central banks will assess their own interest rate to be at such a level that any further decline would damage the economy more than it would help due to the negative impact on the profitability of banks, therefore hurting their ability to grant credit. In the eurozone, the ECB cut its deposit rate by -10 bps to -0.5% and restarted its asset purchase programme (QE), which might have to run for a prolonged period. In order to quell criticism, a two-tier system for reserve remuneration was introduced, in which part of banks' holdings of excess liquidity will be exempt from the negative deposit facility rate. That said, the ECB's willingness and ability to act are uncertain as dissidence from the Governing Council's hawks has led market participants to question how aggressive the ECB can get. Furthermore, the staff projection for just 1.5% core inflation at end-2021 despite open-ended QE raises questions of monetary transmission. As the macroeconomic backdrop remains especially vulnerable for export-oriented economies, and monetary policy effectiveness might have reached its limits, the ECB has explicitly asked for fiscal policy to support growth prospects. For now, only a few countries have both the fiscal capacity and political will to answer the call.

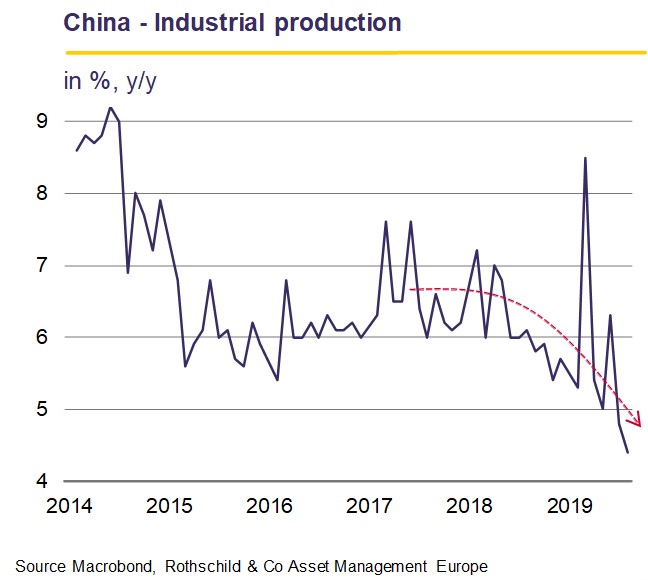

Meanwhile, China cut - again - the reserve requirement ratio by -50 bps for all financial institutions and by -100 bps for some smaller commercial banks. More broadly, monetary conditions have been very accommodative for more than a year, yet Chinese economic growth continues to weaken. While trade tensions are magnifying the slowdown, the lack of economic response to a myriad of measures is also explained by an impaired policy transmission mechanism due in part to high private sector indebtedness. What's more, the authorities' fight against corruption and pollution, as well as shadow banking reform, are also at play. The upshot is that optimism surrounding recent policy announcements might be misguided and investors could be disappointed not only by the magnitude, but also the effectiveness of the support measures.

Click the image to enlarge

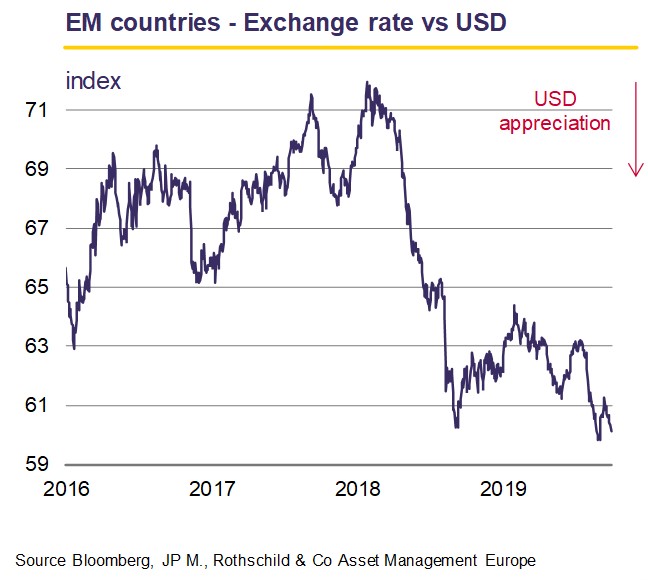

The reduction in US interest rates and limited inflationary pressures have provided scope for many other emerging-market (EM) central banks to lower policy interest rates. That said, as sentiment towards EM assets soured and the depreciation of the yuan accelerated, most currencies have reached a very low level against the USD, which will weigh on the private sector's ability to service USDdenominated debt, forcing some countries to tighten monetary policy in order to fight capital outflows. To add to an already complex equation, weak global trade and China's slowdown have exacerbated persistent vulnerabilities in many EMs.

Click the image to enlarge

Overall, the global outlook has become increasingly fragile and uncertain as continued and deepening trade policy tensions are taking a toll on confidence and investment. Accordingly, central banks have eased policy to pre-empt a further deterioration and this shift to a more accommodative monetary stance has reassured investors. Giving the impression of a dance, markets have continued to sway as trade tensions pushed them down and monetary policy propelled them up. Yet, equity investors might become disenchanted if the central banks do not play their music loud enough to silence the din of trade war. In this push-pull dance, bond yields have continued their downward glide while the USD reached a new multi-decades high just as, worryingly, we see emerging signs of weaknesses in the labour market.

Download the PDF version Monthly Letter (430 KB)